A view on the 2026/2027 Australian Federal Budget

Introduction

Treasurer Jim Chalmers has handed down the Albanese Government’s fifth Budget. While this Federal Budget has been characterised as ambitious by the Federal Government, it does raise questions regarding the underlying benefits of the reform. While fundamental changes to the tax system are forecasted to significantly raise revenue, average Australians are unlikely to feel tangible benefits.

Consistent with market expectations, the Budget is focused heavily on a package of tax measures that the Federal Government has introduced to boost home ownership and address intergenerational equity challenges. While several of the measures themselves are not a surprise given the media reports in recent weeks, some of the specific details have caught some observers off-guard. The Budget adds to recent tax reforms that paint Australia as a challenging (and potentially unpredictable) place to do business. Despite the housing-affordability framing, several changes reach deep in the Australian start up and business ecoystem.

The key tax measures from this year’s Federal Budget are outlined below.

As anticipated in recent weeks, the most significant Budget announcement relates to a measure that was framed as tax reform to boost home ownership – by reforming negative gearing and reducing the capital gains tax (CGT) concessions. Treasury has stated that this is to “improve the fairness of the tax system, support home ownership and help fund new tax cuts for workers.”

"Improving" (or complicating?) capital gains

From 1 July 2027, the 50% CGT discount for individuals, trusts and partnerships will be replaced by cost base indexation for assets held for more than 12 months alongside a 30% minimum tax on net capital gains (Indexation and Minimum Tax).

This will apply to nearly all CGT assets, including assets that were previously exempt from CGT (i.e. on the basis that they were acquired prior to the introduction of the CGT regime on 20 September 1985). Indexation and Minimum Tax will not apply by default to any ‘new build’ residential properties (discussed below), whereby investors will have a choice between the 50% CGT discount or Indexation and Minimum Tax.

Additionally, the amendments are not proposed to change the application of the main residence CGT exemption, the superannuation fund CGT discount and the current small business CGT concessions.

In relation to assets acquired prior to 1 July 2027, a transitional regime will be in effect for assets that are held for longer than 12 months (i.e. the impact of the changes will be limited on assets that have already been acquired). For these assets, the 50% discount will continue to apply on any gains arising before 1 July 2027 on assets that were acquired after the introduction of the CGT regime. In relation to assets that are ‘pre-CGT’ assets which were acquired before 20 September 1985, gains arising on these assets before 1 July 2027 will be exempt.

The changes therefore gives rise to a ‘multi-speed’ and complex CGT regime, and the Budget does not identify exactly how these transitional provisions will be effected in practice. However, based on documents released by Treasury that accompany the Budget, Treasury have stated that:

- The portion of the gain that is either exempt (for pre-CGT assets) or is subject to the 50% discount (for post-CGT assets) will be calculated as the difference between the asset’s cost base and the market value of the asset as at 1 July 2027.

- Indexation and Minimum Tax will then apply to calculate the tax payable on gains that are referable to the period from 1 July 2027 onwards, using the value of the asset at 1 July 2027 as the cost base.

- The value of an asset at 1 July 2027 is to take the form of a valuation of the asset at that time or via a specified apportionment formula that estimates the asset’s value on 1 July 2027 based on its growth rate over the asset’s holding period. Treasury has also stated that the ATO will provide tools to estimate this value.

There are several measures which will be subject to clarification once further guidance or draft law is released. In particular:

- It is unclear whether the 30% minimum tax rate would also apply to distributions of capital gains made by a Managed Investment Trust (MIT), given that a withholding tax rate of 15% would otherwise apply. This could mean that non-resident investors deriving capital gains from a MIT have a more favourable tax outcome as compared to Australian investors (excluding superannuation funds).

- It remains to be seen whether the rules will distinguish between disposals of direct and indirect disposals of assets. This is relevant for two reasons. Firstly, it will be relevant to determining the relevant asset taken to be disposed of in applying the transitional provisions (i.e. if the shares in a company or units in a trust are disposed, is the asset to which the transitional provisions applied the shares or units, or is it the underlying property that is owned by the company or trust). Secondly, in determining the pre-CGT status of an asset, the tax law currently contains provisions which ‘look-through’ to the ultimate investors to determine the status of an asset and whether it is a pre-CGT asset or not. It will be relevant to consider how these measures may apply in context of the transitional provisions.

