Production Cuts Expected to Continue in 2023, with No Clear End in Sight for the Chip Shortage or Supply Chain Issues; Macroeconomic Forces Creating Uncertainty for Vehicle Sales

Production shutdowns and delays continue to persist among the industry, as automakers and suppliers have been enduring harsh operational conditions for over two consecutive years. Automotive inventories saw a noticeable increase, while month-over-month sales remained flat on an unadjusted basis. Rising interest rates, reduced vehicle affordability and general economic uncertainty have started to cloud the picture for new vehicle sales heading into 2023.

In this issue, A&M analyzes the changing structure of sourcing strategies in the new era of electric vehicles (EVs) for original equipment manufacturers (OEMs) as the selected topic for the October Industry Focus.

In transaction news, OEMs and suppliers continue to strategically position themselves in accelerating the growth of global EV adoption and self-driving technologies.

In regulatory news, New York is adopting legislation originally proposed by the state of California, which bans the sale of gas-powered vehicles by 2035. Additionally, Nikola Corporation founder, Trevor Milton was convicted on several counts of fraud by a U.S. jury verdict.

Additional October insights are included below.

Financial Performance

Auto Forecast Solutions’ (AFS) latest numbers show that shutdowns and delays have resulted in approximately 3.5 million lost vehicles globally during calendar year 2022. Although the chip shortage and supply bottlenecks have begun to ease, semiconductor and supply chain issues are unlikely to be resolved in the near-term and are expected to continue to affect production in 2023. In addition to the vehicles lost year-to-date, Hurricane Ian could result in a further increase of lost vehicles ranging from 30,000 to 70,000 cars. The latest AFS estimates suggest approximately 4.4 million total cars and trucks will be affected by chip-related disruptions in 2022.

As the world transitions to EVs, consumers have faced a number of challenges that include elevated vehicle prices, low affordability, increased fuel costs and a limited charging infrastructure for their EVs. EV makers and charging companies are working to address and solve many of these issues through subscription-based and pay-as-you-go business models. Nissan and EVCS have recently launched these plans, offering flexible lease programs for low-mileage consumers and a flat-rate subscription yielding access to a charging network for high-mileage EV drivers.

Industry Update

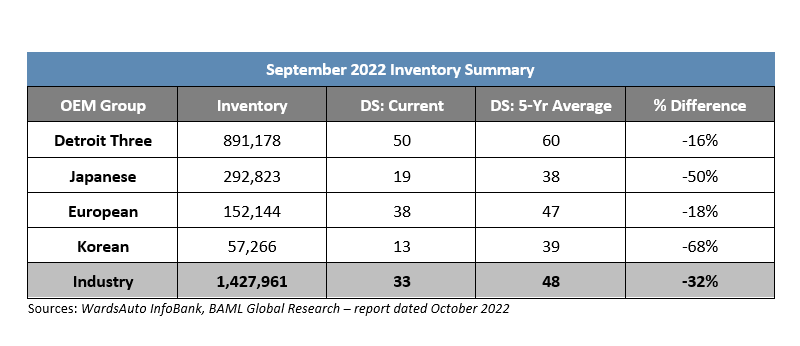

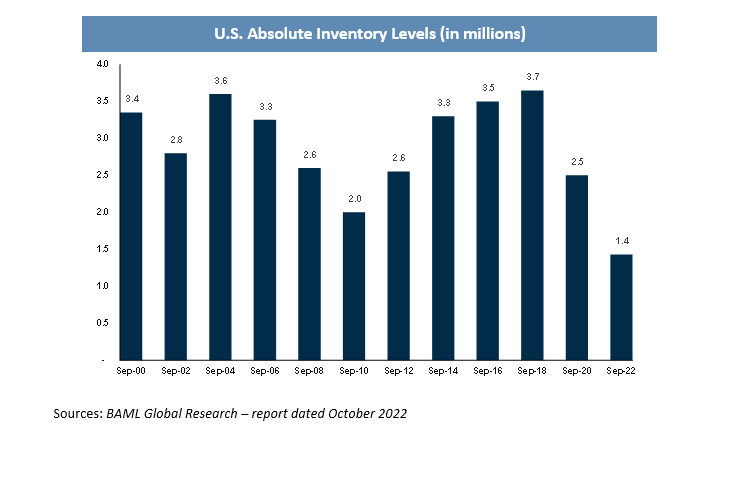

Automotive inventory increased by 160,000 units in September, resulting in approximately 1.43 million total units. This translates to a days’ supply (DS) that is 32 percent below the five-year average at 33 DS. Rapidly rising interest rates and persistent inflationary conditions may continue to reduce consumer demand for vehicles and increase unit volumes on hand. Despite adverse economic circumstances, inventories have made a significant recovery from the September 2021 level of roughly 970,000 vehicles but remain well below the industry’s normal range of 2.5 million to 3 million units.

New light vehicle sales in the U.S. increased 10 percent year-over-year in September with a 13.5 million seasonally adjusted annualized rate (SAAR) of sales, while the full-year sales pace is tracking at 13.6 million units. Although the sales pace increased month-over-month from the August SAAR of 13.2 million, the monthly SAARs continue to trend towards recessionary levels. Average transaction prices also increased year-over-year in September, resulting in a 5.7 percent increase to $44,942 per vehicle.

