SINGAPORE’S GST INVOICENOW: Working Backwards from 2031

As detailed in our previous article, “Singapore’s GST InvoiceNow: A Compliance Requirement with Enterprise Wide Consequences”, IRAS has confirmed that GST registered businesses will be required to transmit invoice data directly to IRAS via the InvoiceNow network, with full adoption required by April 1, 2031. At first glance, April 2031 can feel comfortably distant. For many organisations, GST InvoiceNow is being interpreted as a future compliance obligation, something to be addressed once mandatory onboarding is closer.

Experience from other e‑invoicing mandates shows that the hardest work does not happen near the deadline. It happens much earlier, when organisations face data quality issues, system constraints, operating model decisions and cross‑functional ownership questions that take time to resolve. In practice, by the time a business reaches its formal onboarding window, many of the most important design decisions have already been made.

This is why the most effective way to approach GST InvoiceNow is not to count forward to 2031, but to work backwards from it.

Why 2031 Is Not the Real Deadline

The phased roll-out approach masks an important reality: readiness is not determined at the point of transmission to IRAS, but much earlier, when invoices are created, coded, approved and processed across the enterprise.

GST InvoiceNow shifts compliance from a periodic, retrospective exercise to one that is data driven and process dependent. Once invoice data is transmitted, errors in GST treatment, master data, or transaction logic are exposed immediately rather than being discovered later during GST return preparation.

As a result, organisations that wait until their mandatory onboarding date often find that:

- A fragmented IT landscape increases implementation complexity.

- Master data standards are incomplete and potentially inconsistent across entities or systems.

- GST logic is embedded inconsistently across order‑to‑cash and procure‑to‑pay flows.

- Remediation becomes reactive, expensive and disruptive.

The formal deadline may only be 2031, but the effective deadline for many design decisions is years earlier.

The Hidden Lead Times Organisations Underestimate

E‑invoicing mandates consistently reveal a gap between regulatory timelines and real implementation effort. Common areas where lead times are underestimated include:

- Operating Model and Ownership

Unlike traditional tax changes, GST InvoiceNow affects front and back‑office processes. Globally, we are seeing ownership shift away from being tax led, towards finance or business‑led models, with tax and IT as co‑owners. . The key to success is to see this as a broad multi-functional or potentially global project, where ERP design choices are standardised to the extent possible, e-invoicing technology implementation is leveraged across the footprint, and processes are streamlined.

Without clear ownership:

- Design decisions fragment across functions.

- Risk tolerances are misaligned.

- Accountability for outcomes becomes unclear.

Establishing governance early is one of the strongest predictors of a smooth implementation later but this must not be underestimated. The reality is all the teams are over capacity and will push back on adding yet another large project. Strategically leveraging a globalised approach to e-invoicing will minimise duplication, maximise benefits of deployment of technology.

- Data Quality and Standardisation

GST InvoiceNow relies on structured invoice data. This places new emphasis on:

- Customer and supplier master data accuracy.

- Tax code and item mapping consistency.

- Treatment of non‑standard transactions such as rebates, discounts, credit notes and adjustments.

Data issues are rarely confined to tax teams. They often sit with commercial, finance operations or shared service centres, and resolving them requires sustained cross‑functional effort.

- ERP and Systems Constraints

InvoiceNow readiness depends heavily on how invoices are generated and processed within ERP and billing systems. Organisations that are part way through ERP upgrades or finance transformations face critical timing questions:

- Should InvoiceNow be embedded now, designed for later, or retrofitted post‑go‑live?

- How will controls, audit trails and exception handling operate in a near real‑time environment?

Decisions made today can materially increase or reduce future rework.

Why “Phased” Does Not Mean “Passive”

The phased rollout is intended to give businesses time to prepare, but only if that time is used deliberately.

While some organisations assume they will wait for IRAS notification of their mandatory implementation date before acting. In practice, globally we have seen organisations use the runway to:

- Socialise the impact at management and board level.

- Align InvoiceNow with broader transformation and data agendas as well as other global mandates.

- Preserve design optionality before systems and vendors are locked in.

- Start a master data cleansing project.

- Secure funding as part of multi‑year roadmaps, rather than as a last-minute compliance request.

What “Working Backwards From 2031” Looks Like in Practice

Reversed planning from end-state reframes the question from “When do we have to comply?” to “What has to be designed, embedded and working by the time of implementation?”

For most organisations, that means ensuring (well ahead of implementation) that:

- Invoicing processes across order‑to‑cash and procure‑to‑pay are mapped and understood.

- GST determination logic is consistent, documented and embedded upstream.

- Master data governance is defined and enforceable.

- ERP and integration choices are compatible with InvoiceNow requirements.

- Roles, responsibilities and escalation paths are clearly established.

