Joint Ventures in Focus: Market Conditions and Keys to Structuring Successful JVs

Executive Summary

Joint ventures are having a moment. Global M&A headline numbers look healthy, but behind them a quieter shift is underway. Companies that would have defaulted to acquisition are now asking a different opening question. At Alvarez and Marsal (A&M), we have been on the inside advising our clients in real time as this shift happens. The question is no longer whether JVs belong on the strategic agenda. It is how and when to use them appropriately.

- Tariffs, a changed financing environment, and regulatory scrutiny of full acquisitions have converged to make the JV structure a deliberate first choice for a growing number of companies. A&M expects these conditions to persist for the foreseeable future.

- More than half of JVs fail to create sustained shareholder value. The differentiator between ventures that succeed and those that do not is almost never top line strategy. It is in planning and execution. The governance design, financial rigor, operating model work, and launch discipline are what most organizations underestimate until it is too late.

- A&M’s framework for building lasting joint ventures centers on four areas where formation decisions have the greatest bearing on long-term outcomes: strategic alignment, operational alignment, governance structure, and capital requirements and exit strategy.

The Market at a Glance

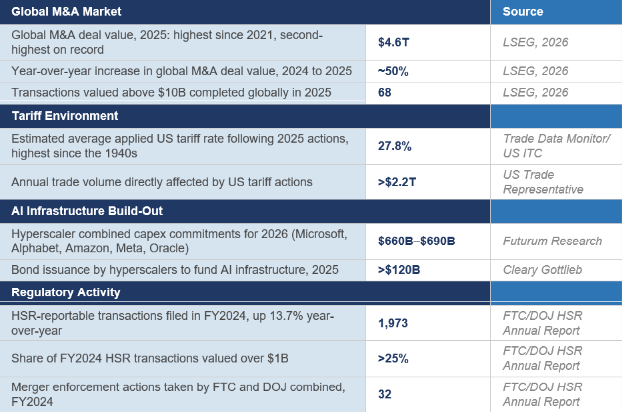

Global M&A deal value reached $4.6 trillion in 2025, according to LSEG.[1] This is the highest figure since 2021 and the second-highest in over four decades of recorded data. Sixty-eight transactions were valued above $10 billion, a concentration of large-deal activity that drove the headline while masking a decline in overall volume. Mid-market deal counts fell. Cross-border activity, while recovering, remained selective. Capital is moving, but toward deals large enough to justify the cost and complexity of execution, and away from transactions where regulatory, financial, or geopolitical exposure makes the outcome uncertain.

Within that overall picture, one sector stands apart in ways that have reshaped the JV market more broadly. The AI infrastructure build-out, led by the world's largest technology companies, has generated a volume and scale of joint venture activity with few modern precedents. According to Futurum Research, Microsoft, Alphabet, Amazon, Meta, and Oracle have collectively committed between $660 billion and $690 billion in capital expenditure for 2026 alone,[2] nearly double their 2025 levels. To fund it, hyperscalers issued over $120 billion in bonds in 2025, per Cleary Gottlieb's capital markets review, with the majority of that issuance in the first half of the year.[3] Much of that capital is flowing into purpose-built ventures: partnerships with utilities to secure dedicated power generation, arrangements with real estate developers to build and operate facilities, and multi-party consortia to develop the interconnection infrastructure that the AI economy requires. The Stargate venture, announced in January 2025 with a stated commitment of $500 billion across OpenAI, SoftBank, Oracle, and MGX, is the most visible example.[4] These are not typical commercial joint ventures. They are infrastructure financing structures for strategic national priorities, and they are establishing templates for large-scale collaborative investment that other industries are beginning to study and adapt.

The AI infrastructure story is specific to a small number of extraordinarily capitalized organizations. But the effect on the broader JV market is real. It has made the joint venture the default structure for very large capital projects in ways that are already visible in energy, healthcare, and advanced manufacturing. In A&M’s client work, both sides of this dynamic are visible. Large enterprises are committing capital to infrastructure partnerships at a scale that would have been difficult to contemplate three years ago. A separate cohort of companies is actively working through how to position themselves in a market that increasingly requires a collaborative structure as the price of entry. That pattern is not confined to technology. It is showing up wherever capital intensity and strategic urgency intersect.

