Despite Strong Winds, Golden Parachutes Still Holding Steady

2016-Issue 7 – Executive compensation continues to be bombarded with scrutiny by shareholders, shareholder advisory firms, politicians and the media. With say-on-pay voting now well established, the voices of shareholders are getting louder, and companies are listening. Many companies have made significant changes to their compensation strategy in recent years to appease stakeholders. In particular, companies have altered their course on benefits provided to executives in connection with a change in control, commonly called "golden parachutes."

Change in control benefits can include severance payments, accelerated vesting and payment of equity awards (such as stock options or restricted stock), fringe benefits, and gross-up payments for excise taxes imposed as a result of Internal Revenue Code Sections 280G and 4999. The Securities and Exchange Commission (SEC) requires public companies to disclose the value of these benefits in the company’s annual proxy filing. Shareholders can voice their frustration (or satisfaction) with the company’s pay practices through their say-on-pay votes.

To help companies keep their change in control benefits in line with their peers and to shed light on current pay trends, Alvarez & Marsal’s Executive Compensation and Benefits Practice conducted another study of change in control arrangements among the top 200 U.S. publicly traded companies in 2015. This article summarizes our methodology and key findings for 2015. Find the comprehensive report with the full study results, including industry-specific analysis here. The study was also performed in 2013.

Methodology for Change in Control Analysis

We conducted a comprehensive analysis of executive change in control arrangements of the top 200 U.S. publicly traded companies. To compare practices in different industries, we reviewed the 20 largest companies in 10 different industries. The companies were selected based on market capitalization.

The analysis focused on change in control protections provided to the chief executive officer (CEO) and other named executive officers (NEOs). The analysis was based on information in each company’s "Compensation Discussion and Analysis" section of the proxy statement. Below is a summary of some of our key findings.

Key Findings

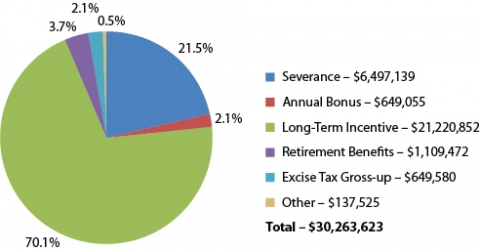

- The average total value of change in control benefits for the top 200 CEOs remained relatively flat, at $30,263,623 in 2015 compared to $29,853,057 in 2013. This is mainly driven by the value of long-term incentive awards offsetting decreases in severance and excise tax gross-ups.

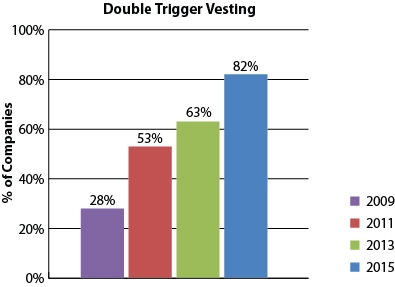

- In 2015, 82 percent of companies had at least one equity plan that provided for double trigger vesting (change of control and termination of employment required to accelerate vesting of equity awards). This is a significant increase since 2011 when just 53 percent of companies had such provisions.

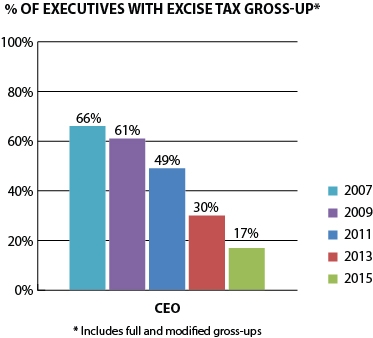

- Just 17 percent of CEOs are entitled to receive “gross-up” payments — meaning the company will pay the executive the amount of any excise tax imposed as a result of a change in control, thereby making the executive “whole” on an after-tax basis. This is a substantial decrease from 2007, when this benefit was provided to 66 percent of CEOs.

- There are significant differences in change in control protection between industries. To examine differences in change in control protection by industry, you can access a full copy of the study results here.

Benefit Values for CEOs

One goal of the SEC executive compensation disclosure rules is transparency. To aid in this effort, companies must quantify any parachute payments the CEO and other NEOs would receive upon a hypothetical change in control at year-end and must disclose those amounts in the annual proxy statement. From information provided in the “Potential Payments upon Termination or Change in Control” section, as well as other sections of the executive compensation disclosure, we calculated the average amount of typical parachute payments.

On average, CEOs were entitled to change in control benefits of $30,263,623 in 2015. Over 70 percent of that value comes from accelerated vesting of long-term incentives, the value of which is largely driven by fluctuations in the stock market. Since 2011, the value of long-term incentives increased by more than $3.25 million. However, this increase was offset by decreases in the value of severance and the elimination of excise tax gross-up payments. Accordingly, the average total value of change in control benefits for CEOs has hovered around $30 million since 2011.

The pie chart below illustrates the 2015 average value of each type of benefit for CEOs at the top 200 U.S. publicly traded companies.

