SINGAPORE’S GST INVOICENOW: A Compliance Requirement with Enterprise Wide Consequences

The Inland Revenue Authority of Singapore (IRAS) has confirmed that GST InvoiceNow will become mandatory for all GST‑registered businesses, representing not just a compliance change but a major move in how transaction data, systems, and controls operate across the enterprise. Early planning is critical, as readiness is determined upstream, at the point where transactions are created and processed, no longer just at the GST return filing stage.

What’s New

At the Ministry of Finance Committee of Supply (COS) 2026, IRAS announced a significant expansion of the GST InvoiceNow requirement. What began as a soft launch and a requirement for new voluntary GST registrants will now be progressively extended to all GST registered businesses, with full adoption required by April 2031.

Under this framework, GST registered businesses will be required to transmit invoice data directly to IRAS via the InvoiceNow network, which is built on the internationally recognised Peppol e-invoicing standard.

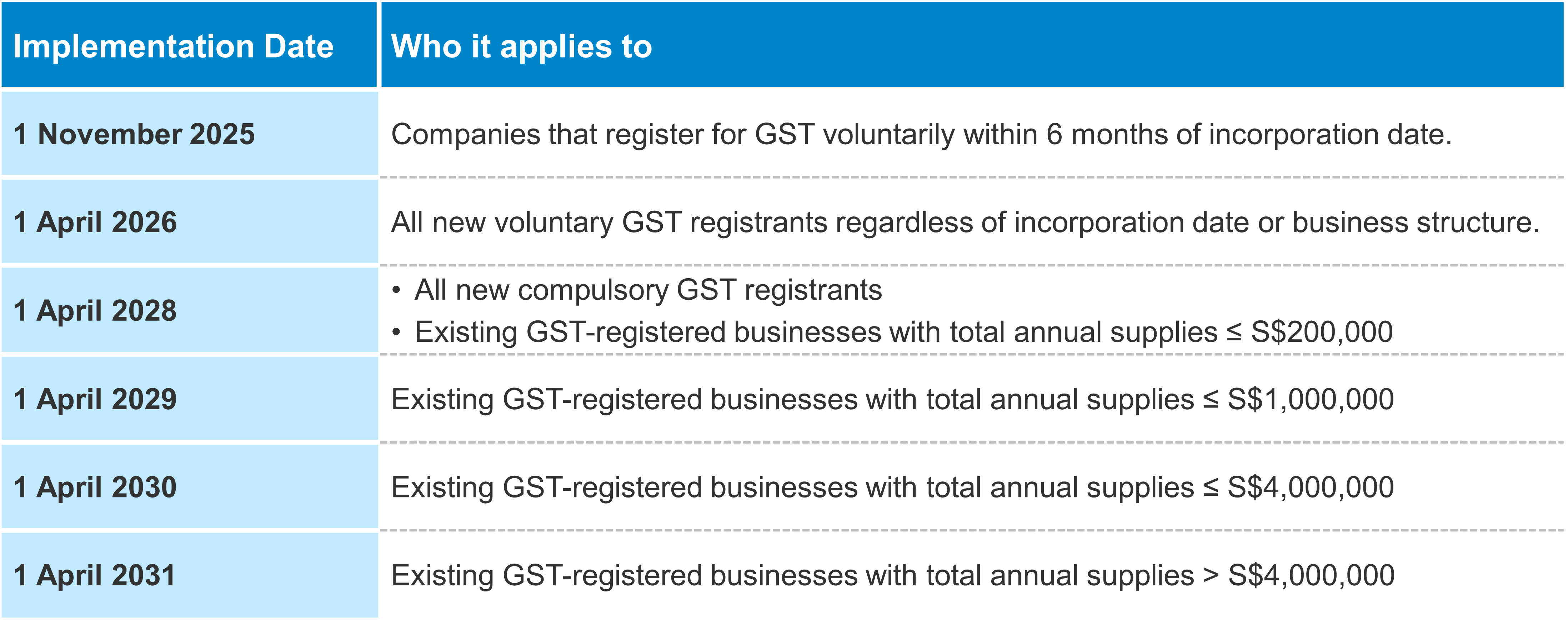

Key Timelines to Note

IRAS has confirmed a phased implementation approach, providing businesses with time to prepare:

To support the transition, the Government has announced transitional grants of:

- Up to S$1,000 for SMEs; and

- S$5,000 for larger businesses

Why This Is Not Just a Tax Issue

GST InvoiceNow is not just a tax or regulatory change; in practice, it represents a fundamental shift in the operating model. E-invoicing moves GST compliance towards a far more data driven and process dependent environment. This means outcomes are no longer determined solely at the point of GST return preparation, but much earlier - when transactions are created, captured and processed across the business.

InvoiceNow readiness typically cuts across multiple functions:

Finance (AR/AP)

- Invoice and credit note workflows

- Customer and supplier master data

- Handling of month‑end exceptions and adjustments

- Recurring non-standard transactions (rebates, discount models)

Tax

- GST determination logic and scenario mapping (e.g., zero‑rating, exemptions)

- Governance, controls, and audit trail

- Alignment between transactional data and GST reporting

Systems

- ERP and accounting system configuration

- Integration approach and access point selection

- Testing, security, change management, and ongoing support

Operations/Sales/Procurement

- Upstream commercial triggers such as contracts, delivery terms, returns, rebates and intercompany flows

Our Practical Takeaway

While the regulatory timelines may appear manageable, experience from other e‑invoicing mandates shows that effort, complexity and risk are often underestimated, particularly where data quality, system integrations, and cross‑functional processes are involved.

Early planning and strong cross‑functional ownership are critical to avoiding last‑minute remediation, unplanned cost overruns and disruption to business‑as‑usual operations. Organisations that engage early are better positioned to preserve design flexibility, align with broader transformation agendas and extract long‑term value from the change.

What Management Should Focus on in the Next 90 Days

- Set clear ownership and governance

This change is very different from other tax legislative changes; this affects the business as a whole and often a combination of the front and back-office. Here, tax has a direct impact on the client engagement systems and strategic vendor relationships. The tax teams should ensure that the right businessowner is appointed. We have seen a clear shift globally to this being Finance‑led or even front-office lead, with Tax and IT as co‑owners, ensuring clear accountability for outcomes, not just delivery. Clear ownership reduces fragmentation and ensures decisions reflect enterprise‑wide priorities rather than functional silos. - Align InvoiceNow with the transformation agenda

Explicitly map InvoiceNow requirements to existing or planned ERP, finance transformation and data initiatives. Management should make a deliberate decision on whether InvoiceNow will be embedded into these programmes now, or intentionally deferred but designed for, to avoid rework and duplication later. - Preserve design optionality early

Agree upfront on high‑level design principles and constraints (e.g., global vs local deployment, control expectations, data governance standards), while avoiding premature commitments to specific vendors or technical architectures. This maintains flexibility as regulatory guidance and business priorities evolve. - Make funding visible and planned

Surface expected investment early so InvoiceNow is reflected in multi‑year technology and transformation roadmaps, rather than emerging later as a compliance surprise. Treating it as part of transformation spend supports better prioritisation and cost control without taking budget from already limited tax budgets. The business case for funding should clearly articulate not only the funding requirements but also surface the expected value opportunities in all relevant processes. - Define re‑engagement and escalation triggers

Establish clear points at which the appointed InvoiceNow owner will return to the Board or transformation committee, such as ERP design decisions, material regulatory updates, or major transformation milestones, to ensure timely oversight, informed decision‑making and overall effective transformation.

A Simple Starting Checklist

- Use the IRAS GST InvoiceNow Implementation Date Calculator to confirm your likely onboarding window and target timeline.

- Socialise the requirement early with key stakeholders and draft the business case for change to secure the budget, clearly identify ownership and IT capacity within management and alignment with the medium and long term IT roadmap.

- Perform walk through of all processes including Order‑to‑Cash, Procure‑to‑Pay and Record‑to‑Report to identify GST and invoicing touchpoints.