Key Market Indicators | 2024–2025

Tariffs: When Trade Structure Becomes Deal Structure

When the Trump administration announced sweeping tariff actions in April 2025, the immediate reaction in M&A markets was not panic. It was recalculation. The average applied US tariff rate reached 27.8%, its highest point since the 1940s according to the US International Trade Commission.[5] Chinese imports faced duties of 145%, matched by equivalent Chinese retaliation.[6] More than $2.2 trillion in annual trade flow was directly in scope, per US Trade Representative data.[7] In February 2026, the Supreme Court struck down those tariffs in a 6–3 ruling, holding that IEEPA does not authorize the President to impose tariffs.[8] The relief was short-lived. Within hours of the decision, the administration imposed a new 10% global tariff under Section 122 of the Trade Act of 1974, with signals of further increases, and announced its intent to use Section 232 and Section 301 authorities to maintain equivalent tariff revenue.[9] For companies weighing cross-border structure decisions, the specific legal authority matters less than the practical reality: The tariff environment that prompted the JV recalculation in 2025 remains in place, and the administration has demonstrated the will to preserve it through whatever mechanisms are available.

The disruption was not confined to North America. European companies with transatlantic supply chains and Asian manufacturers built on China-plus-one logic confronted the same recalculation. Across every major trade corridor, the response was consistent. Where outright cross-border ownership became harder to justify, the JV offered a way to maintain commercial presence without concentrating tariff exposure in a single corporate structure.

What emerged from that recalculation, in many cases, was a case for the joint venture that had not previously existed. Depending on the jurisdiction and sector, a venture structured to produce goods inside the end market can reduce or eliminate exposure to import duties that would otherwise apply. A partnership with a local producer may satisfy domestic content requirements and, in many markets, provides a degree of political standing that a foreign parent company would struggle to establish on its own. The trade framework negotiations that the US has been conducting since May 2025 have reinforced this logic at the geopolitical level. Japan's structured commitment to import US energy through a purpose-built commercial arrangement, and the supply-chain cooperation provisions embedded in ongoing EU talks, are JV structures by another name.

In some markets, the joint venture is no longer just a commercial arrangement. It is the price of entry.

Rates: A Partial Thaw with a Changed Calculus

The Federal Reserve cut rates six times between September 2024 and December 2025, bringing the federal funds rate to 3.5% to 3.75%.[10] The April tariff shock reignited inflation expectations and disrupted the anticipated pace of rate relief, leaving M&A activity in 2025 more concentrated in the second half of the year than had previously been expected. During the years of elevated rates, the math on leveraged acquisitions stopped working for many buyers. Discount rates rose, target valuations stayed sticky, and the bid–ask gap proved stubborn. Joint ventures offered a practical workaround, with smaller initial capital commitment, staged investment, and no requirement to put the full asset on the balance sheet at a premium moment.

Looking ahead, the rate story is not as simple as “cheaper money, more deals.” Private equity dry powder has accumulated to levels that create genuine deployment pressure, and the return of more favorable financing conditions will intensify competition for quality assets. A&M’s view is that the JV offers a different kind of value than it did when rates were high. Where it previously served as a capital-efficient workaround, it now serves as a speed advantage: a way to secure a strategic position, a technology relationship, or a market foothold ahead of a fully competitive auction process. The companies that used the high-rate period to build collaborative structures are entering 2026 with partnerships already in place, while their competitors are catching up through the same route.

Rate cycles are temporary. The partnerships built through them have a way of outlasting the conditions that made them necessary.

Regulation: Full Acquisition Has Become a Longer, Costlier Bet

For the better part of a decade, antitrust has been creeping up the list of reasons that deals do not get done. The Biden administration sharply accelerated that trend. The 2023 Merger Guidelines rewrote the analytical framework for horizontal review, expanding the categories of transaction considered presumptively harmful.[11] The new HSR premerger filing rules, which took effect in February 2025, substantially increased what parties were required to disclose at the outset of any US-reportable transaction. Although a federal district court vacated those rules in February 2026, the compliance burden created during the period they were in force has had a lasting effect on transaction planning practices.[12] In the United States, this front-loaded disclosure requirement fell on both buyer and seller regardless of whether the deal ultimately cleared. The FTC and DOJ acknowledged in their own rulemaking commentary that the new form would increase the burden on filers.[13] In practice, starting a large transaction became more expensive and time-consuming than it had been.

