Manufacturing in the UAE: Tax and Trade Considerations for Industrial Growth

Driven by "Make it in the Emirates" and Operation 300bn, the UAE is pivoting toward advanced manufacturing and export-led growth. For multinational groups, integrated tax and trade planning is essential to reduce costs, manage compliance risk and support a more sustainable manufacturing and export model.

Industrial incentives and policy relief are strictly linked to the UAE's industrial licensing framework. Regulatory benefits apply exclusively to entities holding a valid industrial licence for localised production, processing or transformation. This remains distinct from pure commercial trading or distribution, where finished goods are imported for resale without adding local value.

The customs industrial exemption allows valid industrial licence holders to import raw materials, semi-finished goods and capital equipment free of the standard 5% GCC customs duty. Unlike other global markets that mandate intensive bonded stock tracking, the UAE framework removes the duty directly at the point of import, providing immediate liquidity and cash flow benefits.

The UAE applies a highly competitive headline corporate tax (CT) rate of 9% on taxable income exceeding AED 375,000. Optimisation depends on the strategic alignment of accounting profits and tax treatments:

- Deductions: Operational business expenses are generally fully tax-deductible, while capital investments in plant and machinery are recovered over time via tax depreciation.

- Free Zone Dynamics (QFZP): Under the Qualifying Free Zone Person framework, industrial manufacturing is a "qualifying activity." Entities meeting operational substance and transfer pricing conditions can access a 0% CT rate.

- Global Minimum Tax: In-scope multinational groups must monitor the interaction with OECD Pillar Two rules and its potential 15% effective minimum tax impact at a consolidated level.

As the UAE CT framework includes formal transfer pricing (TP) rules aligned with OECD principles, businesses should evaluate their operating model, functional profile and intercompany arrangements at an early stage of any manufacturing investment or restructuring.

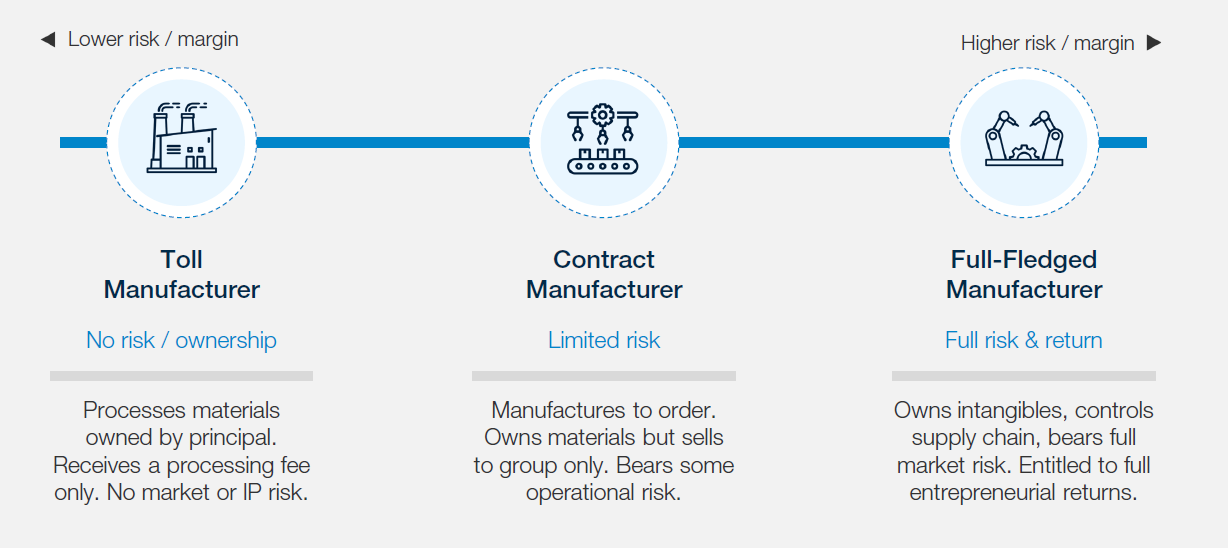

For UAE manufacturing entities, a key consideration is the characterisation of the local entity within the wider group supply chain. For example, the UAE entity may operate as a toll manufacturer, contract manufacturer, limited-risk manufacturer or full-fledged manufacturer, depending on the functions performed, assets used and risks assumed. This characterisation will directly influence the expected profitability of the UAE entity and the appropriate TP methodology.

Misalignments between intercompany import values declared for corporate tax and those used for customs exemptions heavily escalate regulatory scrutiny. Businesses must maintain robust contemporaneous documentation, including a master file, local files and TP disclosure forms, thereby ensuring intercompany agreements perfectly match day-to-day operational conduct.

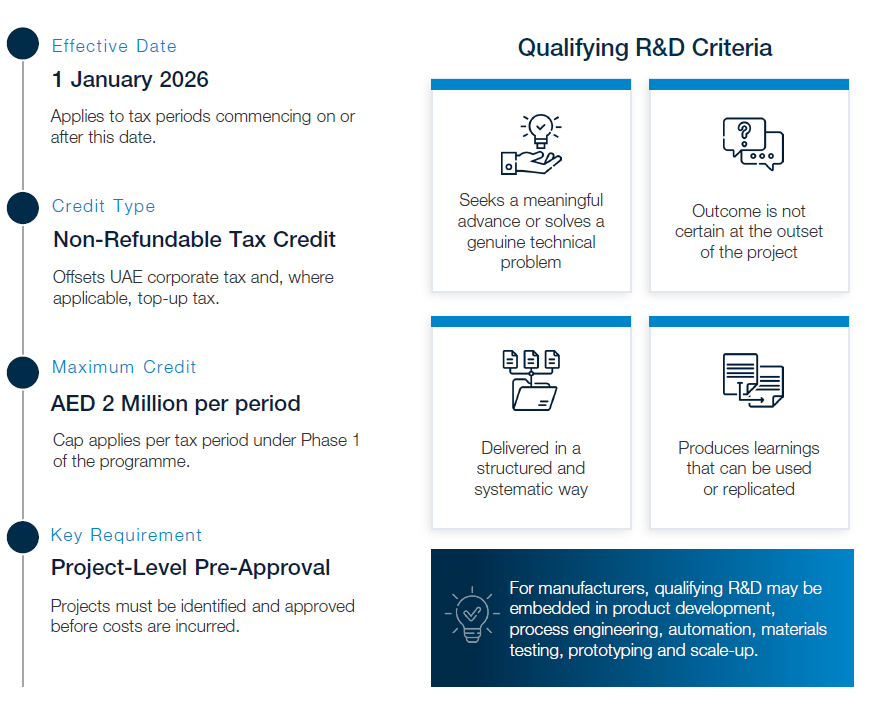

Effective for tax periods commencing on or after 1 January 2026, Phase 1 of the UAE’s R&D Tax Incentives Programme allows eligible manufacturers to access a non-refundable tax credit of up to AED 2 million to offset corporate or top-up tax liabilities.

Qualifying activities must target a clear technological advance or resolve a specific technical uncertainty using a structured, reproducible methodology. Because the Programme requires project-level pre-approval, manufacturers maximise value by identifying eligible workflows early such as process engineering, automation scaling or prototyping and mapping costs directly to those technical milestones.

Conclusion

The UAE's industrial growth creates a compelling commercial imperative for localised production. Unifying regulatory licensing, customs duty exemptions, corporate tax positioning and transfer pricing baselines ensures multinational groups are optimally positioned to capture economic value from the region's industrial expansion.