Given the CGT changes apply to all CGT assets, Treasury have specifically highlighted that the Federal Government will consult on the interaction of the CGT reforms and incentives for investment in early-stage and start-up businesses “given the unique characteristics of the tech and start up sector.”

Our expectation is this consultation has been flagged given some of the recent media attention associated with the impact that amendments to the CGT would cause on the technology and start-up industries given their reliance on equity-based remuneration arrangements. It remains to be seen whether this consultation leads to any meaningful change in how the CGT regime applies to interests in early-stage and start-up businesses.

"Two-step" negative gearing system

Following years of negative gearing being on the hypothetical chopping block, the Budget includes significant reforms to the negative gearing rules, with the availability of negative gearing for residential property to be limited to new builds from 1 July 2027. Under the proposed changes, losses from existing residential properties acquired after 7:30pm on Budget night will no longer be deductible against an investor’s broader assessable income. Instead, those losses will be quarantined and only deductible against rental income or capital gains derived from residential property. Any excess losses may be carried forward and offset against residential property income in future income years. This introduces a similar (although not identical) system to that which exists in other jurisdictions, including the United States.

The measure is also expected to include exclusions for widely held trusts and superannuation funds, together with targeted exemptions for build-to-rent developments and private investors supporting ‘new housing’ initiatives.

Based on broader commentary ‘new housing’ would represent residential properties which genuinely add to supply, inclusive of:

- Dwellings constructed on vacant land,

- Duplexes constructed through a knock-down rebuild replacing a single, free-standing house,

- Newly constructed apartments bought off-the-plan, or`

- A newly built property which is occupied for less than 12 months before being first sold.

Existing property renovations, knock-down rebuilds of a singular free-standing house should not constitute new builds for these purposes.

A&M View on Boosting Home Ownership Proposal

The key strapline from the Federal Budget is that the measures reforming negative gearing and capital gains tax concessions are proposed “to support an additional 75,000 homeowners over the decade.”

Given investors will continue to have access to other negatively geared investments (including commercial property), shares and other non-residential property assets, rather than producing a direct and proportionate shift into new residential housing, the measure may instead encourage some investors to reallocate capital away from residential property altogether (with resulting impacts on property prices).

In our view, this creates tension between the perceived policy objectives and the likely behavioural response. While there may be encouragement to invest in new housing, it may also stagnate investors desires to dispose of existing residential properties.

The underlying ‘grandfathering’ rules will be central to how the measure operates in practice. Based on the announcements, existing residential properties acquired before Budget night will be excluded from the new restrictions . While this provides certainty for existing investors, it may also have the practical effect of discouraging the sale of established residential investment properties already held.

The grandfathering mechanism may encourage investors to hold existing properties for longer than they otherwise would have. While it may encourage some investment into new residential stock, its practical impact may be more nuanced than the policy framing suggests. In particular, the combination of grandfathering, continued access to negative gearing for other asset classes, and exemptions for particular investment vehicles may limit the extent to which the measure drives meaningful additional housing supply.

Separately, one interesting observation is that this measure may also have an unintended consequences of actually reducing a young person’s ability to enter into the property market. To the extent that supply tightens as a result of owners looking to retain grandfathered properties and new housing growth does not rapidly increase, entry into the property market may only become more difficult – especially in the case of ‘rent-vesting’ as opportunities for young owners to take first steps towards entering the property market are reduced.

Better targeting the Research and Development Tax Incentive

The Federal Government has announced a number of changes to the Research and Development (R&D) Tax Incentive from 1 July 2028. These changes are in response to the Strategic Examination of Research and Development (SERD) Report released earlier this year and reflect mainly positive changes for taxpayers and wider accessibility to the R&D Tax Offset (with some catches). The changes include:

- Increasing all R&D Tax offset rates by 4.5 percentage points. The effect of this is that the R&D tax offset rates would be:

- For taxpayers with an annual turnover of less than $50 million per year: 23% over their corporate tax rate.