The numbers from the FTC and DOJ's Fiscal Year 2024 HSR Annual Report to Congress bear this out.[14] Some 1,973 transactions were reported under the HSR Act during the year, up 13.7% from FY2023. More than a quarter were valued above $1 billion. The agencies took 32 formal enforcement actions. Eighteen of those were FTC actions, and 12 of the 18 resulted in the transaction being abandoned or restructured before any court ruled. It reflects how thoroughly the threat of sustained enforcement has changed pre-signing deal calculus. Parties now make decisions about what to pursue, and at what valuation, with antitrust risk as a prominent input rather than an afterthought managed by outside counsel late in the process.

The current administration has shifted the tone. The FTC chair and the DOJ antitrust chief both signaled early that they would negotiate remedies rather than litigate every contested transaction. Pre-complaint settlements returned in volume, with five in the second quarter of 2025 alone, more than in the prior nine quarters combined, according to Dechert's DAMITT tracker.[15] The DOJ's unconditional withdrawal from its challenge to the American Express Global Business Travel acquisition of CWT was the most concrete signal, and notably the first such unconditional withdrawal in the 15-year history of the DAMITT database.[16]

What has not changed is the underlying structure of review. The 2023 Merger Guidelines remain the operative analytical framework. The disclosure expectations established by the new HSR rules, while subject to ongoing legal challenge, have reshaped how parties prepare for large transactions regardless of the rules' current legal status. And outside the United States, merger review has moved only in one direction.[17] For example, Australia's transition to mandatory pre-closing merger review took effect in January 2026. Multiple EU member states have adopted call-in powers that allow scrutiny of transactions falling below standard thresholds. Saudi Arabia and the UAE have expanded their merger control regimes. A company pursuing a cross-border acquisition of meaningful scale today may need simultaneous clearance across six or more jurisdictions, each with its own timeline, its own information requirements, and its own scope for imposing conditions. The aggregate cost (in time, legal fees, management distraction, and exposure to deal failure) has become a genuine factor in whether to pursue a full acquisition at all.

The JV does not eliminate regulatory exposure. Formations meeting applicable filing thresholds require notification in the US and many other jurisdictions, and competition authorities examine structures that concentrate market power regardless of the vehicle used. JVs between direct competitors in concentrated markets warrant particular care. That said, the analytical framework typically applied to a JV differs from that governing outright mergers, remedies tend to be more flexible, and the probability of completion is generally higher. For a board weighing deal certainty alongside strategic fit, those differences are a real consideration.

Antitrust has not made acquisition impossible. It has made it slower and less certain, and in deals where timing and momentum matter, that uncertainty has its own cost.

What This Means in 2026

These conditions are pressing on every company weighing a significant cross-border transaction. A&M’s view is that they will persist for the foreseeable future. The same urgency that makes the JV structure attractive is the condition under which JVs fail. Corners get cut, governance is simplified, and partner alignment is assumed rather than tested. The ventures A&M is seeing restructured today were mostly formed in earlier periods of similar pressure, by capable teams that underestimated what the structure actually demands. The framework that follows is designed to close that gap.

The case for the joint venture has rarely been stronger. The case for getting it right has never mattered more.

Getting Joint Ventures Right

4 Keys to Structuring Joint Ventures That Last

What follows is A&M’s framework for building ventures that last, drawn from experience advising on JV formation, governance design, and restructuring across industries and geographies. These are not abstract principles. They are the areas where the difference between a venture that creates value and one that gets unwound is most consistently found.

- Strategic Alignment

Agreeing on a market opportunity is not the same as being aligned. Two organizations can see the same JV clearly and still want fundamentally different things from it. Most JV failures trace back to assumptions that looked shared at signing but were never actually tested. A&M’s view is that partners should stress-test their alignment before a term sheet is signed. Do they want the same things from the venture in the short term? Do their long-term strategic objectives remain aligned as the JV matures? Are their underlying assumptions about market focus, competitive approach, and resource commitment genuinely compatible? If any of those answers is unclear, the term sheet is premature. Strategic alignment is necessary. It is not sufficient on its own.

Culture is the part of strategic alignment that few organizations test at formation and most regret later. People arrive at a JV carrying the loyalties and habits of their parent companies, and if no one actively builds a JV identity, those affiliations fill the vacuum. Both partners need to be willing to let the venture become something neither of them fully controls. A shared strategy means nothing if either parent is pulling the JV back toward its own culture rather than letting it develop its own. In A&M’s experience, cultural incompatibility surfaces faster than strategic misalignment and is harder to fix. A&M works with partners at formation to test cultural compatibility directly and to build the conditions for an independent JV identity before the venture launches, not after the problems surface.

