Tax Cuts and Jobs Act Impact on Compensation and Benefits

The Tax Cuts and Jobs Act (the Act) is the most significant change to the U.S. tax law since 1986. Although much of the focus is on “bigger ticket” items, such as moving to a more territorial-type tax system and taxation of “pass-through” entities, the Act contains numerous compensation and benefit provisions and considerations which should not be overlooked. This article highlights a few of the impacts of the Act on compensation and benefits and what taxpayers must consider to fully comply with the new provisions.

$1 Million Limitation under Section 162(m)

Prior to the Act, Section 162(m) limited the deduction for compensation paid to “covered employees” of a publicly-listed company to $1 million unless the compensation was “qualified performance-based compensation.” Most public companies relied heavily on this exception to deduct compensation paid to their top executives. The Act, however, made the following changes:

- Repealed the performance-based exception, so any compensation in excess of $1 million is no longer deductible.

- Expanded the definition of “covered employee” to also include the CFO and covered employees from a prior year (starting with 2017 covered employees – i.e., “once a covered employee, always a covered employee”).

- Expanded the definition of “publicly held corporation” to also include companies with publicly-traded debt and certain foreign private issuers.

These new rules apply to taxable years beginning after 2017; however, included in the new law is a provision which exempts compensation payable under a written, binding contract effective November 2, 2017. It is currently unclear how broadly this grandfathering provision will be applied.

Downward discretion is a common provision contained in many performance-based compensation arrangements. Many believe that such potential discretion negates any binding contract argument that could otherwise be made. It is also unclear exactly how the grandfathering will work for the newly included CFOs and corporations added to the rules. The implications could also be huge for companies in their three-year IPO transition period and for companies with significant post-employment compensation, such as deferred compensation.

We are still waiting for guidance from the Treasury and the IRS on how this grandfathering provision applies, which is expected this summer. In the meantime, we recommend continuing to go through the normal Section 162(m) certification process as to not jeopardize any potential grandfathered amounts.

In light of the new rules, it is still uncertain what changes companies will make to compensation arrangements on a go-forward basis. Under the old Section 162(m) rules, it was advantageous from a tax perspective to grant performance-based compensation that did not count towards the $1 million limit. With that benefit removed, some companies may choose to pay more guaranteed compensation such as base salary rather than at-risk pay since there is no tax incentive to structure it as performance-based. Netflix did just that by announcing elimination of their annual bonus in exchange for significantly higher base salaries. The company’s public filings announcing this change acknowledged that it was a direct result of Section 162(m) modifications in the Act. We think the Netflix example will be an anomaly since companies will still need to consider the views of their shareholders and shareholder advisory firms such as Institutional Shareholder Services (ISS) and Glass Lewis. Generally speaking, shareholders are in favor of performance-based compensation so the executives’ interests are aligned with their own.

With the expansion of the covered employee definition to include all covered employees in 2017 and later years, companies may re-think their severance arrangements. Currently, lump-sum severance payments are common since they are usually paid after termination when an executive is no longer a covered employee under the old rules. However, it may now be advantageous to spread out payments over several years since the $1 million limit resets each year. Additionally, companies will need to be aware of potentially unintended consequences of individuals moving in and out of their covered employee population when a particular executive receives higher than normal compensation during a year (e.g., strong bonus year, sign-on equity grants, etc.).

The change to Section 162(m) is arguably the biggest change in the Act related to executive compensation, and time will tell on how companies adjust to the new rules.

Impact of Tax Rate Decreases

As part of the Act, the corporate tax rate was reduced to 21 percent from 35 percent. On the individual side, the top marginal tax rate was also reduced from 39.6 percent down to 37 percent. Below are three ways the decrease in both the corporate and individual tax rates may impact compensation and benefits:

1. Deferred Tax Assets

- As book expense is recognized for equity awards granted to employees, a deferred tax asset (DTA) is typically set up if the company expects to receive a tax deduction for those awards down the road at the tax event (e.g., vesting, exercise, etc.). Prior to the Act, these DTAs were set up assuming a corporate rate of around 35 percent. However, with the reduction in the corporate tax rate to 21 percent, companies will have significant income tax expense adjustments on their income statements. Now is the time to check that your DTAs are accurate. We’ve seen several auditors focus on these DTAs and ask additional questions to ensure that the proper adjustments have been made.

- The interplay with the new Section 162(m) is another important consideration. Historically, DTAs may have been set up for awards where the company may no longer receive a deduction due to the changes to Section 162(m) discussed above. For example, DTAs may have been set up for CFOs and other individuals who were not expected to be covered employees at the tax event, but will now be pulled into these rules due to the “once a covered employee, always a covered employee” concept. Accordingly, it is crucial for companies to review their DTA balances for equity-based compensation and determine if a new methodology for establishing future DTAs is needed given the new Section 162(m) rules.

