Canada’s Private Capital Outlook 2026: Infrastructure, Insight, and Operational Alpha

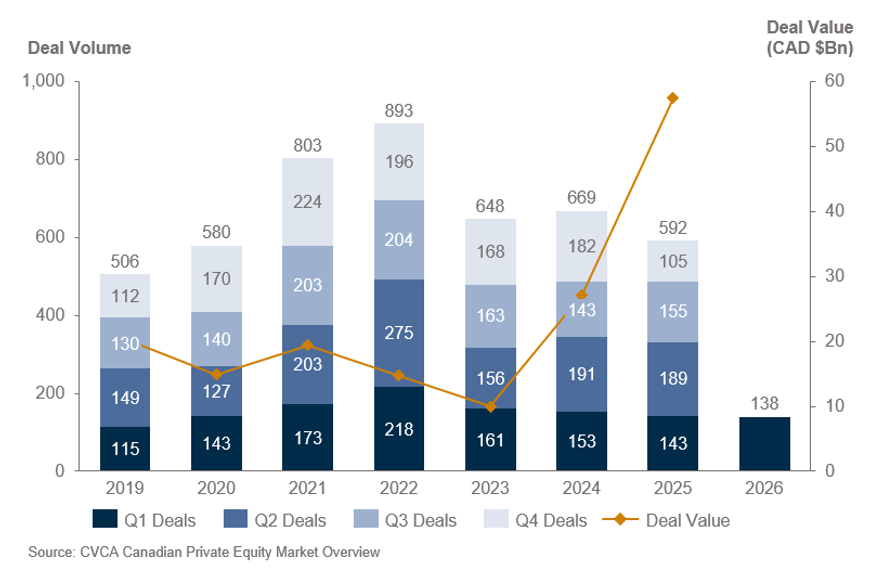

Fewer Deals, Larger Commitments: Canadian Private Equity (PE) Mergers and Acquisitions Value Rebounds on Megadeals Despite Subdued Transaction Activity

Canadian private capital enters 2026 in a state of disciplined optimism. The environment is more selective, more data-driven, and significantly more execution-focused than in prior cycles. Deal flow remains below past highs, but capital deployment is far from muted. In fact, dollars are concentrating into fewer, higher conviction investments, with 2025 headlined by major transactions such as Garda World Security’s $14 billion recapitalization; CI Financial being taken private by Mubadala Capital for $12 billion; and CDPQ’s agreement to acquire Innergex Renewable Energy for about $10 billion.[1] Sponsors are leaning into scale or platform investments where the thesis is compelling, even as the broader mid-market activity remains measured.

Chart 1: PE M&A in Canada (2019—Q1’2026)

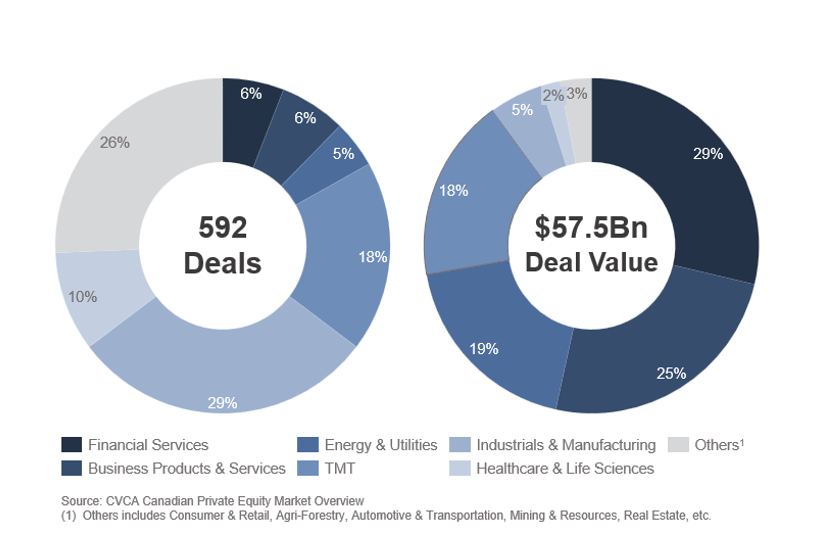

Business services, financial services and energy and utilities accounted for about 72% of total value in 2025, representing a disproportionate share and reflecting both the capital intensity of transactions in these industries and their role in supporting long-term economic and supply chain priorities.

