THE RETURN OF SECTION 301: WHAT DOES IT MEAN FOR APAC?

Section 301 of the US Trade Act of 1974 has re-emerged as a US trade-enforcement tool. Once used selectively, it is now being applied more broadly, covering forced labor, industrial policy, and structural excess capacity.

Following the Supreme Court ruling in February 2026 that limited presidential tariff powers under the International Emergency Economic Powers Act (IEEPA), two Section 301 investigations launched in March 2026 underscore a strategic shift: the statute is increasingly being used to influence global production and supply-chain behavior. For APAC companies embedded in manufacturing networks, this raises near-term risks of potential new tariffs and import restrictions.

Structural Excess Capacity and Production

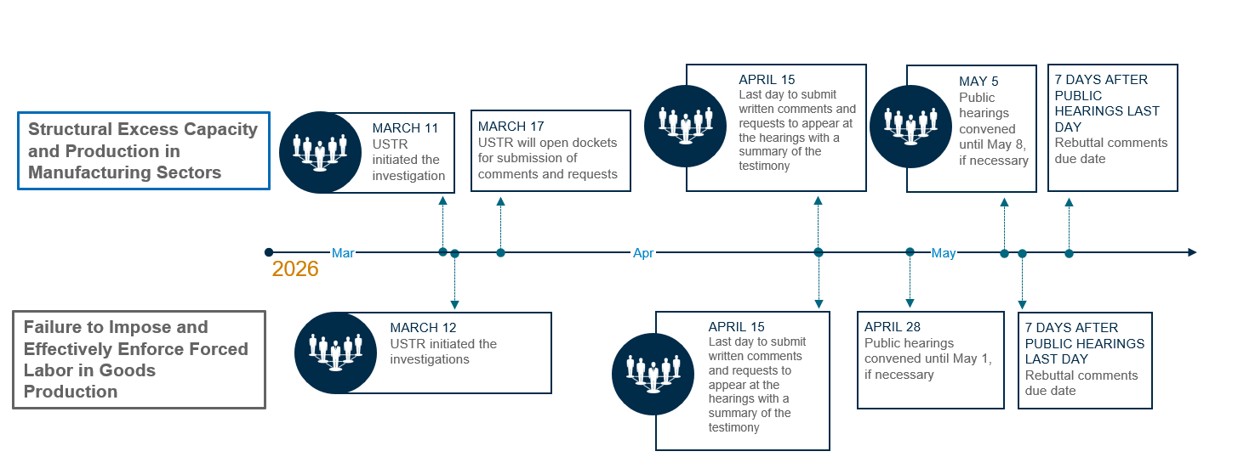

On March 11, 2026, the US Trade Representative (USTR) began investigating policies that contribute to excess manufacturing capacity. USTR claims that some countries maintain production levels beyond demand, often through subsidies or state-owned enterprises, leading to overproduction, export surges, and global market distortions that negatively impact US manufacturing.[1]

The investigation covers a broad range of sectors, including autos, electronics, semiconductors, steel, batteries, solar modules, and machinery and focuses heavily on Asia‑based manufacturing hubs. The table below presents selected APAC economies under review, along with their respective targeted manufacturing sectors:

| Country | Sector |

| China | Electronic equipment, machinery, automobiles and auto parts, plastics, furniture, articles of iron or steel, apparel, organic chemicals, toys and sporting goods, optical, photo, technical, and medical apparatus, iron and steel, footwear, ships and vessels, aluminum, and others |

| Singapore | Semiconductors, electronic equipment, petrochemicals, and pharmaceuticals |

| Indonesia | Metals, agricultural products, fuels, textiles, and construction goods |

| Malaysia | Electronic equipment, mineral fuels and oils, machinery, animal and vegetable fats and oils, and optical, photo, technical, and medical apparatuses |

| Thailand | Autos and auto parts, machinery, and rubber |

| Korea | Electronic equipment, automobiles and auto parts, machinery, steel, and ships and marine vessels |

| Vietnam | Electronic equipment, machinery, footwear, apparel, furniture, and steel |

| Taiwan | Semiconductors, electronic products, information technology products, and machinery |

| Japan | Automobiles and auto parts, and optical, photo, technical, and medical apparatuses |

| India | Textiles, health, construction goods, and automotive goods |

Forced Labor Import Prohibitions

On March 12, 2026, USTR initiated another Section 301 investigation into the failure of multiple economies to impose and effectively enforce prohibitions on the importation of goods produced with forced labor.[2]

The investigation examines not only domestic labor conditions but also whether jurisdictions block imports of forced-labor goods from other countries, especially those found in complex supply chains. USTR explicitly highlights downstream products such as textiles, electronics, solar products, and auto parts. Examples of significant products produced in certain APAC countries, as listed in the US Department of Labor’s 2024 List of Goods Produced by Child Labor or Forced Labor (the TVPRA List)[3], are provided below:

Table 1: Goods ‘Produced’ with Forced Labor

| Country | Good |

| Bangladesh | Dried fish, garments |

| Myanmar | Bamboo, beans (green, soy, yellow), bricks, fish, garments, jade, palm thatch, rice, rubber, rubies, sesame, shrimp, sugarcane, sunflowers, teak |

| Cambodia | Bricks |

| China | Gold, aluminum, artificial flowers, bricks, caustic soda, Christmas decorations, coal, cotton, electronics, fireworks, fish, footwear, garments, gloves, hair products, jujubes, metallurgical grade silicon, nails, polysilicon, polyvinyl chloride, squid, textiles, thread/yarn, tomato products, toys |

| India | Bricks, carpets, cottonseed (hybrid), embellished textiles, garments, rice, sandstone, shrimp, stones, sugarcane, tea, thread/yarn |

| Indonesia | Fish, nickel, palm fruit |

| Malaysia | Electronics, garments, palm fruit, rubber gloves |

| Pakistan | Bricks, carpets, coal, cotton, sugarcane, wheat |

| Thailand | Fish, garments, shrimp |

| Vietnam | Garment |

Table 2: Downstream Goods ‘Produced’ with Forced-Labor Inputs

| Country | Downstream Goods at Risk | Forced-Labor Input (source) |

| China | Garments, textiles, cotton-based Products | Cotton |

| Silica-based products, solar products, semiconductors | Polysilicon | |

| Malaysia / Indonesia | Cooking oils, animal feed, baked goods, biofuels, beverages, household and industrial products, infant formula, personal care products, cosmetic products, shortening, pet food | Palm fruit |

| Thailand | Animal Feed (fish-based) Fishmeal Fish Oil | Fish from Thai fisheries (forced) |

The scope is broad and includes several APAC economies, including China, India, Indonesia, Thailand, Vietnam, and Malaysia.

A summary of the timelines for both investigations is provided below:

Implications for APAC

The current Section 301 investigations represent a pivotal moment for APAC economies. Today, most imports face a uniform 10% tariff under Section 122 of the Trade Act of 1974, a temporary, and time limited measure designed for short-term balance of payment concerns. Section 122 is not intended to support long-term or country specific actions, and once it expires, USTR is expected to use other statutes, such as Section 301 as a more durable legal basis for tariffs.

In the absence of submissions to USTR, the investigations are likely to be shaped largely by US government and industry evidence, increasing the likelihood of broader, higher, and longer-lasting tariffs that exceed the current 10% baseline, potentially returning to (or surpassing) the tariff levels previously imposed under the IEEPA tariff actions.

Recent developments have also weakened the stability of recently concluded trade deals and framework agreements, reducing their value as a predictable backstop against renewed tariff escalation. In practice, this can delay implementation, narrow the scope of commitments, and increase the risk that agreed market-access terms are revisited or suspended, leaving companies again with a lot of uncertainty.

Procedurally, submitting comments seems straightforward, but effective participation requires credible data, documentation, and coordination. For APAC companies, engaging in the Section 301 process is now essential to mitigate long-term trade risks.

Industry groups and affected sectors have begun preparing and submitting written comments, including coordinated submissions by global industry associations and responses from manufacturing sectors.[4] Companies may wish to monitor and, where appropriate, participate in these channels, while also preparing their own fact-based inputs (e.g., supply chain mapping, cost and sourcing impacts, and feasibility of alternative production) so that the USTR record reflects operational realities.

This kind of active engagement and monitoring process is increasingly becoming more important given the broader direction of US trade policy. In particular, recent Section 232 actions, effective April 6-7, 2026, further expand US trade‑policy risk for APAC supply chains. These new measures include a headline 100% tariff on certain patented pharmaceuticals and ingredients (with phased implementation and exceptions), as well as applying aluminum tariffs on the full customs value of aluminum articles and many downstream products, rather than only specific metal components. Together with the renewed use of Section 301, these Section 232 actions point to a more assertive and structural US trade policy approach, increasing overall tariff exposure for APAC‑linked supply chains.

Key Takeaways

- Section 301 is likely to remain a central US trade tool after the current temporary, uniform Section 122 tariff expires, and the two March 2026 investigations signal broad coverage across multiple APAC manufacturing and supply chain nodes.

- If companies do not submit comments, the administrative record may be shaped primarily by US government and industry inputs, raising the risk of wider or longer lasting tariffs and other restrictions.

- Begin preparing defensible, data-supported inputs now (e.g., product coverage, origin and transformation steps, sourcing flexibility, cost passthrough, and downstream impacts) to support submissions and ensure consistency across internal and external messaging.

With the renewed use of Section 301 together with the Section 232 measures effective in early April 2026, APAC companies need to act now and start building scenarios around potential outcomes (tariff rates, product lists, implementation timing) and identify practical mitigations (re‑sourcing options, inventory strategy, contract terms, and compliance enhancements).

[1] https://ustr.gov/trade-topics/enforcement/section-301-investigations/section-301-structural-excess-capacity-and-production-manufacturing-sectors

[2] https://ustr.gov/trade-topics/enforcement/section-301-investigations/section-301-failure-impose-and-effectively-enforce-prohibition-importation-goods-produced-forced

[3] https://www.dol.gov/agencies/ilab/reports/child-labor/list-of-goods#collapseOne

[4] https://tna.mcot.net/tna/en/news/list/148370; https://invisionmag.com/ustr-announces-multiple-section-301-investigations/; https://www.steel.org/2026/03/aisi-statement-on-ustr-section-301-investigations/; https://steelnet.org/sma-applauds-ustr-for-launching-section-301-investigations-into-excess-capacity/