The India–EU Free Trade Agreement: A Structural Shift in India’s Trade Trajectory

At a time when global coverage frequently highlights geopolitical tensions, trade policy shifts, and macroeconomic uncertainty, some material developments are also reshaping the future of global commerce. The India–EU Free Trade Agreement (FTA)1 signed in 2026 is one such milestone.

It represents a strategic opportunity for India’s trade ecosystem that can fundamentally reshape how Indian industry participates in Europe-linked value chains. Against the backdrop of shifting global supply dynamics, rising protectionism elsewhere, and intensifying competition from low-cost manufacturing hubs, this pact offers India a window to diversify exports, attract foreign investment, and integrate deeper with technology-intensive and consumer-facing markets.

A Structural Shift, Not Just a Tariff Event

India-EU FTA commits two of the world’s largest economic blocs - India (projected to be among the top three global economies by the early 2030s) and the EU (a € trillion-plus single market) - to long-term rules on trade facilitation.

For India, this is a diversification lever. Merchandize exports to the EU approached ~US$75 billion in 20242. This deal embeds tariff certainty and predictable market access - a critical factor that encourages European companies to invest, not merely trade.

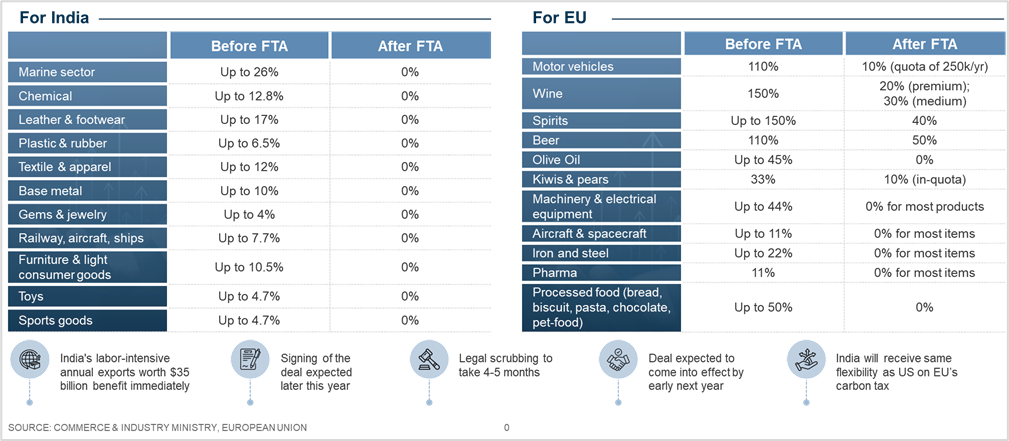

Tariff Liberalization Overview

As part of the pact, EU will eliminate duties on ~70% of tariff lines immediately, covering nearly 90% of India’s export value to EU. Another ~20% of lines will see phased elimination over three-five years, thus liberalizing ~99% of India exports to EU3.

India will open about 50% of tariff lines immediately, and phase out another ~40% over five, seven, and 10 years, thus liberalizing ~98% of EU export value to India4.

This will benefit key sectors on both sides.

Labour-intensive industries (textiles, leather, apparel, toys, marine products, gems & jewellery) benefit from immediate duty elimination, enabling rapid competitiveness gains. Heavy engineering and capital goods face a phased reduction, giving EU producers time to adapt.

Similar tariff events in other geographies have led to differentiating growth curves after initial capital flows.

Data reveals that Vietnam’s exports to EU jumped to 12-13% annual growth post FTA vs pre-FTA 4-5% average growth rate from 2018-20205. Similarly, Bangladesh leveraged the EU’s duty-free Everything But Arms (EBA) preferences to significantly expand its exports—from approximately US$2 billion in the early 2000s to over $23 billion in 2022–236.

Tariffs Matter Less, Non-Tariff Barriers Are the Real Gateways

Even after tariff elimination, Indian exporters will confront non-tariff barriers (NTBs) that have historically limited market access to Europe, such as

- Conformity Euro penne (CE) Marking: Mandatory for industrial machinery, electronics, and many engineered products.

- REACH (Registration, evaluation, authorization and restriction of chemicals) has forced ~40%7 of certain Indian chemical exporters to withdraw from the EU market due to compliance costs.

- Carbon border adjustment mechanism (CBAM) levies import charges based on embedded carbon emissions in goods like steel, cement and aluminium. CBAM can impose additional tax costs equivalent to 25%8 or more of export value on carbon-intensive exports if compliance is not managed, significantly dampening the financial benefits of tariff elimination

These regimes are enforced not merely as administrative compliance checkpoints but as commercial gatekeepers - they often require investments in testing, audits, and supply chain documentation that dwarf the cost savings from tariff elimination.