Chart 2: PE M&A in Canada by Sector (2025)

Persistent macro volatility has raised the level of work required to get comfortable deploying capital. As a result, investors are spending more time validating assumptions, testing downside scenarios, and engaging earlier on execution risk. At the same time, record levels of dry powder and Limited Partner (LP) liquidity pressure have delayed deployment rather than reduced appetite, with sponsors waiting for clearer signals on pricing, exits, and macro direction before re-engaging more competitively.

These dynamics are reshaping where capital is being deployed, how risks are underwritten, and how returns are ultimately generated. Infrastructure represents one of the most attractive areas for scaled deployment, reinforced by ongoing policy momentum. Due diligence has become critical for price discovery, conviction, and differentiation. Broad confirmatory exercises are giving way to focused, hypothesis-driven work that rigorously tests the operational and commercial drivers that determine outcomes. Operational value creation has emerged as the primary source of alpha as gains from leverage and multiple expansion recede. Investors who align capital deployment to these priorities and build the capability to execute against them will be best positioned to outperform in a market that increasingly rewards discipline, evidence and delivery.

Energy and Infrastructure: A Key Deployment Engine for the Next Investment Cycle

Canadian Private capital is pivoting to energy and infrastructure, not only from dedicated infrastructure funds, but also from PE sponsors seeking assets with infrastructure‑like characteristics, including contracted revenues, regulated pricing, and resilient demand. This reflects both the size constraints of traditional buyouts and the relative scarcity of large‑scale opportunities in Canada.

Policy momentum is reinforcing this shift. Budget 2025 allocates approximately $115 billion to federal infrastructure over the next five years, focused on core public infrastructure, healthcare and housing.[2] In parallel, the Major Projects Office, established in August 2025, is implementing a “one project, one review” framework, targeting approval timelines of roughly two years, while coordinating financing with Crown Corporations. In recent news, Prime Minister Carney also announced the Canada Strong Fund, Canada’s first national sovereign wealth fund, which will invest in strategic areas alongside the private sector. Together, these reforms are aimed at compressing timelines, reducing regulatory uncertainty, and materially improving the risk-return profile for private capital.

The need for capital is both wide and deep. Canada’s massive government commitment creates multi-year pipelines across transit, clean power, broadband, and digital infrastructure. This was already evidenced in deal numbers in 2025, in which transactions in energy and natural resources rose 133% from the year prior.[2]

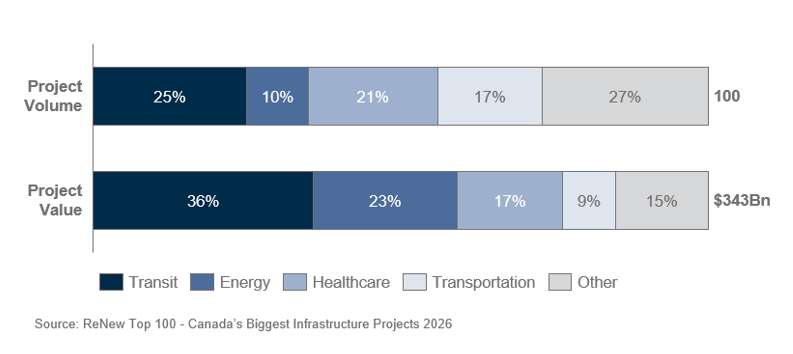

Canada’s top 100 infrastructure pipeline expanded materially, with total project value rising from about $300 billion in 2025 to about $343 billion in 2026, driven by large nuclear and transit programs that align with private capital’s preference for scale, durability, and inflation-linked economics.[3]

Within this expending pipeline, three sub-sectors are primed for private capital deployment:

- Transit: Revenues are typically supported by long-term contracts or payment structures backed by public entities. While not risk-free, these structures limit exposure to demand volatility and provide clear visibility into long-term cash flows.

- Energy Transition (including nuclear): Clearer permitting, standardized regulatory pathways and structured public cofinancing improve visibility into execution risk in areas such as nuclear refurbishment, grid modernization and clean power buildouts.

