Alvarez & Marsal releases UAE Banking Pulse for Q1 2021

Dubai – Leading global professional services firm Alvarez & Marsal (A&M) has released its latest UAE Banking Pulse for Q1 2021. The report highlights that the top 10 UAE banks started the year on a mixed note, as the aggregate net income increased by 85 percent QoQ, due to a decline in operating expenses and impairment charges which supported the overall profitability. However, loan & advances continued to contract with a 0.7 percent decrease in fiscal first-quarter whilst deposits increased to 1.2 percent, after declining in Q4’2020.

The UAE’s strong fiscal and external positions will continue to support the fundamentals of the banking sector. However, persistent pressure on the real estate sector continues to pose risks for UAE banks.

Authored by Asad Ahmed, A&M Managing Director and Head of Middle East Financial Services, Alvarez & Marsal’s UAE Banking Pulse, examines the data of the 10 largest listed banks in the UAE, comparing the Q1’21 results (Q1’21) against Q4’20 results. Using independently sourced published market data and 16 different metrics, the report assesses banks’ key performance areas, including size, liquidity, income, operating efficiency, risk, profitability and capital.

The country’s 10 largest listed banks analysed in A&M’s UAE Banking Pulse are First Abu Dhabi Bank (FAB), Emirates NBD (ENBD), Abu Dhabi Commercial Bank (ADCB), Dubai Islamic Bank (DIB), Mashreq Bank (Mashreq), Abu Dhabi Islamic Bank (ADIB), Commercial Bank of Dubai (CBD), National Bank of Fujairah (NBF), National Bank of Ras Al-Khaimah (RAK) and Sharjah Islamic Bank (SIB).

The prevailing trends identified for Q1 2021 are as follows:

-

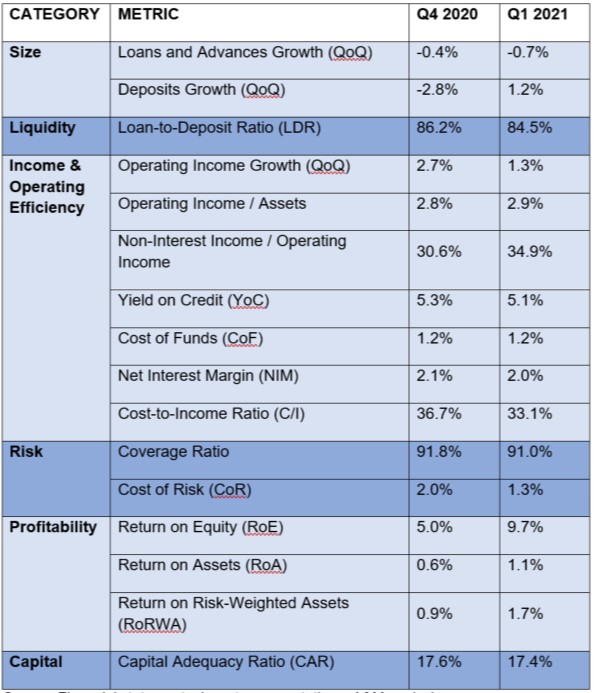

Loan & advances (L&A) declined by 0.7 percent QoQ whereas deposits increased by 1.2 percent QoQ in Q1’21. Aggregate loans to deposit ratio (LDR) decreased to 84.5 percent in Q1’21 compared to 86.2 percent in Q4’20.

-

Operating income increased by 1.3 percent QoQ, largely on the back of reduced net interest income (NII). This was partially offset by 5 percent QoQ decline in net interest income due to lower interest rates. Emirates NBD reported the highest increase in its total operating income, of more than 25 percent QoQ, as fee income grew by 42 percent owing to higher business volumes.

-

Aggregate net interest margin (NIM) continued to remain under pressure as declined to a multi-year low, decreasing by 10 bps to 2.0 percent in Q1’21. This was due to a decline in yield on credit, -19 bps QoQ, while the cost of funds remained largely flat at 1.2 percent. NIM deteriorated for most of the banks.

-

Cost-to-income (C/I) ratio decreased by 3.6 percent points to 33.1 percent, after increasing for two consecutive quarters. Among the top 10 banks, Mashreq Bank reported the highest decrease in C/I ratio by 46.1 percent in Q1’2021. Five of the top 10 banks reported decreased C/I ratio.

-

Eight of the top 10 banks reported a decrease in cost of risk (CoR), as improved macroeconomic environment led to lower provisioning. Total loan loss provisions decreased 36.1 percent QoQ in Q1’21. The overall slump was driven by lower impairments from NBF (-71.7% QoQ), ADIB (-62.9% QoQ), DIB (-60.5% QoQ) and MSQ (-58.5% QoQ). Aggregate CoR decreased by 72 bps QoQ, as total provisioning decreased ~36.1 percent to AED 5.3bn. To achieve 100 percent coverage ratio, the top ten UAE banks would have to book additional AED 18.2bn in provisions, coming to 20 percent more than booked FY’20 provisioning. Among the individual banks, ADCB requires 40 percent more provisioning, than FY’20 levels, to achieve 100 percent coverage ratio.

-

Cumulative net income increased by 84.8 percent versus the previous quarter primarily due to significant decline in impairment allowances along operating expenses. Aggregate return on equity (RoE) improved from 5.0 percent in Q4’20 to 9.7 percent in Q1’21, as net income increased 85 percent QoQ.

OVERVIEW

The table below sets out the key metrics:

Mr. Ahmed commented: “The UAE banking sector has witnessed a sizeable improvement in profitability in the first quarter, and the trend is likely to continue for subsequent quarters. The Targeted Economic Support Scheme (TESS), which the Central Bank of UAE extended until June 2022, is expected to help cushion banks’ asset quality and ease their balance sheet stress through the second quarter of 2022.

As the economy recuperates from pandemic headwinds, banks’ income streams are expected to remain under pressure, while interest rates are likely to remain historically low. Operating costs and credit loss charges are expected to improve in 2021 compared to 2020 as banks focus on cost efficiency, adopt innovation and gain clarity on the economic recovery.”

About Alvarez & Marsal

Companies, investors and government entities around the world turn to Alvarez & Marsal (A&M) for leadership, action and results. Privately held since its founding in 1983, A&M is a leading global professional services firm that provides advisory, business performance improvement and turnaround management services. When conventional approaches are not enough to create transformation and drive change, clients seek our deep expertise and ability to deliver practical solutions to their unique problems.

With over 5,400 people across four continents, we deliver tangible results for corporates, boards, private equity firms, law firms and government agencies facing complex challenges. Our senior leaders, and their teams, leverage A&M’s restructuring heritage to help companies act decisively, catapult growth and accelerate results. We are experienced operators, world-class consultants, former regulators and industry authorities with a shared commitment to telling clients what’s really needed for turning change into a strategic business asset, managing risk and unlocking value at every stage of growth.

To learn more, visit: AlvarezandMarsal.com. Follow A&M on LinkedIn, Twitter, and Facebook.

###

CONTACT

Prerna Agarwal, Hanover Middle East, +971 52 787 3189

Sandra Sokoloff, Senior Director of Global Public Relations, Alvarez & Marsal, +1 212 763 9853