This work cannot be compressed into the final months before onboarding. It benefits from early starts, iterative testing and alignment with broader change programmes.

What Is the Opportunity for Tax?

While GST InvoiceNow may be viewed as a compliance burden by many, it also creates a meaningful opportunity for tax teams to move upstream and become more embedded in how the business operates.

Traditionally, indirect tax teams have operated downstream, reviewing outcomes after transactions have already occurred. These mandates change that dynamic. Because compliance outcomes are now driven by transactional data created in real time, tax input is required at the point of design, not just at the point of filing the return.

In short, this allows tax to shift from being a reactive control function to a proactive design partner but only if tax engages early and is equipped to operate cross‑functionally.

Our Practical Takeaway

April 2031 is a regulatory milestone, not an implementation plan. Organisations that treat GST InvoiceNow as a distant compliance event risk discovering, often too late, that the real effort sits in data, systems and operating model foundations laid years earlier. Those that work backwards from the end state are better positioned to control cost, reduce disruption and preserve flexibility.

In our experience, the most successful implementations share one trait: they start long before they are forced to.

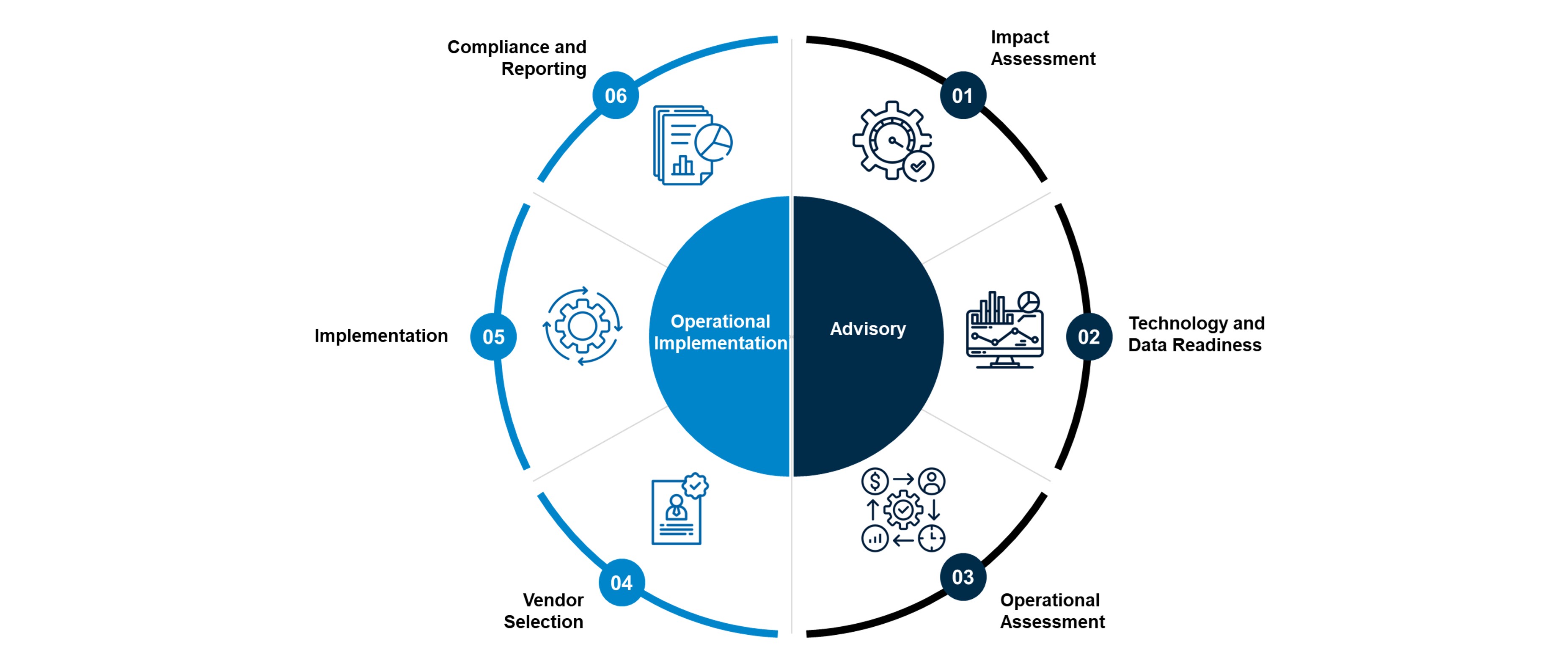

How We Can Support

A&M is experienced in supporting organisations navigate regulatory and e‑invoicing change from initial impact assessment through to implementation and ongoing compliance. We are focused on translating client requirements into practical solutions, support delivery with minimal disruption, and help clients stay prepared for future change.