- Healthcare: Initiatives focus on advancing the modernization of essential, government-backed care infrastructure with resilient demand, delivering stable cash flows and downside protection through cycles.

Chart 2: Top 100 Infrastructure Projects in Canada (2026)

In a market full of volatility, infrastructure is standing out as a source of dependability. Long duration contracts, scale, and predictable cash-flows are driving renewed momentum into the sector. Geoff Hayes – Managing Director, TAG - Energy & Infrastructure |

Investor Behaviour is Converging with These Dynamics: A recent infrastructure investor study shows that nearly 50% of surveyed LPs plan to increase infrastructure allocations over the next 12 months, with a pronounced shift toward core-plus and value-add strategies. For example, about 47% intend to increase core-plus approaches and approximately 37% intend to boost value-added strategies, compared with only about 14% focused on core initiatives.[4], [5]

This is pushing infrastructure General Partners (GPs) into core-plus and value-add opportunities, historically the domain of private equity, driven by the pursuit of higher return profiles, operational value creation, and growth exposure within essential-service platforms.

This pattern is also extending into infrastructure adjacent sectors such as business services, industrial and engineering services, and tech-enabled products and services platforms that support construction, maintenance, and operations. These businesses occupy mission critical roles in delivery chains yet offer opportunities for operational upgrades, digital transformation, and pricing optimization, allowing managers to capture above core returns with infrastructure-like resilience.

In short, Canada’s accelerating energy and infrastructure agenda is not just a policy priority; it is becoming an increasingly attractive deployment engine for private capital, offering scale, stability, and long-term alignment at a moment when visibility and downside protection are at a premium.

Due Diligence: From ‘Checking-the-Box’ to ‘Pressure-Testing the Plan’

Canadian private capital investors are redefining what rigorous due diligence means in an environment marked by higher valuation multiples on platform acquisitions, tighter lender scrutiny, and increased geopolitical and regulatory uncertainty. Longer hold periods and larger platform investments, despite slower deal volumes, have increased the importance of integrated, hypothesis‑driven diligence.

Leading investors are moving beyond traditional financial and tax reviews to a unified diligence process that integrates operational, commercial, IT, AI, cybersecurity, human capital, and Environmental, Health and Safety workstreams. The objective is sharper underwriting: connecting systems constraints and organizational capacity directly to the profit and loss, capex requirements, and value creation timing so that underwriting reflects how value will be realized post-close, not just what it could be in theory. This approach clarifies the structural investments, sequencing, and leadership capacity required to deliver the thesis, giving investment committees more conviction when approving capital.

A robust and pragmatic value creation plan has become a differentiator for investors. The strongest processes are explicitly hypothesis driven; investors articulate testable theses around scalability, margin expansion, price realization, integration synergies, regulatory friction points, and technology enablement. This mirrors a Canadian trend in which commercial and operational diligence, when integrated into a cohesive growth plan, has become a decisive driver of returns as competition intensifies, particularly in carve‑outs and add‑ons.

The biggest risk in deals today is not missed upside. It is untested assumptions about customers, pricing, and execution. Integrated diligence pressure tests whether the value creation plan holds up under real operating constraints, not just on paper Vipul Soni – Senior Director, Commercial Diligence & Strategy |

Primary input is increasingly non-negotiable: Industry operators have become a vital piece of due diligence, particularly when it comes to infrastructure and other regulated or capital-intensive assets. Embedding operators from Day One enables real‑world testing of market assumptions, operational feasibility, supply chain constraints, and technology readiness. Operator insight closes the gap between deal models and operating reality, resolves intricate questions that often stall bids late in the process, and increases underwriting accuracy and confidence.

Sell-side sophistication is catching up to buy-side depth: More vendors are running commercial and operational diligence ahead of a sale to strengthen the equity story, quantify value drivers, and anticipate buyer concerns around growth, risk, and capital needs. This trend is accelerating as Canadian PE sponsors seek to time the market and execute opportunistic exits, often after holding assets longer than usual. When sell‑side materials present a credible, evidence‑based path to value, buyers respond with tighter spreads between indicative and final offers, greater underwriting confidence, and faster execution. This often expands the buyer universe to include cross‑border sponsors.