Change in Control Triggers

Upon a change in control, most companies provide for accelerated vesting of equity awards. The two most common equity acceleration triggers are the single trigger (only a change in control must occur) and double trigger (change in control and termination of employment must occur). We continue to see a shift from a single-trigger toward double-trigger vesting. Accordingly, double-trigger vesting has significantly increased as shown in the chart below.

Notwithstanding the current shift to double-trigger vesting, 43 percent of companies still have at least one equity plan that provides for single-trigger vesting. However, because equity plans typically remain in place for 10 years, we expect the prevalence of single-trigger vesting to continue to decrease in the coming years.

Excise Tax Protection

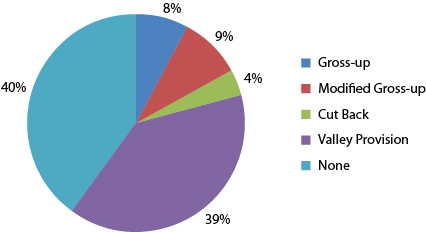

Under the “golden parachute” provisions of Code Section 280G, a payment to an executive exceeding the “safe harbor” limit results in a 20 percent excise tax on the executive and a disallowance of the tax deduction to the corporation. Companies may address this excise tax issue in one of the following ways:

- Gross-up: The company pays the executive the full amount of any excise tax imposed. The gross-up payment thereby makes the executive “whole” on an after-tax basis. The gross-up includes applicable federal, state and local taxes resulting from the payment of the excise tax.

- Modified gross-up: The company will gross-up the executive if the payments exceed the safe harbor limit by a certain amount (e.g., $50,000) or percentage (e.g., 10 percent). Otherwise, payments are cut back to the safe harbor limit to avoid any excise tax.

- Cut-back: The company cuts back parachute payments to the safe harbor limit to avoid any excise tax.

- Valley provision: The company cuts back parachute payments to the safe harbor limit if it is more financially advantageous to the executive. Otherwise, the company does not adjust the payments and the executive is responsible for paying the excise tax.

- None: Some companies do not address the excise tax; therefore, executives are solely responsible for the excise tax.

This pie chart illustrates the prevalence of excise tax protection provisions for CEOs in 2015.

Shareholder advisory firms continue to drive changes in excise tax protection. Providing excise tax gross-up protection in new or amended agreements could lead shareholder advisory firms to recommend voting against the company’s say-on-pay resolution and/or the reelection of members of the compensation committee. Because of this increased scrutiny, many companies have chosen to eliminate the use of excise tax gross-ups from executive agreements. Additionally, 93 percent of the companies that currently provide excise tax gross-up protection have disclosed their intention to eliminate this benefit in the future. Companies that have removed, or intend to remove, excise tax gross-ups are generally moving to a valley provision or to providing no excise tax protection to executives.

The decline in the prevalence of excise tax gross-up protection for CEOs from 2007 through 2015 is illustrated in the chart below.

Alvarez & Marsal Taxand Says:

While the total value of benefits that CEOs are entitled to upon a change in control has remained flat for the past five years, shareholders and other stakeholders have succeeded in changing the course of golden parachutes, as evidenced in the decline of excise tax gross-ups and single-trigger equity vesting. Ongoing pressure from shareholders, shareholder advisory firms and regulators will continue to make a significant impact on the types of change in control benefits provided to executives. Boards of directors and compensation committees need to remain attentive to changing market trends and be ready to respond when challenges arise regarding the benefits provided to executives.

Managing Director, Dallas

+1 214 438 1028

Disclaimer

The information contained herein is of a general nature and based on authorities that are subject to change. Readers are reminded that they should not consider this publication to be a recommendation to undertake any tax position, nor consider the information contained herein to be complete. Before any item or treatment is reported or excluded from reporting on tax returns, financial statements or any other document, for any reason, readers should thoroughly evaluate their specific facts and circumstances, and obtain the advice and assistance of qualified tax advisers. The information reported in this publication may not continue to apply to a reader's situation as a result of changing laws and associated authoritative literature, and readers are reminded to consult with their tax or other professional advisers before determining if any information contained herein remains applicable to their facts and circumstances.

About Alvarez & Marsal Taxand

Alvarez & Marsal Taxand, an affiliate of Alvarez & Marsal (A&M), a leading global professional services firm, is an independent tax group made up of experienced tax professionals dedicated to providing customized tax advice to clients and investors across a broad range of industries. Its professionals extend A&M's commitment to offering clients a choice in advisers who are free from audit-based conflicts of interest and bring an unyielding commitment to delivering responsive client service. A&M Taxand has offices in major metropolitan markets throughout the United States and serves the United Kingdom from its base in London.

Alvarez & Marsal Taxand is a founder of Taxand, the world's largest independent tax organization, which provides high quality, integrated tax advice worldwide. Taxand professionals, including almost 400 partners and more than 2,000 advisers in nearly 50 countries, grasp both the fine points of tax and the broader strategic implications, helping you mitigate risk, manage your tax burden and drive the performance of your business.

To learn more, visit www.alvarezandmarsal.com or www.taxand.com