- Operational Alignment

The most common operational failure in JV formation has less to do with getting the model wrong and more to do with deferring the hard decisions and leaving them for the operations team to resolve after launch. The formation team’s job is to provide clear direction on the key operational areas, including organizational structure, department leadership, and the approach to technology and systems, so that the JV leadership can focus on execution rather than relitigating parent disputes from day one. The JV should have room to refine and adapt as it finds its footing. What it should not inherit is a set of unresolved questions about the basics. Two legacy organizations each assuming their structures and systems will survive into the JV, and leaving it to the operations team to referee that dispute while simultaneously running a business, is a reliably destructive pattern that A&M sees in JV formation.

Ideally, the people making those formation decisions include the people who will live with them. Deal teams built for M&A rarely have the operational experience to make these decisions well. When the deal team transfers to an execution team reading the agreement for the first time, the institutional knowledge of where the key risks are buried goes with them. That is where the damage compounds. When that handoff happens without continuity, the JV inherits a structure its operators did not build and cannot fully explain. A&M’s view is that keeping the formation team connected through early operations is one of the highest-value investments an organization can make.

Building a cohesive culture and organization is vital for a JV's success. This includes defining the rules for parent secondees, creating compensation and incentive plans, and establishing a compelling employee value proposition. The goal is to attract and retain high-caliber talent while leveraging the JV's ownership structure to offer unique career development opportunities. A&M has a methodology for hosting cultural workshops that can help in blending and reimagining parent cultures to create a nimble and innovative JV environment.

Transition Service Agreement reliance deserves specific attention. TSAs are a necessary bridge in most JV formations, but overreliance on parent company services limits the venture’s ability to develop its own identity and operate independently. If the JV is still running on parent systems, parent processes, and parent people 12 months after launch, it never becomes its own organization. The TSA that was meant to be temporary becomes a permanent dependency, and the independent culture the venture needs to perform never materializes. A&M advises clients to plan TSA exits with the same rigor as TSA formation, defining from day one what the JV will need to stand independently and building toward that state on a clear timeline. Ventures that fail to do this typically discover the problem 18 months in, when the TSA is up for renewal and the JV has built nothing of its own to replace it.

- Governance Structure

Governance is not bureaucracy. It is the development of a framework for dispute prevention and, when necessary, efficient resolution. Well-designed mechanisms built at formation, including decision rights, deadlock provisions, escalation pathways, and buy–sell provisions, are ones that typically never need to be invoked. The goal is a governance structure so clear and so consistently applied that disagreements resolve themselves through process rather than through escalation. Because once a dispute escalates to the CFO level, both organizations are already in a bad place. Litigation is costly, visible, and damaging to both parties’ reputations. In A&M’s experience, when disputes reach that level they rarely get resolved cleanly. The options tend to narrow to capitulate, compromise badly, or unwind. None of those is a good outcome for either partner.

The most common governance failures are not unique. They are predictable. Decision rights between parent, board, and management levels are frequently left unclear. Deadlock mechanisms are often absent or too slow for the typical disagreements over budgets, capital plans, and leadership changes. Escalation pathways that sound reasonable on paper tend to collapse under the pressure of a real dispute. A&M designs governance frameworks that distinguish clearly between three levels of authority. Parent-level decisions require shareholder agreement. Board-level decisions sit with JV directors. Management-level decisions are ones the operations team can make without escalation. Each level needs clear boundaries, and the boundaries need to be tested before they are needed.

There is no single governance structure that works for every JV. A&M helps clients think through the full menu of options and choose the combination that fits their specific situation, their partners, and their industry. Independent directors with defined authorities is one lever. De-linking ownership from voting rights is another. Pre-agreed escalation mechanisms, buy–sell provisions, and deadlock resolution procedures are others. The right combination requires experience with how each mechanism performs under pressure, not just how it reads in an agreement. This is where joint venture advisory experience makes the difference. The right governance structure is the one neither partner ever has to invoke.

- Capital Requirements and Exit Strategies

The beginning of a JV is the only moment when both partners have equal leverage, equal goodwill, and equal incentive to be reasonable. What can be agreed at that moment, including capital mechanisms, funding triggers, exit terms, and valuation methodology, will be harder to agree on later and much harder under pressure. Capital requirements and exit strategy share the same underlying principle. Agree on the mechanism before anyone needs it.

