Global Economic Conditions Remain Unfavorable, and A&M Finishes Its Two-Part Series on Expanding Business Opportunities for OEMs and Suppliers

Along with inflation of 8.3 percent in August, the industry is still facing the challenges of COVID-19, supply chain issues and parts shortages. Despite remaining at historically low levels, automotive inventory in August increased to its highest level in over a year, while sales saw marginal improvement month-over-month.

In this issue, A&M explores new opportunities for original equipment manufacturers (OEMs) and suppliers through analyzing various recreational vehicle markets as the selected topic for the September Industry Focus.

In transaction news, IPO activity remains strong even with difficult global financial market conditions. Additionally, OEMs and suppliers continue to evaluate growth initiatives to competitively position themselves for the electric vehicle (EV) era.

In regulatory news, federal agencies and the state of California are working to decarbonize global economies and implement zero-emissions transportation solutions by 2035, respectively.

Additional September insights are included below.

Financial Performance

Auto Forecast Solutions’ (AFS) latest numbers show that shutdowns and delays have resulted in approximately 3.3 million lost vehicles globally during calendar year 2022. In the past month, microchip shortages have affected production across the globe, contributing to major OEMs shutting down facilities and decreasing their manufacturing output capacity. The latest AFS estimates suggest approximately 4.1 million total cars and trucks will be affected by chip-related disruptions in 2022, in addition to more than 10 million vehicles cut from production in 2021.

Global EV sales have surged to their highest levels, although several challenges for auto makers have begun to surface. The growing popularity of EVs has resulted in OEMs and battery manufacturers investing significant capital to formulate strategic partnerships to build U.S. battery plants and assist in sourcing key materials, especially lithium, which has tripled in pricing over the last year to a record high of $71,315 per ton. Along with elevated pricing, China is the global hub for battery mineral refining, a critical component of the EV supply chain. The U.S. is currently in a booming EV market but will need to diversify the EV supply chain to localize mineral mining and chemical processing, while keeping high environmental standards in order to benefit from tax-credits and create long-term success.

Industry Update

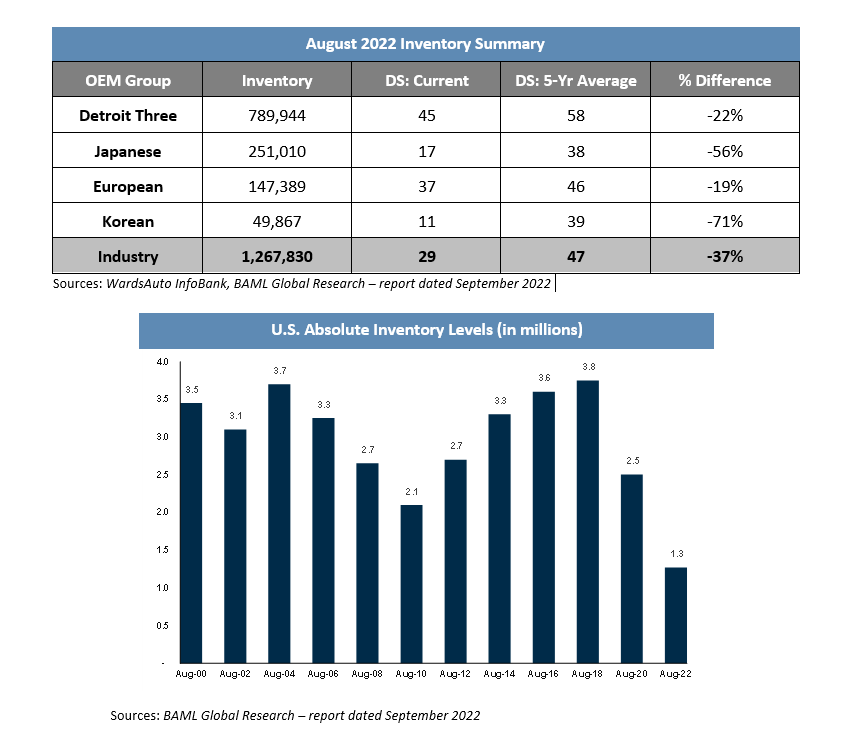

Automotive inventory increased by 117,000 units in August, resulting in approximately 1.27 million total units. This translates to a days’ supply (DS) that is 37 percent below the five-year average at 27 DS. The month-over-month unit increase in inventory is the highest level recorded since June of 2021. While uncertainty persists across the broader macroeconomic environment, auto production will likely remain under pressure for the rest of 2022, with predictions of a more robust inventory restock occurring well into 2023 at the earliest.

New light vehicle sales in the U.S. improved 1 percent year-over-year in August with a 13.2 million seasonally adjusted annualized rate (SAAR) of sales, while the full-year sales pace is tracking at 13.7 million units. 2022 sales continue to be heavily impacted by limited inventories that are a product of global COVID-19 outbreaks, supply chain issues and component part shortages. Average transaction prices also increased month-over-month, resulting in a 10.3 percent increase to $45,178 per vehicle. Transaction prices are expected to remain elevated and may subsequently fall as unit volumes begin to recover.