Indian Premiumization Meets a More Competitive EU

The FTA will also reshape competitive dynamics in Indian market. For example -

- European premium auto brands (e.g., Audi, BMW, Mercedes) will see tariff-induced price compressions. As India’s middle class grows wealthier and consumer preferences shift toward premium imported goods, demand will naturally gravitate upward. Tariff liberalization will accelerate this “premiumization” curve in consumer categories such as automobiles, branded appliances, fashion and wines.

- High-value technology-led goods (like manufacturing machines, specialized coatings or engineered stone) imported from EU producers will become more price-competitive, forcing Indian manufacturers to enhance product specifications and service quality to maintain share.

These competitive pressures also carry multiplier effects: cheaper imports create higher quality benchmarks, which in turn fuel further demand of similar products or complementary products/services, and aftermarket industries.

Compliance Costs Can Erode Tariff Gains

Contrary to simplistic estimates of a 10–20 % price advantage from tariff removal, compliance costs can be far more significant:

- Certification & Testing: European test houses often charge premium rates, especially for advanced electronics and safety-critical equipment.

- Documentation & Traceability: Multiple audits, supplier declarations and digital record keeping increase working capital and time-to-market.

- Sustainability Verification: CE, REACH and environmental due diligence requirements may require systems changes—carbon accounting, life-cycle assessments, or traceability systems.

Unless actively managed, these costs can fully offset tariff benefits, particularly for SMEs or low-margin producers.

Operational Underestimation: Most Indian Firms Could Be Under-Prepared

A pervasive issue in trade expansion is firms’ inclination to underestimate operational effort. Many Indian firms focus on tariff arbitrage but overlook:

- CE conformity processes

- REACH registrations

- Product traceability systems

- Carbon and sustainability data collection

Failure to address these domains can result in losing opportunity to compliant competitors.

Early Movers Will Capture Strategic Advantage

The landscape ahead is unmistakably one of time-bound advantage. Early adopters who invest in capability upgrades, sustainability compliance, global distribution networks can:

- Secure longer-term contracts with European buyers.

- Demand premium pricing for differentiated compliant products.

- Expand into adjacent services (installation, servicing, aftermarket support).

Delaying action increases risk. Firms that proactively build compliance, operational excellence, and market understanding now will compound advantages over the long run.

The Central Question for Indian Leaders

Ultimately, the India–EU FTA is not about whether opportunities exist, they do. The question for leaders is whether their organizations are structurally prepared to capture them. This requires vision beyond tariff math: a reimagined approach to quality systems, regulatory expertise, cross-border compliance, and operational excellence.

Firms that invest now in people, processes, technology and governance will not just survive the transition; they will define a generation of Indian global champions.

- https://www.pib.gov.in/PressReleasePage.aspx?PRID=2219065®=3&lang=2

- Press Info Bureau (PIB), India EU FTA Announcement - https://www.pib.gov.in/PressReleasePage.aspx?PRID=2219065®=3&lang=1#:~:text=In%202024%E2%80%9325%2C%20India's%20bilateral,USD%2083.10%20billion)%20in%202024

- PIB, India EU FTA Fact Sheet - https://www.pib.gov.in/PressReleasePage.aspx?PRID=2219146®=3&lang=1#:~:text=70.4%25%20tariff%20lines%20covering%2090.7,certain%20marine%20products%2C%20amongst%20others%3B

- PIB, India EU FTA FAQ Sheet -

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2220413®=3&lang=2#:~:text=Response%3A%20India%20has%20adopted%20a,into%20force%20of%20the%20Agreement - https://market-insights.upply.com/en/review-of-the-eu-vietnam-free-trade-agreement-5-years-on#:~:text=For%20Vietnamese%20exports%20to%20the,grey%20curve%20in%20figure%201

- https://www.rapidbd.org/wp-content/uploads/2023/03/Policy-Brief_50-years-of-EU-BGD_Mar14_Revised_RI_MR_11March_FINAL.pdf

- REACH - https://www.ceew.in/sites/default/files/sustainability-driven-non-tariff-measures-and-assessing-risks-foreign-trade-risks-india.pdf

- CBAM - https://ficci.in/press_release_details/5081

Disclaimer: This article is based on publicly available information and the authors’ professional experience and market analysis. For questions regarding the underlying sources or analytical methodologies, please reach out to the author directly. The analysis reflects market trends and observations and is intended for general informational purposes only. It does not constitute investment, legal, or financial advice.