On capital, the failure mode is specific and common. The JV is 18 months in, performing below plan, and needs additional funding. The partners sit down to discuss it and realize they never agreed on any of it. Will additional capital come from equity contributions? Loans from the parents and, if so, at what rate? Can the JV access external financing independently and under what conditions? Neither partner wants to dilute. Neither wants to extend credit on terms that disadvantage them. The JV cannot wait while the dispute is resolved. A&M advises clients to define capital mechanisms explicitly at formation. That means working through the triggers that require additional funding, the sequencing of funding options, the terms on which parent loans can be extended, and the conditions under which the JV can seek external financing. These are not difficult conversations when goodwill is high. They become very difficult conversations when the business needs cash.

Capital is not the only form of contribution that can shift the equity balance over time. Partners in many JV structures contribute assets, intellectual property, or products on an ongoing basis, and those contributions create value that was not anticipated in the original equity split. Without a mechanism agreed at formation for rebalancing when contributions change, a partner who brings significant new value into the venture has no clear path to being compensated, and the dispute that follows is as difficult to resolve as any cash-based disagreement.

An example could be a JV between a pharmaceutical company and a consumer retail business. If a product moves from prescription to over-the-counter and enters the JV, the contributing partner has added meaningful value that did not exist at signing. Without a pre-agreed process for how that contribution is valued and how the economics adjust in response, the conversation quickly becomes contentious. A&M advises clients to think through contribution scenarios at formation and build rebalancing mechanisms before they are needed. That means agreeing on how noncash contributions are valued, what thresholds trigger a rebalancing discussion, and how disagreements about value get resolved. The logic is the same as it is for cash: Agree on the mechanism before anyone needs it.

On exit, the same logic applies. Partners do not need to agree on what the JV is worth today. The more productive question is how they will determine value when the time comes. That means aligning on valuation methodology, the relevant multiples, the independent auditor, and the process. It also means agreeing on who can ask for an exit and when, on what grounds, and through what trigger mechanism. And it means agreeing on how the exit executes. A right of first offer, a right of first refusal, a drag-along, and a third-party sale each carry materially different implications for both partners and the JV itself, and those differences matter far more when one party wants out than when both are aligned. Think through those implications before either partner has a reason to want out. A&M helps clients design capital and exit frameworks that reflect the specific structure of the venture, the risk appetite of both partners, and the realistic range of outcomes that the JV might produce.

The Bottom Line

What the best JV practitioners share is not a formula. It is a disposition, the willingness to do the hard work at the front end of a venture that makes the back end manageable. The companies that treat the complexity premium as an investment rather than an overhead cost are the ones still running their ventures a decade later. The work is harder than most organizations expect. When the foundation is right, the venture lasts.

How A&M Can Help

A&M’s Corporate Transactions Group has deep experience advising on joint venture formation, governance design, and restructuring across industries and geographies. The concepts described in this publication, and the four keys to structuring ventures that last, are not observations from the outside. They are the patterns A&M has identified through direct experience working on these structures across sectors and market cycles.

By combining operational, financial, accounting, tax, and industry expertise, our global team engages directly with clients at every stage of the JV lifecycle. Organizations call us at formation, when the structure needs to be designed to last rather than just to close. They call us during the venture’s operating life, when governance gaps surface before they become disputes. They call us at exit, when the terms that were not agreed at the outset need to be negotiated under pressure. If your organization is considering a joint venture, restructuring an existing one, or navigating the exit from a venture that has run its course, we welcome the conversation.

Note on Sources and Scope

The data and analysis presented in this publication draw on publicly available sources including government reports, regulatory filings, financial market data providers, and named third-party research. Individual source citations, including author, title, date, and URL where available, are provided in the footnotes accompanying each data point throughout the document.

The analysis, conclusions, and perspectives expressed in this publication are those of Alvarez & Marsal alone and do not represent the views of any data provider or third party cited herein. This publication is intended for general informational purposes only and does not constitute legal, regulatory, financial, or investment advice. The regulatory and legal observations contained herein reflect publicly available information as of the date of publication and are general in nature. Laws, regulations, and enforcement practices vary by jurisdiction and change over time. Nothing in this publication should be relied upon as legal or regulatory guidance applicable to any specific transaction or situation. Readers should consult qualified legal and financial advisors regarding their specific circumstances.