Industry Focus – Recreational Electric Vehicle Markets

As EV production continues to expand, OEMs and suppliers are strategically expanding into markets beyond passenger vehicles. Automotive companies are looking to generate further movement towards electrification by capitalizing on a relatively new and untapped market, recreational vehicles (RVs).

In this month’s industry focus section, A&M finishes its two-part series on expanding markets for OEMs and suppliers, through analyzing several types of electric recreational vehicle (e-RV) market opportunities that include motorcycles, boats and several different types of air mobility solutions.

RVs and Motorcycles

The fast-paced evolution of EVs has already impacted the recreational vehicle market, with several RV manufacturers developing concepts purposed for activities such as emissions-free camping, in addition to having towing and charging capabilities. RV maker, Thor, recently conducted a North American study which illustrated approximately 50 percent of individuals expect to drive five to six hours before needing to charge their e-RVs, consistent with the 300-mile range exhibited by most EVs currently on the road. Foreign OEM, Renault, has piloted the movement into RVs for auto makers through the release of its new campervan, which is fully electric and features drone delivery capabilities.

In addition to RVs, OEMs are also sparking innovation with electric motorcycles. Honda has recently announced plans to launch more than 10 models of e-motorcycles globally over the next three years. As part of its mission to achieve zero-emissions in transportation, the Japanese manufacturer is targeting 1 million units in motorcycle sales in the next five years and 3.5 million units annually by 2030. Electric motorcycles are more popular in developing economies, while growing in developed economies as the industry continues its shift towards electrification.

Boats and Air Mobility Solutions

Over the last year, OEMs have created exposure to a new type of electric recreational vehicle: boats. Through strategic investments and partnerships with boat manufacturing startups, both GM and Polestar have exploited the opportunity and are looking to diversify their operations. GM paid $150 million for a 25 percent stake in Pure Watercraft, a Seattle-based startup. Polestar announced a multi-year agreement to supply batteries and charging systems for Candela, an electric speed boat and water taxi manufacturer. Additionally, a third boating startup, Arc, has emerged, with roots to Tesla and SpaceX engineers. Arc recently raised $30 million in its Series A round of financing and looks to revolutionize the boat industry with a battery capacity three times that of a Tesla.

The investments into this segment come as the U.S. boating market has seen growth for nine consecutive years. Similar to EVs, investors are betting on increased consumer interest based on electric boats being more cost-effective and reliable, requiring less maintenance and reducing carbon emissions.

Companies are also looking to further diversify their electrification and usher in a new era of electric transportation by expanding into air mobility solutions. Honda Motor Co., which announced it will discontinue internal combustion products by 2040, has stated its focus on electric air mobility vehicles. One new initiative is an electric vertical take-off and landing, or eVTOL, aircraft. This new direction helps the company integrate itself further in the aircraft space, working cohesively with its established jet business arm. Honda is looking to begin test flights in 2024, determine the business outlook by 2025 and subsequently go commercial by 2030. Hyundai has also tapped into electric air mobility through its air taxi division, Supernal. The company plans to utilize Miami as a commercial hub and launch its flying taxis in 2028.

Suppliers are also noticing the lucrative opportunity as Denso Corporation, a Japanese global automotive components manufacturer, has developed a new motor through partnerships with aerospace company Honeywell International and German air transport company, Lilium. The electric motor will be integrated into Lilium’s eVTOL aircraft and represents Denso’s commitment to achieve carbon neutrality through various vehicle types.

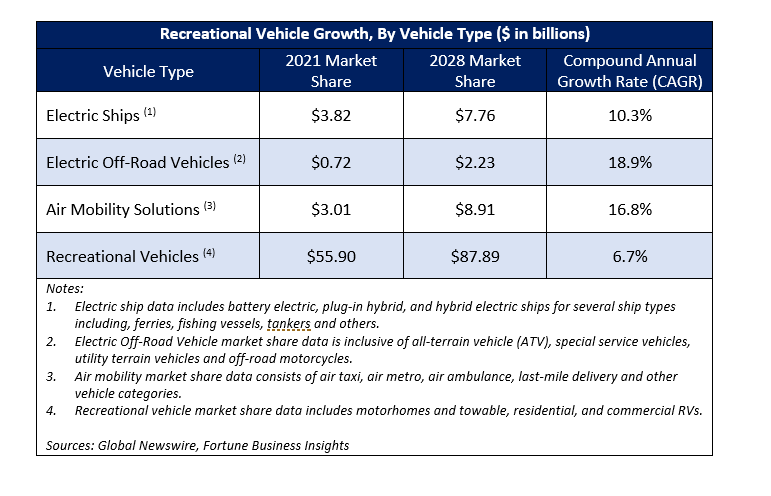

The expansion of electric recreational vehicles will certainly have its challenges, but e-RVs offer the potential for diversification and immense growth over the next five years. To see each RVs respective market share and estimated annual growth rate, please view the table below.

