Under the Hood: Transfer Pricing in the Thai Auto Parts Sector

The Thai auto parts sector is a cornerstone of the Thai economy contributing 10-12% of the GDP and has earned Thailand its nickname “The Detroit of Asia”. The strength of this sector results from several factors, including sustained support from the Thai government over a number of decades, especially through the Thai Board of Investment, a well-developed and integrated automotive ecosystem and a strategic location within ASEAN with extensive and efficient infrastructure. Thailand has also been able to build a large pool of experienced and skilled workers, which is being continually up skilled to face industry demands, including technological advancements.

Structure of the Thai Auto Parts Industry

Thailand has been able to attract many of the largest Original Equipment Manufacturer (OEM) automakers, from Japan, US, Europe and China. As the OEMs require auto parts makers to provide them with timely and cost-effective delivery of products, this has resulted in the development of a comprehensive local network of suppliers close to the OEMs. The auto parts industry is typically categorized into a hierarchy of three tiers, as follows:

Tier 1: Production of systems, modules and complete assemblies

Tier 2: Production of parts (e.g., chips, sensors, aluminum and steel components)

Tier 3: Production of raw materials (e.g., plastic, rubber etc.)

The Tier 1 suppliers in Thailand are mainly comprised of foreign-owned or foreign-Thai joint ventures whilst Tier 2 and 3 suppliers are dominated by Thai SMEs.

Transfer Pricing Considerations

For the foreign-controlled auto parts makers, a key tax issue to consider is the application of the Thai transfer pricing rules to any related party transactions. These rules are aimed at protecting Thailand’s tax base by requiring that the pricing of the related party transactions within a MNE group are arm’s length. Arm’s length prices are prices that would be expected in transactions between independent parties in the same or similar conditions and should ensure that MNE profits are allocated according to where value is created. The Thai subsidiary of the MNE is required to prepare documentation to support that its significant related party transactions are arm’s length based on the acceptable transfer pricing methods.

Key Value Drivers

Whilst the auto-parts suppliers share some common value drivers across the various tiers e.g., production quality and efficiency, there will be some significant differences given the level of the market and nature of products in each tier. For Tier 1 suppliers, technological development and OEM relationships are key whilst for Tier 2, the ability to produce highly technical parts without defects is critical. Tier 2 suppliers may also diversify sales across multiple industries. As the supplier of raw materials, Tier 3 suppliers drive value primarily through volume to lower unit costs. Managing the price volatility of commodities used in production will also be a key financial driver.

Functional Analysis

As a starting point in performing the transfer pricing analysis for an auto parts MNE operating in Thailand, it will be necessary to perform a functional analysis of the related parties in the supply chain. One of the key objectives of the functional analysis is to address where value is created within the MNE supply chain. To the extent that significant value creation activities take place in the Thai subsidiary, the transfer pricing policy adopted should ensure that that an appropriate profitability level is attributed to this entity.

R&D

Consistent with the nature and complexity of the products, most of the product R&D within the auto parts sector will be performed by Tier 1 suppliers with lower levels of R&D at Tiers 2 and 3 as focus shifts from systems innovation to process and material efficiency.

The auto industry’s move towards Electric Vehicle (EV) production and increasing adoption of automation technologies means added focus on R&D. For manufacturers of traditional combustion engine components, continued investment in research and development remains essential to advancing fuel efficiency.

The R&D may be split between (1) ground or platform R&D; and (2) application engineering. Platform R&D would be to develop technology which is used across OEMs e.g. ADAS sensors/software, flexible seating structures. Application engineering is an investment in a client specific project and may be compensated upfront by the OEM or through product pricing over the product life cycle.

During the functional analysis it will be necessary to assess which entity (or entities) own the product/manufacturing IP, which will entitle them to the returns on IP. Under the Thai TP rules, this will involve a consideration of which entity(ies) perform and control the development, enhancement, maintenance, protection and exploitation (DEMPE) functions. However, this may not be straightforward as it may be difficult to clearly identify the IP. The IP may, for example, be embedded in processes and know-how that are not clearly documented. It may also be difficult to identify valuable IP owned by the parts supplier in the case of the application engineering for specific OEM sales where the products are customized based on the technical specifications provided by the OEMs.