[1] Matthew Toole et al., “The State of Global M&A: 2026,” Report, LSEG Data & Analytics, accessed March 31, 2026. Mega-deal count (68 transactions above $10 billion) per LSEG Deals Intelligence league table data, as reported by Reuters, January 6, 2026.

[2] Nick Patience, “AI Capex 2026: The $690B Infrastructure Sprint,” Futurum Group, February 12, 2026.

[3] “M&A: 2025 in Review and a Look Ahead to 2026,” Cleary Gottlieb, January 7, 2026.

[4] “Remarks: Donald Trump Announces AI Infrastructure Initiative - January 21, 2025,” Roll Call, January 21, 2025. The $500 billion figure represents the total stated investment commitment announced at launch. Actual deployed capital may differ materially from stated commitments, and the structure and ownership of the venture may evolve over time.

[5] “State of U.S. Tariffs: April 15, 2025,” The Budget Lab at Yale, April 15, 2025. Tariff rate calculated using U.S. International Trade Commission DataWeb.

[6] Congressional Research Service, “Presidential 2025 Tariff Actions: Timeline and Status (R48549),” Congress.gov., Updated January 12, 2026. The 145% rate on Chinese imports reflects cumulative IEEPA executive orders (February–April 2025). China imposed retaliatory tariffs of 125% on US goods.

[7] Robert McClellan and John Wong, “TPC Tariff Tracker,” Tax Policy Center, Urban Institute & Brookings Institution, March 10, 2026. Trade volume figures derived from U.S. Trade Representative data on total annual goods imports subject to 2025 tariff actions.

[8] Learning Resources, Inc. v. Trump, 607 U.S. ___ (2026), Decided February 20, 2026. The Supreme Court held in a 6–3 decision that IEEPA does not authorize the President to impose tariffs.

[9] Whitehouse.gov, “Imposing a Temporary Import Surcharge to Address Fundamental International Payments Problems,” Presidential Proclamation, February 20, 2026, issued under Section 122 of the Trade Act of 1974. The proclamation imposed a 10% global tariff effective February 24, 2026, for 150 days.

[10] “Federal Reserve issues FOMC statement,” Press Release, Federal Reserve, December 10, 2025. The Federal Open Market Committee reduced the federal funds rate by 25 basis points to a target range of 3.50%–3.75%, the third consecutive rate reduction.

[11] U.S. Department of Justice, Antitrust Division, “2023 Merger Guidelines, December 18, 2023. The guidelines remain operative under the current administration. See Federal Trade Commission, “FTC Chairman Andrew N. Ferguson Announces that the FTC and DOJ’s Joint 2023 Merger Guidelines Are in Effect,” Press Release, February 18, 2025.

[12] Federal Trade Commission and Department of Justice, “Premerger Notification; Reporting and Waiting Period Requirements,” Federal Register 89, no. 218 (November 12, 2024): 89216–89414. Effective February 10, 2025. Note: A federal district court vacated the updated HSR form on February 12, 2026, with a seven-day stay pending further proceedings. The status of the rules should be confirmed with qualified legal counsel before reliance on any specific disclosure obligations.

[13] Federal Trade Commission, “FTC Finalizes Changes to Premerger Notification Form,” Press Release, October 10, 2024. See also 89 Fed. Reg. 89215 (November 12, 2024). For current status of these rules, see footnote 12.

[14] Federal Trade Commission with Department of Jusstice, “Hart-Scott-Rodino Annual Report, Fiscal Year 2024,” Federal Trade Commission, September 17, 2025.

[15] Dechert Antitrust Merger Investigation Timing Tracker (DAMITT), Dechert LLP, Q2 2025 Report (July 2025) and 2025 Annual Report (January 2026).

[16] “Amex GBT Announces Dismissal of US Department of Justice Lawsuit Challenging CWT Acquisition,” American Express Global Business Travel, July 29, 2025. The DOJ voluntarily dismissed its complaint without conditions, the first such unconditional withdrawal recorded in the DAMITT database.

[17] See Jean-Francois Bellis and Porter Elliott, “Merger Control 2025: Global Practice Guide,” Chambers and Partners, Last updated July 12, 2025. Australia: Treasury Laws Amendment (Mergers and Acquisitions Reform) Act 2024 (Cth), effective January 1, 2026. UAE: Federal Decree-Law No. 36 of 2023; Cabinet Resolution No. (3) of 2025. Saudi Arabia: General Authority for Competition, 2024.