To view part 1 of the new market opportunities for OEMs, please see here.

Transaction Activity

In recent transaction news, adverse market conditions have not stopped Volkswagen from moving forward with its IPO for Porsche, which will consist of 911 million shares and an estimated valuation range of approximately $70 billion to $80 billion. Additionally, EV and autonomous driving startups, Leapmotor and WeRide, are considering going public and plan to raise up to $42.4 million and $500 million, respectively. Lastly, Honda and Nissan have announced two joint ventures and an acquisition, respectively, focused on electric vehicle batteries and procurement.

See below for additional detail on recently announced transactions.

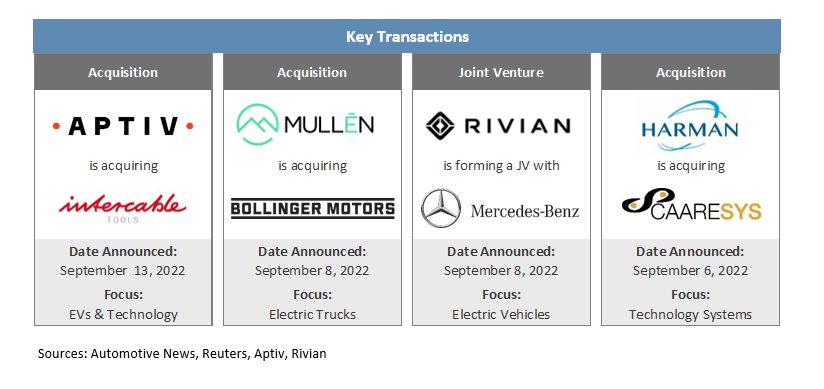

• Autonomous vehicle software supplier, Aptiv plc, has acquired 85 percent of Intercable Automotive Solutions for approximately $600 million. The acquisition will enhance Aptiv’s position as a full system EV manufacturer, provide more efficient and cost-effective assembly operations and address complex challenges in vehicle electrification. Intercable is an industry leading provider of high-voltage power distribution and high-precision connection technologies.

• EV manufacturer, Mullen Automotive, acquired a 60 percent controlling interest in Bollinger Motors for $148 million in cash and stock. The transaction allows Mullen to tap into the electric SUV and commercial truck markets, while Bollinger can leverage Mullens solid-state battery technology and expertise.

• Rivian Automotive and Mercedes Benz have announced their joint venture and look to develop synergies in scaling the production of electric vans in Europe. As part of the transaction, Mercedes will spend about $400 million to restructure its German-based manufacturing facilities that currently build Sprinter vans, in an effort to neutralize the heightened costs for EVs. Both OEMs aim to produce their EV models on a joint production line.

• HARMAN International acquired CAARESYS, an Israel-based startup that develops vehicle passenger monitoring systems. CAARESYS has already partnered with major auto makers and will assist in strengthening HARMAN’s capabilities for in-cabin safety, digital cockpit and advanced driver assistance system (ADAS) solutions.

Regulatory Landscape

California Vehicle Sales Ban: California has recently approved regulations by the California Air Resources Board (CARB) that ban the sale of new gasoline-powered vehicles and trucks by 2035. The regulations aim to phase out internal combustion engine vehicles and establish zero-emission vehicle (ZEV) sales targets of 35 percent in 2026 and 68 percent in 2030. The rules will test the power grid and EV charging networks but could potentially avoid greenhouse-gas emissions that amount to the equivalent of 915 million barrels of oil between 2026 and 2040.

Federal Decarbonization Efforts: The U.S. Environmental Protection Agency (EPA), Energy, Transportation and Housing and Urban Development federal departments have announced their agreement to collectively decarbonize the transportation sector and increase affordability in low- and zero-emission vehicles. The agencies plan to lead the global decarbonization effort and domestic net-zero emissions by 2050 through working closely with states, local communities and other key stakeholders.

Cybersecurity Improvements: The National Highway Traffic and Safety Administration (NHTSA) has revamped its cybersecurity guidelines from 2016, covering several potential issues and making vehicle security a top priority for auto makers. In a time when vehicle technology and connectivity is developing quickly, the updated practices will provide the industry with the necessary tools to combat cybersecurity risks.

Toyota Settlement: Toyota Motor Corporation has reached a settlement potentially worth $150 million, as the OEM works to resolve U.S. class-action lawsuits over defective fuel pumps and recalls. The litigation covers about 3.36 million Toyota and Lexus vehicles that experienced several engine-related issues, which resulted in Toyota providing extended vehicle warranties, complimentary loaner cars and towing options for repairs to the claimants.

Stay connected to industry financial indicators and check back in October for the latest Auto Industry Spotlight.