- For taxpayers with a turnover of greater than $50 million per year: 13% for R&D expenditure up to 1.5% of total business expenditure, and 21% for R&D expenditure over 1.5% of total business expenditure.

- For taxpayers with an annual turnover of less than $50 million per year: 23% over their corporate tax rate.

- Removing eligibility of supporting R&D activities, which differs from the recommendation in the SERD report of a fixed rate for these activities.

- Reducing the intensity threshold from 2% to 1.5% to access the R&D premium rate (set to be 21%) for businesses accessing the non-Refundable R&D Tax Offset.

- Increasing the turnover threshold to access the refundable R&D Offset from $20m to $50m, and limiting it to companies under 10 years of age. Other companies will only be able to access non-refundable R&D Tax offsets.

- Firms with a turnover below $50 million that do not meet the above requirements will only be eligible for a non-refundable R&D Tax Offset, albeit at the highest R&D Tax Offset rate.

- Lift the maximum eligible expenditure threshold from $150 million to $200 million per annum, which will impact a small number of businesses.

- Lift the minimum expenditure threshold from $20,000 to $50,000.

In addition to the above, the Federal Government will establish a National Resilience and Science Council to advise on Research, Development and Innovation objectives. It is expected that the Council will report on the R&D Tax Incentive.

These changes to the R&D Tax Incentive will have mixed implications for taxpayers:

- The increase to the R&D Tax Offset rates is a positive for all companies undertaking R&D.

- Companies will need to be careful as to how they document their R&D as any supporting (e.g. background research) R&D activities will no longer be eligible.

- While the increase in the turnover threshold to access the refundable R&D Tax Offset from $20 million to $50 million will benefit some, companies greater than 10 years old will not be able access cash benefits. Companies with long development timelines or SMEs that undertake ongoing R&D may in future be locked out of the refundable offset.

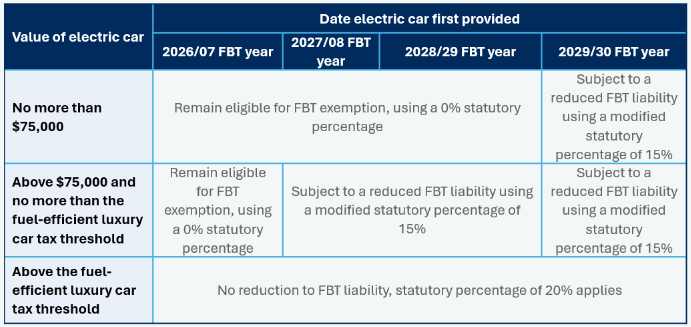

Fringe Benefits Tax & Electric Vehicles

As widely anticipated given the high uptake, the Federal Government is winding back the full FBT exemption for electric vehicles. However, as a direct result of the current fuel crisis, the Federal Government has delayed implementing any changes to the current FBT exemption for electric vehicles until 1 April 2027.

Eligible electric vehicles will retain any FBT concessional treatment or exemption that was available when the arrangement first commenced.

The changes will be gradually implemented, dependent on the value of the vehicles as follows:

The reportable value of electric cars will continue to be calculated as if the FBT concession did not apply.

Loss carry back and refundability reforms for businesses and start-ups

Effective 1 July 2026, the Federal Government will re-introduce measures to allow companies with aggregated global turnover under $1 billion to carry back a tax loss against tax paid in the prior two years, up to a limit of their franking account. This replicates similar changes previously enacted in response to the COVID-19 pandemic.

Additionally, from 1 July 2028, companies with aggregated annual turnover under $10 million that generate a tax loss in their first two years of operation will be able to convert the loss into a refundable tax offset. This offset is capped at FBT paid and PAYG withholding on Australian employee wages in the loss year.

This has the potential to result in a real cash flow improvement for early-stage companies that are not yet profitable but are meaningfully contributing to job creation.