2. Incentive Stock Options

- In the past, incentive stock options (ISOs) were a common equity vehicle used to compensate employees in a tax-favored manner. However, ISO use fell, in part, due to the treatment of related gains as an alternative minimum tax (AMT) preference item. The Act increased the AMT exemption amount and significantly increased the phase-out threshold for AMT. Accordingly, ISOs may now be more attractive because more ISOs will be eligible for the tax-favored treatment thanks to the increased AMT limits. While the employer loses the deduction for ISOs, at a 21 percent corporate tax rate, the loss may be more tolerable than with the previous 35 percent corporate rate.

- However, the use of ISOs requires adhering to a number of conditions, including a) meeting holding requirements (1 year after exercise and 2 years after grant) and b) $100,000 per year exercise limit. Keep in mind that ISOs have not been a prevalent vehicle in recent years so additional employee communication could be needed on how the long-term incentive vehicle works.

3. Withholding on Compensation

- While the number of tax brackets remained the same, rates have decreased overall with the top rate falling from 39.6 percent to 37 percent. Employees will need to rethink their tax withholding for various changes including, but not limited to the following:

- Repeal of personal exemptions;

- Increase in the standard deduction;

- Changes in tax rates and brackets;

- Elimination or restriction of itemized deductions; and

- Increase in the child tax credit.

- The IRS released the 2018 Form W-4 on February 27, 2018, which addresses the various law changes. The IRS is generally not requiring employers to obtain new W-4s from their employees since it revised the withholding tables to function with the old W-4 for 2018. However, given all the changes in the tax law, employees may want to submit new Form W-4s to confirm their current withholding rate is appropriate.

- Also, the IRS clarified in Notice 1036 that the optional flat withholding rate for supplemental wages (e.g., restricted stock vesting, annual bonuses, etc.) of $1 million or less has been adjusted to 22 percent while the mandatory withholding rate for supplemental wages in excess of $1 million changed to 37 percent.

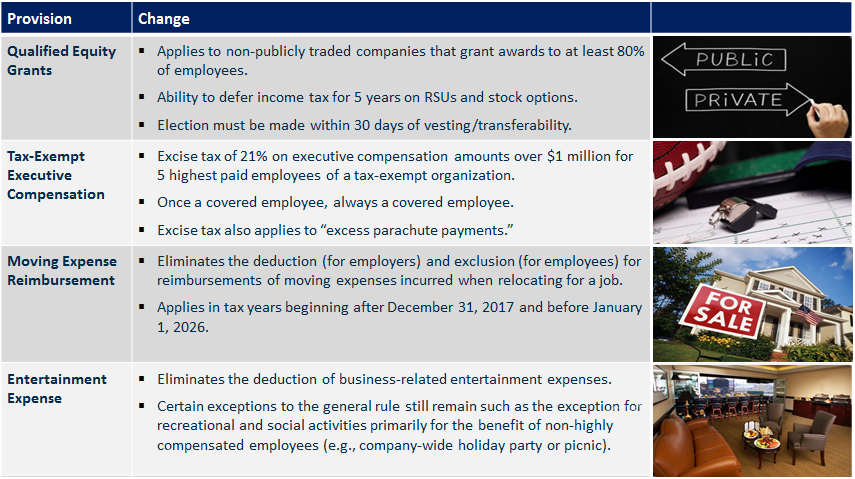

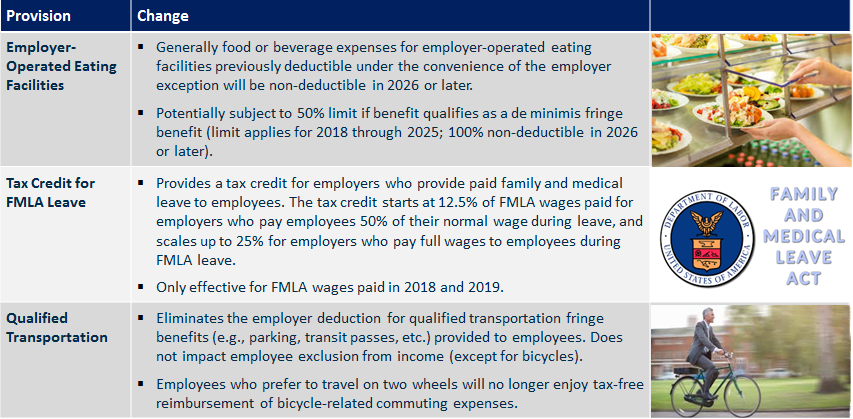

Miscellaneous Compensation & Benefit Provisions

The Act also contained a host of other provisions that will impact compensation and benefits. Below are just a few of the changes made by the Act:

Now What?

The Act constitutes a substantial overhaul of the U.S. tax laws, which directly impacts how companies will compensate their employees. We are still waiting for the dust to settle to get a lay of the land post-tax reform. In the meantime, companies should try to get their arms around the potential consequences while we all wait for additional guidance.