U.S. Infrastructure Investments Remain Strong Despite Midstream Management Risks

In the mid 2000s, an American energy renaissance began. As a result, an industrial renaissance also dawned in the U.S. Both are being driven by new fossil fuel technologies that make cheap energy possible. Government economic studies have stated that almost one million jobs have been added due to cheaper natural gas as a result of the new fracking technologies. Other studies model an additional million manufacturing jobs to be created in the coming years as a result of continued cheap natural gas prices. India has agreed to begin importing U.S. crude to replace Middle Eastern crude in the near future. China will soon be importing a massive amount of U.S. liquefied natural gas (LNG) to satiate its energy hunger as it industrializes its western regions and modernizes its energy sector.

United States capitalists know the energy markets will be there. Manufacturing. China. India. Global population growth. Technology. They all point to the U.S. as the global leader in energy with the ability to provide the world its energy needs - and soon. As a result, investments in U.S. energy will increase dramatically over the coming years. Despite low crude prices in the U.S. today, investments are increasing quickly. In the first quarter of 2017, private equity alone invested nearly $20 billion into shale assets. Per Barclays and Bloomberg, U.S. drillers will spend over $80 billion in 2017.

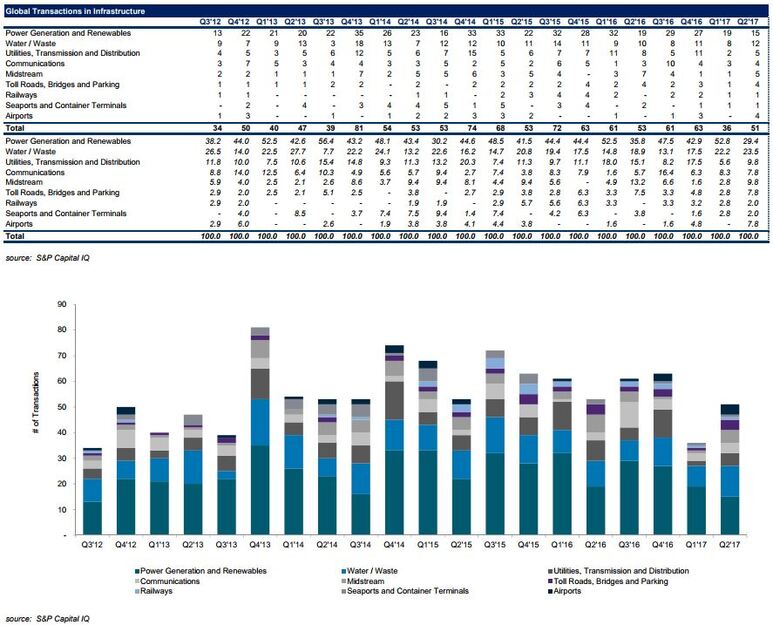

With drilling capital comes infrastructure spend. For every $1 of upstream spend, it is estimated that 15 to 30 cents of infrastructure spend is required to push the BTUs to market. Infrastructure is capital-intensive, with fewer players than their exploration and production counterparts. Despite the use of MLPs as an efficient mechanism to invest in this infrastructure and numerous public midstream companies, there is still an undersupply of infrastructure for producers. The pipe in the ground doesn’t necessarily go to the right plays nor, due to LNG, necessarily does the pipe today deliver to its end market. As a result, there is massive opportunity for investors - and quite a bit of risk.

Infrastructure projects are, of course, susceptible to price risk. Price variation has and will always exist in a capitalistic market. There is a large and less apparent risk to be managed by investors, however. It is important that infrastructure investors understand that midstream is not ‘your father’s pipeline’ business, but rather a service business that requires an intimate relationship with the producer customer. Producers provide intensive amounts of intellectual property and planning information associated with their fields. Midstream companies make large investment bets in exchange for that information. Their financial well-being relies on the accuracy of the geology, drilling programs, investment timing and production estimations of producers and their contractors.

The relationship between the producer and midstream is more akin to a marriage contract than a commercial contract. Midstream management teams must be very good at building that intimate relationship with their producers. They must understand the producer and his motivation and they must service that producer based on the understanding of this motivation. Good midstream teams understand that contracts are not just ‘cents per MMBTUs’ but value-added contracts that help producers make hydrocarbons flow to end markets as a service, given the producers’ motivations and plans. Good midstream management teams also understand how to build contracts with producers that extract the value out of this intimate knowledge for themselves while making their producers satisfied. Good midstream management teams are a rare and difficult find. Like coach trees in the NFL, management team candidates are often found under existing, strong midstream teams. They are highly valued and the proven ones are difficult to pry from current investments. Potential investors must scrutinize these teams thoroughly, for all bets on success lay with their capabilities. Front end capital with years of contractually obliged profits, or losses, are at risk in every producer relationship.

The opportunity is large for investors. Risks must be managed. The biggest risk to manage is to ensure the right midstream management team for the market is at the helm.