Making tax simpler for businesses

From 1 July 2027, the $20,000 instant asset write-off (IAWO) will be made permanent for small businesses with aggregated turnover up to $10 million.

The 5-year “lock-out” rule which prevents small businesses from re-entering the simplified depreciation regime after opting out will remain suspended until 30 June 2027.

Small and medium businesses will now be able to opt into monthly PAYG instalments and use an ATO-approved calculation embedded in their accounting software to calculate and vary instalments closer to real time. Notably, the Federal Budget has indicated that taxpayers with poor compliance histories may also be required to report and pay monthly.

In our view these measures are sensible housekeeping rather than meaningful reform, noting they broadly impact the “timing” of deductions rather than the underlying amount. Further they reinforce broader policy intent to reduce the reliance of taxpayers on the ATO as a source of short-term working capital.

Expanding venture capital tax incentives

With effect from 1 July 2027, the Federal Government will expand the existing venture capital tax incentives to better facilitate venture capital investment and support early stage and growth businesses.

Relevantly, the cap on the asset size of an investee business will increase. In the case of Venture Capital Limited Partnerships (VCLP), the cap at time of investment will rise to $480 million (up from $250 million). For Early Stage Venture Capital Limited Partnerships (ESVCLPs), the cap will rise to $80 million (up from $50 million).

The ESVCLP investee asset cap at which investment returns can still be fully tax exempt rises to $420 million (from $250 million), which materially extends the runway for portfolio companies to grow while still allowing the LP-level tax exemption.

The maximum fund size of an ESVCLP will increase to $270 million from $200 million, which provides managers with room to raise larger funds without losing the benefits associated with the ESVCLP regimes.

For a strategy that backs Australasian founders early and holds through to scale, these expansions are genuinely helpful. The fund size cap in particular has been a constraint on the regime's accessibility for the larger end of the Australian VC universe, and the broadening of the VCLP investee cap may makes them structurally available to some mid-market buyout strategies.

While this seems like a good news story for venture capital, the combination of the CGT and venture capital changes is genuinely mixed. While the VCLP and ESVCLP cap expansions are helpful, the CGT discount reform is materially harmful at the founder, employee and partner level.

Global Anti‑Base Erosion Rules (Pillar Two) Side-by-Side Package Implementation

The Federal Government has announced that Australia’s global and domestic minimum tax legislation will be amended to implement the OECD/G20 Inclusive Framework’s Pillar Two “Side-by-Side” (SbS) package from 1 January 2026. While included in the Budget announcement, the measure was broadly anticipated following the OECD’s release of the SbS package on 5 January 2026, and is consistent with Australia’s established approach to implementing Pillar Two in line with OECD guidance.

The SbS package is a further refinement of the global minimum tax framework. It is intended to simplify certain aspects of Pillar Two while preserving the core objective of a 15% minimum effective tax rate. In practice, it introduces a combination of permanent safe harbours and simplification mechanisms designed to reduce compliance pressure in lower-risk cases and improve consistency across jurisdictions.

Key elements include:

- a new SbS Safe Harbour for MNE groups headquartered in jurisdictions with sufficiently robust domestic minimum tax systems. Where available, this effectively disapplies the Income Inclusion Rule (IIR) and Undertaxed Profits Rule (UTPR) for in-scope entities, although Qualified Domestic Minimum Top-up Taxes (QDMTTs) continue to apply independently. At present, the United States is the only jurisdiction recognised as a qualified SbS regime, meaning access is currently limited in practice, subject to further OECD assessment of additional jurisdictions;

- a permanent UPE Safe Harbour following expiry of the transitional UTPR Safe Harbour. This is intended to reduce UTPR exposure for constituent entities located in the ultimate parent entity jurisdiction. No jurisdictions are currently recognised as qualifying, so the measure is not yet available pending further OECD assessment and domestic implementation;