- Review data quality, including tax codes, item mapping, and customer and supplier master data.

- Assess system readiness, covering ERP and accounting capabilities, integration gaps, security and key controls, particularly around master data.

- Build a phased implementation roadmap aligned to your mandatory onboarding window and the business transformation agenda with a focus on incorporating testing, training, and change management.

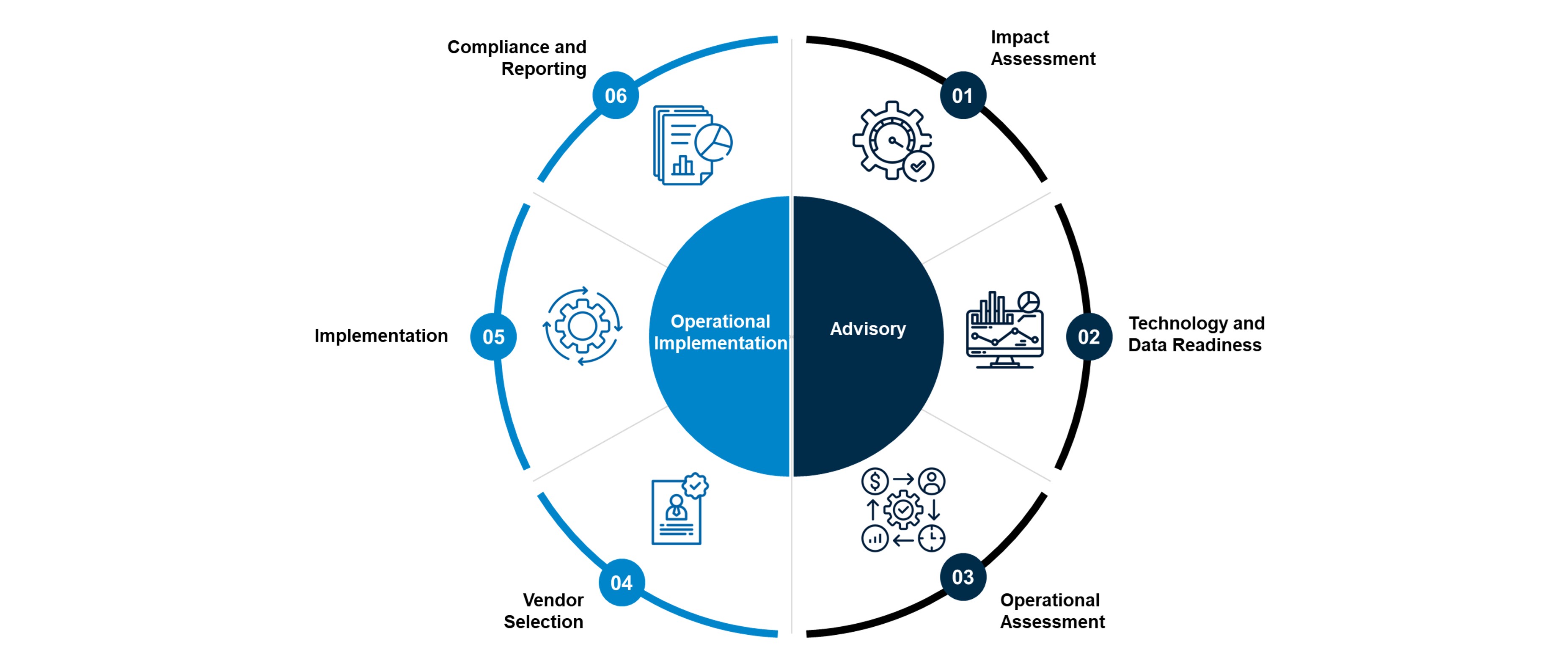

How We Can Support

A&M is experienced in supporting organisations navigate regulatory and e‑invoicing change from initial impact assessment through to implementation and ongoing compliance. We are focused on translating client requirements into practical solutions, support delivery with minimal disruption, and help clients stay prepared for future change.