A&M Case Study A cross‑functional Alvarez & Marsal team worked alongside an infrastructure fund on an integrated buy‑side diligence of an energy sector asset with a complex, multi‑site operating model. The business operated across varied commercial and regulatory environments, with differing feedstock procurement structures and production efficiency profiles by site. A&M led a coordinated commercial, operational, financial, tax, and technology diligence, aligning findings into a single, integrated view of the asset’s earnings profile and growth plan. This one‑firm perspective highlighted key sensitivities and execution risks, enabling the investment team to underwrite the opportunity with greater confidence and precision. |

Operational Value Creation: The Default Source of Operational Alpha in the Next Cycle

In this changing investing landscape, operational value creation has become a key durable source of operational alpha. LPs are reinforcing this shift: capital is flowing toward sponsors who can articulate clear, thesis led operating plans and demonstrate consistent, execution across the life of the investment. GPs have accordingly shifted their focus, some moving down market to more traditional mid-market investing, allowing for a clearer path to value creation in new investments; and many investing in operating talent and data management capabilities.

Operational improvement, not financial engineering, is carrying returns: With elevated financing costs and intense competition, investors are zeroing in on systematic operational plays that strengthen profitability, resilience, and scalable growth. Recent analysis by StepStone suggests earnings growth and margin expansion can drive roughly 3.3 times more unlevered value creation than multiple expansion, reinforcing that the next cycle will reward operators, not observers.[6] For sponsors, this means building repeatable playbooks across multiple operational efficiency areas, including pricing, procurement, SG&A efficiency, and working capital management, and pursuing them across their portfolio.

Operational improvement is no longer optional. The best sponsors ensure real, sustained gains in margin and growth, and understand this as the path to long-term success. Matti Keskikyla – Managing Director, Performance Improvement |

Diligence is evolving into a value-focused discipline: Investors are increasingly using data, predictive analytics, and sector expertise to pinpoint and underwrite the specific operational performance levers most likely to drive value. This shift transforms diligence from confirmatory analysis into an early-stage blueprint for execution. Firms with sophisticated, data-led operating models are now widening the performance gap versus peers: they enter ownership knowing not only where value will come from, but how to unlock it with precision.

LPs are benchmarking execution, not narratives: In today’s liquidity‑constrained environment, attractive stories no longer clear committees. LPs are demanding documented operating plans with measurable key performance indicators, including EBITDA milestones, cash generation targets, and line‑of‑sight to distributions to paid-in capital. Track record now matters as much as strategy: sponsors who consistently deliver against their plans are increasingly advantaged in fundraising cycles, co-invest partnerships, and extension vehicle approvals.

Operational resourcing is being rewired for impact: While some larger GPs are expanding in-house operating teams with deeper sector expertise, digital and analytics capability, and transformation experience, the market is not shifting uniformly toward vertically integrated value creation groups. Mid-market sponsors are increasingly relying on specialized operational consultants to access the same depth of expertise without the fixed cost of fully staffed internal teams. These consultants are being embedded earlier in the deal cycle to run hypothesis led diligence sprints, pressure test operational feasibility, and accelerate Day One execution. Even at scale, many large platforms continue to supplement internal teams with external specialists to flex capacity, expand capability, or deploy bespoke playbooks. The result is a more modular, industry‑focused approach to value creation that blends in‑house talent, external specialists, analytics, and execution rigor into a repeatable source of returns.

A&M Case Study A sponsor‑backed portfolio company in the automotive sector had grown rapidly through acquisitions but struggled to translate that growth into performance as integration lagged and complexity increased. Working alongside management, the A&M operations and performance improvement team helped identify and lead a focused set of value levers, with integration at the center of the agenda. As execution tightened, margins improved sustainably and the business began to present as a more cohesive, scalable platform. The sponsor is now positioned for a successful exit, having grown the business more than threefold while expanding profitability by over 40% and strengthening the foundation for long‑term value creation. |

[1]GardaworSld, CI Financial, Innergex

[2]The Logic: Canada lags global M&A but outpaces US in strategic deals in 2025

[5]LP Perspectives 2026 | Infrastructure Investor

Contact our experts