- a Simplified ETR Safe Harbour which allows jurisdictional effective tax rates to be calculated using consolidated financial statement data rather than full GloBE calculations. While presented as a simplification, it remains technically complex in practice, requiring detailed adjustments, annual eligibility testing, and application of the broader GloBE framework. Importantly, it does not retain the “once out, always out” feature of the transitional Country-by-Country Reporting (CbCR) safe harbour;

- a Substance-Based Tax Incentive Safe Harbour designed to preserve the effectiveness of genuine domestic investment incentives by allowing certain qualified tax incentives to reduce top-up tax exposure where sufficient economic substance exists, subject to payroll and tangible asset-based caps aligned with real activity; and

- a one-year extension of the transitional CbCR Safe Harbour through to 2027, maintaining the 17% threshold and providing additional time for systems and processes to be fully embedded.

The Simplified ETR mechanism is simple in name only. While it reduces the scope of calculations, it still requires detailed application of the GloBE rules and careful data alignment, and does not materially reduce the underlying technical complexity.

Overall, the measure reflects Australia’s continued alignment with the OECD framework and the broader international trend toward streamlining Pillar Two without altering its core architecture.

Importantly, the amendments do not replace existing Pillar Two obligations, which are already in force. In practice, MNE groups will need to continue complying with the current rules for FY24 and FY25 while preparing for the amended framework from 1 January 2026. This creates a dual-track period in which both regimes operate in parallel, requiring coordinated management of compliance, reporting and governance across both frameworks.

Strengthening the Foreign Resident Capital Gains Tax Regime

Given its impact upon the Federal Government’s Budget position, the Budget has detailed the already announced reforms to the CGT exemption for foreign residents, which apply to disposals of certain renewable energy infrastructure assets at any time before 30 June 2030. Draft law for this exemption was released last month and subject to a truncated consultation process.

While the Budget itself does not add any further detail beyond what was already known, the Budget did disclose that, during the five-year forward estimates period, the renewable energy CGT exemption is budgeted to decrease tax receipts by $425 million. This implies that Treasury’s expectation is that foreign residents are anticipated to derive total capital gains of $2.8 billion over the next four years.

As several parties have already identified in their submissions to Treasury, the relatively minor forecast revenue impact highlights the limited nature of the exemption. This is at odds with Treasury’s stated policy of incentivising investment in the renewables sector.

The Budget also states that the amendments to the foreign resident CGT regime (in relation to the definition of “real property”) have been characterised as having no positive impact to revenue on the basis that the measure is a “clarification intended to protect existing revenue.”

A minimum tax on discretionary trusts

In a seismic shift for the trust landscape, the Budget announces a 30% minimum tax on discretionary trust income from 1 July 2028. Under the proposal, the tax would be imposed at the trustee level at first instance (unless a higher rate applies).

Corporate beneficiaries would not be entitled to a credit for tax paid by the trustee. As a result, income distributed to a corporate beneficiary would be taxed at the trustee level and again in the hands of the corporate beneficiary with the effect being that the effective tax rate for corporate beneficiaries being up to 51%. This outcome appears to be a deliberate policy design aimed at dissuading taxpayers from the use of corporate beneficiaries (commonly referred to as “bucket” companies) as an income tax deferral strategy.

In practical terms, the proposed amendments are intended to significantly limit the advantages of discretionary trust structures and broader private group structures. While these may be subject to some consultation, we anticipate there will be limited appetite by the Federal Government to move away from the announced measures. This means many private groups in Australia may need to revisit their current structures as well as their approaches to estate planning and asset protection.

While the Budget Papers also reference potential rollover relief to allow restructuring away from discretionary trust structures, details are limited. To this end, we expect that any relief may build on existing rollover provisions (such as the existing small business restructure rollover) and apply in limited cases, while still giving rise to other tax or duty implications.

Where trust income is distributed to “individuals and other non‑corporate beneficiaries”, those beneficiaries would be entitled to a non‑refundable tax credit in respect of the tax paid by the trustee. In effect, this would result in discretionary trust distributions being subject to a minimum effective tax rate of 30%.