Industry Focus – OEM Sourcing Strategies

While OEMs and suppliers continue to move towards electrification, they are simultaneously battling unfavorable industry conditions and undergoing major operational shifts, coupled with increased vehicle demand. A critical operational component of the vehicle supply chain consists of parts and material sourcing, which has several changing dynamics.

In this month’s industry focus section, A&M explores several different methods that OEMs are utilizing to source key materials for improving production in the short-term and streamlining EV manufacturing processes for the future.

In-Sourcing

After several decades of outsourcing production of more and more component parts and systems to suppliers, auto makers are entering into a new era, which necessitates a unique approach for acquiring new parts and establishing different sourcing methods. Since the onset of COVID, millions of vehicles have been lost in production and countless plant shutdowns have occurred due to the semiconductor shortage and global supply chain issues. One solution OEMs have since undertaken involves in-sourcing chips or creating business plans for bringing chip manufacturing in-house.

Tesla pioneered the movement of in-sourcing semiconductor manufacturing, which proved to pay dividends through the pandemic-era. Despite still being affected by the chip crisis, Tesla was able to mitigate supply bottlenecks and production issues more efficiently than most OEMs. The semiconductor industry is heavily dependent on Asia for both the parts and production of chips, which has led to several other auto makers announcing their intentions to bring chip production internal. GM plans to develop its own chips by 2025 to lower costs and scale volume, as the OEM works to grow its autonomous driving unit, Cruise. Hyundai and Ford are also among those working to develop their own chips, through affiliate Hyundai Mobis and partner GlobalFoundries, respectively.

OEMs have also taken a new approach for in-sourcing, which has resulted in the creation of circular economies. Car makers are under heavy pressure to navigate fractured supply chains and elevated raw material and energy prices that have limited their access to already scarce materials. Several auto makers, including Stellantis and Renault, plan to utilize this new strategy by remanufacturing, repairing, reusing, and recycling vehicle parts and materials in a closed loop setting. By doing so, Stellantis and Renault will extend the life of vehicles and their component parts, build sustainability, and aim to generate $2 billion and $2.2 billion in revenue by 2030, respectively.

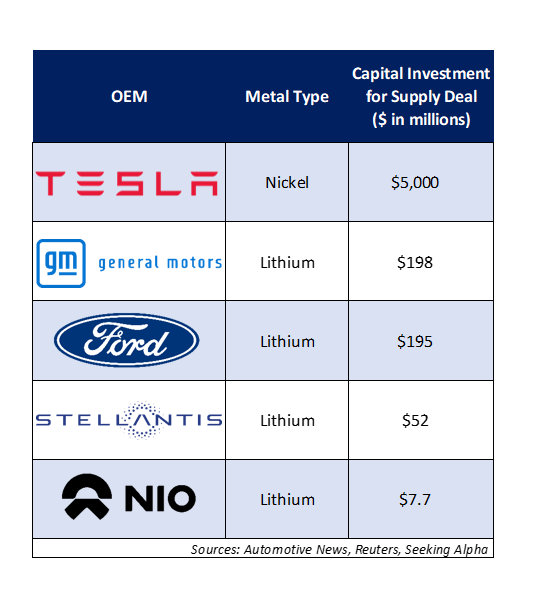

Additionally, in anticipation of the high consumer demand for EVs, several auto manufacturers have recently started to establish partnerships with mining companies to secure supply of crucial metals for EV batteries such as lithium, nickel, and cobalt. The table below illustrates several OEMs that have recently struck supply deals for these key resources, and the respective capital investment amounts.

In-sourcing will allow OEMs to maintain control over vital parts of their supply chains and reduce their dependency on external suppliers and influence from other industries, such as personal computers. Also, utilizing in-sourcing strategies enhances value creation, increases the scale of production, and secures the supply of scare materials and component parts. OEMs have clearly determined if they are to achieve targets established for meeting certain production goals for EVs and comply with mandates for phasing out internal combustion engine vehicle sales, they must move to an in-house strategy for manufacturing parts and securing supplies of raw materials critical to EV production, while also driving cost savings, supply chain reliability and achieving ESG goals.

Alternative Sourcing Strategies

In addition to in-sourcing, OEMs are also engaging in other strategic alternatives to drive innovation and boost the production of EVs, particularly in the area of battery production and recycling. In an industry that has experienced high levels of volatility for consecutive years, OEMs are looking to partnerships to improve their current sourcing methodologies and establish supply chains for their electric vehicles.

While some auto makers have moved battery recycling in-house, others have formed partnerships with battery recyclers such as Redwood Materials and Li-Cycle. From legacy OEMs to EV startups, Redwood Materials and Li-Cycle have joined forces with Audi, Volkswagen, Toyota, Arrival and others. Battery recycling is a critical component of EV supply chains, helping to reduce carbon emissions and accelerate global EV adoption.