Given that the MNE parts suppliers may have a number of manufacturing bases around the globe located close to OEM manufacturers, it is possible that product development is decentralized and different elements of development are dispersed among these entities. This will further complicate consideration of which entities own the manufacturing IP and where the IP returns should be allocated.

Production

Production is the core driver and typically needs to be located close to the OEM and other suppliers to ensure optimal inventory management, including just in time delivery needs for the OEM. Quality management is key for the suppliers given the nature of the end-product with significant potential costs in cases where defects are found whether in the form of re-work/replacement costs through penalties and product liability. The suppliers bear volume risk associated with weak demand from the OEMs. In times of significant downturn, this could lead to difficulty in covering fixed production costs.

Marketing and Sales

Similar to the manufacturing IP, it will be necessary to determine which entity(ies) within the MNE own the marketing IP such as trademarks/tradenames and brands based on DEMPE analysis. Returns from the marketing IP should be allocated to these entities. The importance of brand value will however vary from Tier 1 to 3 suppliers with brand arguably more important for Tier 1 suppliers. However, even for Tier 1 suppliers there may be a question as to whether marketing IP provides significant value for sales to OEMs, given that it is a B2B transaction where more focus may be on technology, reliability, and quality. The brand itself may not feature on the product sold to the OEM as it is integrated into vehicles. Brand may, however, be a valuable profit driver for Tier 1 suppliers, such as the tire manufacturers, which operate in the aftersales market, where B2C sales may rely on brand recognition.

The strength of the tier 1 suppliers’ relationship with the OEMs will also be key to building long term stable business. The ability of the supplier to collaborate with the OEM on innovation, improved product quality and manufacturing efficiency will enable it to develop a more strategic and value-based relationship. The Tier 1 supplier’s sales teams may therefore be located close to the OEMs headquarters to support this collaboration.