Supporting working Australians

Cutting taxes with a Working Australians Tax Offset

From 1 July 2027, taxpayers will be entitled to a $250 Working Australians Tax Offset (WATO), which is legislated to be a permanent annual offset available to working Australians on income derived from work.

The WATO effectively lifts the tax-free threshold on work from $18,200 to $19,985 (or up to $24,985 for those eligible for the Low Income Tax Offset), which represents the largest permanent increase since 2012.s

The new WATO stacks with the previously legislated marginal rate cuts taking effect on 1 July 2026 and 1 July 2027, as well as the newly introduced $1,000 instant deduction.

Introducing a $1,000 Instant Tax Deduction

From 1 July 2026, a $1,000 instant tax deduction will be available without substantiation to Australian residents earning income where the total work-related expenses claim is under $1,000.

Taxpayers with work-related expenses above $1,000 can continue to claim in full under the existing rules.

Non-work deductions (e.g. charitable donations, union and professional association membership fees) remain separately deductible in addition to the $1,000 instant deduction.

It is expected that the law will be amended to prevent a double benefit where expenses covered by the $1,000 instant deduction are also salary packaged. The draft legislation will need to be reviewed to assess the practical impact on existing salary sacrifice arrangements in respect of FBT.

This measure is designed to complement the new WATO and the legislation marginal rate cuts effective from 1 July 2026 and 1 July 2027.

Increases to the Medicare Levy low-income thresholds

In a measure represented to provide continuing cost-of-living relief and set to apply retrospectively from 1 July 2025, the Medicare Levy low-income thresholds will be increased by 2.9% for singles, families, seniors and pensioners.

The increase to the thresholds is estimated to decrease tax receipts by $450 million over five years from 2025-26.

Whilst never unwelcome, as in previous years, the practical impact of the cuts may not provide sufficiently tangible benefits for low-income taxpayers.

Protecting the tax system against fraud

In keeping with recent Budgets, the ATO is to receive additional funding to deliver Phase 2 of the Counter Fraud Strategy to modernise the prevention and detection of fraud in the tax and super systems. This is intended to enhance the ATO’s ability to combat fraud by tax agents and intermediaries.

Most meaningfully under this announcement, the Budget announces that the ATO will receive powers to pause the recovery of tax debts where the taxpayer is a victim of fraud by tax agents or intermediaries, to waive such debts in “appropriate circumstances” and to enable the ATO to recover the debt from the intermediary instead. This is an important shift for taxpayers who are victims of fraud. Currently, as a feature of the self-assessment regime, a legal fiction exists which treats a tax agent’s statement as being the taxpayer’s own statement. It remains to be seen what will constitute “appropriate circumstances”.

An additional measure announced in arming the ATO with additional powers to combat fraud in the tax system was the broadening of garnishee powers to include jointly-held assets in circumstances where assets are jointly held to delay or frustrate recovery actions.

Under the proposed changes, in circumstances where the taxpayer facing a tax debt shifts assets (for example, house, bank accounts) into joint names (i.e. with a spouse or associate) in an attempt to frustrate garnishee action, the ATO will have power to garnish these assets, with the ‘frustrate recovery’ qualifier (as currently drafted in the Budget papers) signalling this is intended to operate as an anti-avoidance trigger rather than a blanket extension to enable the ATO garnishee power over all jointly-held assets.

The Federal Government will also progress further targeted exceptions to tax secrecy and enhancements to tax regulators’ informationgathering powers to support integrity, compliance and effective administration of the tax system.

The Budget has also identified that the ATO will undertake additional targeted compliance activities over the two years from 2026–27 to address fraud in the system, specifically identifying the R&D Tax Incentive as an area of focus.

Extending the ban on foreign purchases of established dwellings

The Federal Government will extend the temporary ban on foreign purchases of established residential dwellings, which will now run through to 30 June 2029.

The policy objective is to decrease competition for established housing stock for Australian buyers while channelling foreign investment toward new housing supply.

Limited exceptions for purchases of established dwellings that support housing supply will continue, as do the general foreign investment screening exemptions for permanent residents and New Zealand citizens.