Alternatively, Volvo and Renault have taken different approaches to scaling their electric vehicle businesses. In conjunction with its Chinese parent company, Volvo has created a joint venture specializing in the powertrain business. The JV, Aurobay, aims to consolidate its legacy auto manufacturing business with its electric business unit, to improve hybrid-combustion technology, reduce costs and add scale. Conversely, Renault has joined forces with Vitesco Technologies as the OEM seeks to design and manufacture power electronics and motors in-house. The partnership is mutually beneficial and will allow Renault to build a scalable platform for its EVs, while Vitesco receives purchase contracts and improves its competitive positioning in the electric supplier space.

Throughout the automotive industry’s transitionary phase, initiatives to insource production and form partnerships with other companies to secure supply of critical materials will have a significant impact on automotive supply chains. At the same time, legacy sourcing strategies will continue as OEMs continue to manufacture and assemble internal combustion engine vehicles. Eventually these will merge into a new supply chain, creating both opportunities and risks for suppliers, especially those involved in propulsion systems.

Transaction Activity

In recent transaction news, BMW and Mercedes have announced their plans to collaborate with Amazon Web Services and Microsoft Cloud, respectively, to collect, analyze, and process vehicle data for developing new vehicle features and improving production efficiency. Intel’s self-driving company, Mobileye, has officially filed for an IPO and is targeting a valuation of approximately $20 billion after initially announcing to publicly list the company in December of 2021. Additionally, Siemens has signed a deal to supply equipment and technology for EV battery plants to a joint venture backed by Stellantis, Mercedes Benz, and Total Energies.

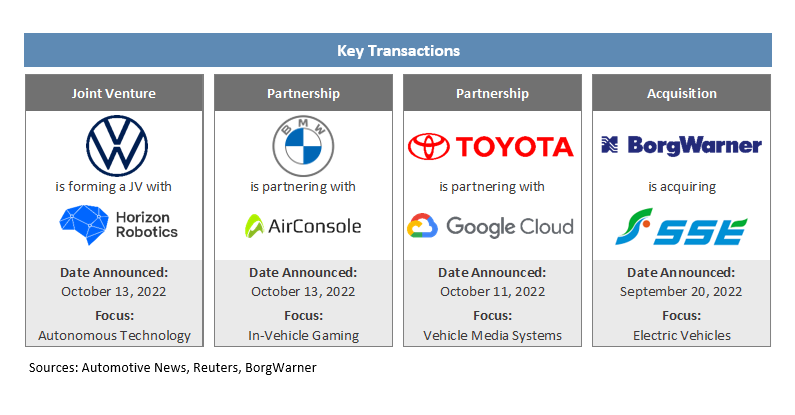

See below for additional detail on recently announced transactions.

- Volkswagen Group (VW) will invest $2.3 billion for a 60 percent equity stake in forming a new JV focused on autonomous driving technology with Chinese technology company, Horizon Robotics. VW and Horizon will collaborate to develop driving software and hardware that will accelerate the automaker’s improvements in its vehicle connectivity and software capabilities.

- BMW and AirConsole have partnered to bring video game services inside the German automaker’s vehicles. AirConsole has more than 180 games, which will be delivered over-the-air and playable via BMW’s infotainment display. The partnership aims to drive innovation in combining technologies for every waiting moment in EVs , such as charging.

- Toyota has announced its partnership with Google Cloud, in efforts to boost the OEMs artificial intelligence-based speech services and enhance its vehicle infotainment systems’ voice recognition ability. The technology has already been included in several 2023 Toyota and Lexus models.

- BorgWarner has announced its intention to acquire the EV charging business of Hubei Surpass Sun Electric Company (SSE) for $58.4 million. With the acquisition, SSE accelerates its growth in electrification and BorgWarner expands its vehicle electrification business into China through SSE’s EV solution, Smart Grid and Smart Energy businesses.

Regulatory Landscape

New York Vehicle Sales Ban: New York plans to require all new vehicles sold within the state to be either electric or a plug-in electric hybrid by 2035. The rules closely follow California’s ban on the sale of gasoline powered vehicles and focus on achieving zero emission vehicle sales targets, effectively phasing out internal combustion engine (ICE) vehicles by 2035.

General Motors Lawsuit: GM has recently faced a class action lawsuit stating the OEM failed to disclose to consumers that thousands of its vehicles had an engine defect. The defects allegedly include engine stalling and premature breakdowns, as well as flaws in steering wheel sensors and ignition switches. GM has been ordered to pay $102.6 million but intends to appeal the verdict.

Stellantis Emissions Probe: Stellantis will pay $5.6 million in total to resolve investigations by the state of California into air quality violations. This is the OEM’s second settlement with California, and it will pay a $2.8 million civil penalty and another $2.8 million to bring more electric school busses to the South Coast Air Basin.

Nikola Founder’s Conviction: Trevor Milton, founder of the electric vehicle and truck manufacturer Nikola, was recently found guilty on one count of securities fraud and two counts of wire fraud by a U.S. jury. The conviction comes after the founder lied to investors about the EV company’s technology and attempted to inflate its stock price. Nikola agreed to pay $125 million to settle with the SEC in 2021.

Stay connected to industry financial indicators and check back in November for the latest Auto Industry Spotlight.