Centralized Vs. decentralized

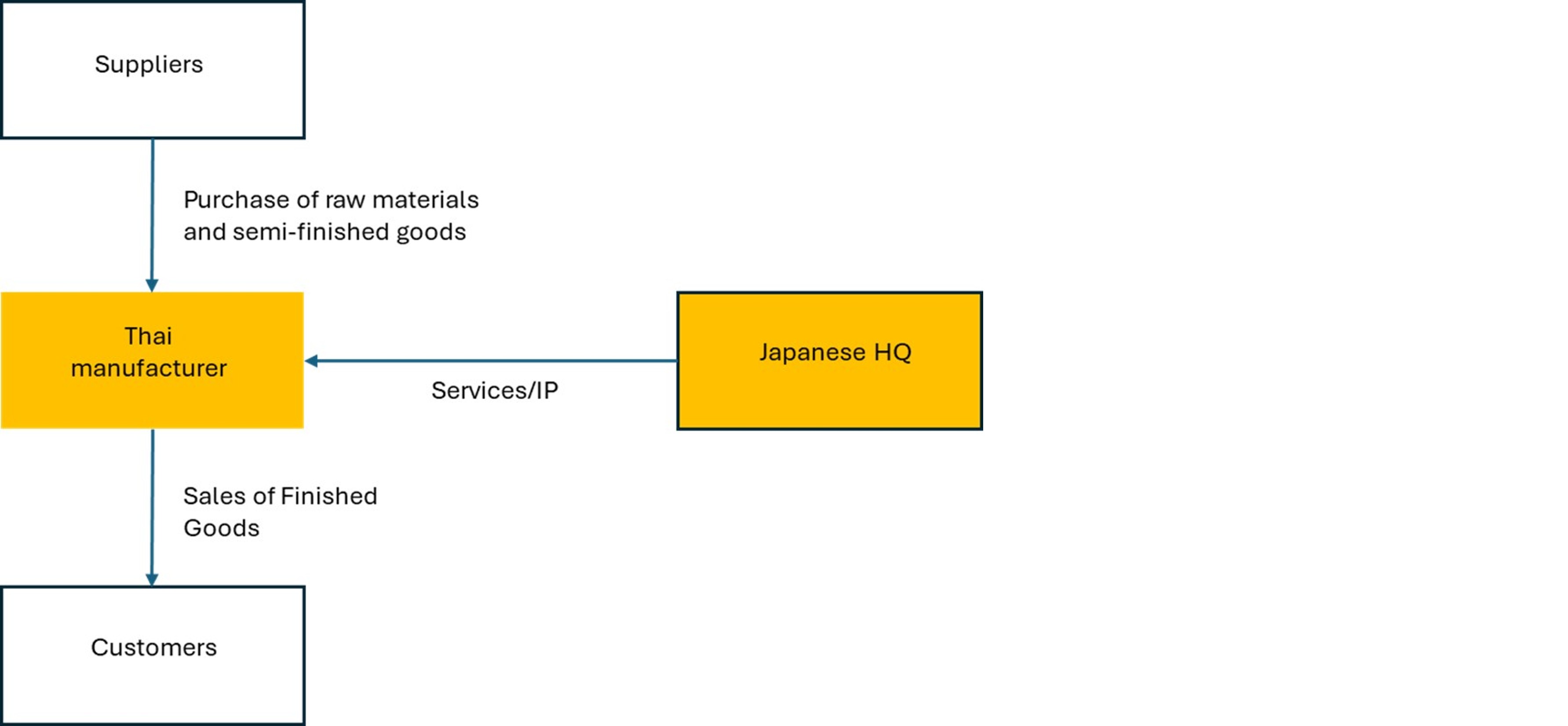

The sales relationship between the MNE supplier and the OEM may be centralized or decentralized. The sales model applied will have significant implications for the transfer pricing approach applied to the Thai manufacturing entity. However, given that the local manufacturing entity will typically be selling directly to the local OEM to satisfy requirements of the OEM, the commercial flows may be similar irrespective of whether a centralized or decentralized approach is applied. An illustrative commercial flow is shown in the diagram below.

Centralized Approach: The HQ owns the manufacturing and marketing IP and is responsible for maintaining the relationship with the OEM HQ, including marketing and sales and product innovation and development. The Thai manufacturer is essentially acting as a contract manufacturer on behalf of its HQ, which is an entrepreneur. In this case, the local manufacturer may be compensated with a routine profit margin for the manufacturing function. This return would typically be determined by benchmarking against the profitability of independent companies performing the same or similar functions. Since the Thai manufacturer is selling to and invoicing the local OEM directly, it would be necessary for the HQ to enter into agreement(s) with the Thai manufacturer to ensure that it receives the compensation for the provision of the IP and services but also ensures that the Thai manufacturer receives a routine return. In effect, the HQ will receive any residual profits under this arrangement.

Decentralized Approach: The HQ owns the platform manufacturing and marketing IP and provides certain support services, but the local manufacturer performs and controls marketing and sales functions with the local OEM and collaborates with the local OEM on new product innovation. In this case, the local manufacturer may be characterized as the entrepreneur given that it bears key risks, including market and volume risk. The HQ may enter into a license agreement with the local manufacturer for the provision of manufacturing and marketing IP and service agreement for the routine support services. The license may be benchmarked using comparable license agreements to provide a license fee based on a % of revenues and the support services may be benchmarked based on comparable service providers to provide a service fee based on cost plus. The result of this would be that the Thai manufacturer would be exposed to profitability fluctuations, which would be consistent with the entity’s characterization as an entrepreneur. However, a word of caution. The Thai Revenue Department typically expects a certain level of profit in a Thai subsidiary of an MNE. To the extent that the Thai subsidiary’s profits fluctuate, it will be necessary to clearly demonstrate that the Thai entity is exposed to risk given the functions it performs.

Conclusion

The Thai auto parts sector is a vital contributor to the Thai economy and is characterized by a structured hierarchy of suppliers. MNE auto parts suppliers operating in Thailand face transfer pricing considerations arising from their related party transactions. A detailed value chain and functional analysis is essential to determining which entities within the MNE group create value, which will need to be compensated through arm’s length pricing. The value creation activities will vary between the various auto tiers. Robust documentation and benchmarking are critical to ensure compliance and demonstrate arm’s length pricing.