UAE Electronic Invoicing — Updated Guidelines (V1.1)

Introduction

The UAE Ministry of Finance issued Version 1.1 of the Electronic Invoicing Guidelines on 1st June 2026, updating the original guidance published in February 2026.

The mandatory implementation deadlines, the Peppol-based 5-corner technical architecture, and the scope and exclusion rules are all unchanged. This update responds directly to implementation questions raised by businesses since February, providing formal regulatory clarity on three areas where businesses have asked for clarifications:

- How the data storage obligation under Article 11 applies in practice;

- How advance payments, prepayments, and retention billing must be handled at the invoice field level

- Technical clarifications covering role responsibilities, system configuration rules, and sector-specific treatment for insurance and financial services.

We have compiled this alert relying on all three source documents — the V1.0 Guidelines (February 2026), the V1.1 Guidelines (June 2026), and the accompanying regulatory analysis and is intended to give the readers a single, accurate reference across what has changed, what remains the same, and what action is required.

1. Deadlines — No critical change apart from the ASP appointment

The mandatory roll-out schedule under MD No. 244 of 2025 is unchanged. Voluntary onboarding and the pilot go live from 1 July 2026.

Who | Annual Revenue | Appoint ASP by | Go-live by |

Larger businesses | ≥ AED 50 million | Changed from 31 July 2026 to 30 October 2026 | 1 January 2027 |

All other businesses | < AED 50 million | 31 March 2027 | 1 July 2027 |

Government entities | N/A | 31 March 2027 | 1 October 2027 |

Voluntary / Pilot — all entities | Any | — | From 1 July 2026 |

e-Invoicing Applicability – UAE Branches of Foreign Entities

A UAE branch of a European entity with minimal local turnover may still be subject to UAE e-invoicing requirements if the wider group exceeds the relevant turnover threshold.

It is important to note that the AED 50 million turnover threshold does not determine whether a business is subject to e-Invoicing, it only determines when compliance must begin (as reflected in the table above).

Accordingly, the branch will be subject to e-Invoicing to the extent it conducts business transactions in the UAE, regardless of the size of its UAE operations. Therefore, the turnover that should be assessed for determining the applicable rollout phase seems to be Group wide turnover as opposed to the local turnover of the UAE branches of the foreign entities.

2. What is New in V1.1?

Topic | V1.0 — February 2026 | V1.1 — June 2026 |

Appendices | 3 appendices | 5 appendices — Appendix 4 (Data Storage) and Appendix 5 (Advance Payments & Retention) are new |

Data storage | 'Within the State' stated in Ch. 5.4 without operational guidance. | New Appendix 4: offshore/cloud hosting confirmed permissible.

|

Advance payments & retention | Brief field notes only in Ch. 12.2. | New Appendix 5: full field-level guidance on advance payments, prepayments, and milestone/retention billing sequences. |

Everything else | Scope, exclusions, timeline, format, flags, penalties — all defined. | Identical — no change. |

2.1. Data Storage — What 'Within the State' Means (New Appendix 4)

Article 11 of MD No. 243 of 2025 requires invoices and related data to be stored 'within the State.' V1.1 resolves what this means in practice for businesses using global systems.

Three conditions for compliance

- Integrity — records must be held in a system that preserves their completeness and prevents unauthorised alteration.

- Retrievability — the storage system, wherever located, must enable the business to provide records to the FTA promptly on request.

- Reproducibility — records must be producible to the FTA in complete, readable form.

Confirmed: Physical servers do not need to be in the UAE. Cloud platforms (AWS, Azure, Google Cloud and equivalents) are fully compliant provided the three conditions above are met. Geography of the server is irrelevant i.e. FTA access is what matters.

ASP-delegated storage — permitted, but legal responsibility stays with the business

- A business may contractually delegate storage of its Electronic Invoices to its ASP. The ASP can then hold the records on the business's behalf.

- This delegation does not transfer the legal obligation under Article 11. The business remains ultimately responsible for ensuring retention requirements are met.

- There is no requirement to store invoices at any specific system layer (e.g. C1 or C4). A business may choose to hold all its e-Invoices solely with its ASP, with no separate copy in its own ERPe. this is technically permissible under the guidelines, though the business must ensure the ASP agreement adequately protects its compliance position.

What counts as 'associated data'?

Only the data needed to verify the integrity, authenticity, and auditability of the invoice itself. General business records and supporting commercial documentation are not included unless directly necessary to confirm the invoice's accuracy.

Retention periods (consolidated in Appendix 4)

Record type | Standard period | Extended period |

Taxable persons | 5 years from end of tax period | +4 years during audit / dispute |

All other persons | 5 years from end of calendar year | +1 year if voluntary disclosure filed in year 5 |

Real estate records | 7 years from end of calendar year | +4 years during audit / dispute |

2.2 Advance Payments and Retention Billing (New Appendix 5)

V1.0 covered this in two brief notes. V1.1 replaces those with a dedicated appendix supposedly following industry feedback, setting out the precise invoicing sequence and fields to use.

Advance payments and prepayments

- Issue a Tax Invoice when the advance payment is received — this is the advance invoice.

- On the final invoice, record the advance amount in the 'Paid Amount' field and cross-reference the advance invoice in the 'Preceding Invoice Reference' field.

- Prepayments follow the same two-field approach.

The linkage between advance invoice and final invoice is mandatory for FTA audit traceability.

Milestone and retention billing — construction and contracting

This is key for businesses in contracting services and developers. The latest version clarifies the following:

- Issue a separate commercial document showing the total milestone value and the retention amount deducted.

- The Electronic Invoice must reflect only the net amount actually payable at that billing event, with VAT applied to that net figure.

- A separate Electronic Tax Invoice with the applicable VAT is issued when the retained amount is released and becomes payable.

3. Technical Clarifications — Confirmed in V1.1

3.1 Who is Responsible for What — Official Allocation

The guidelines clarify the following responsibilities between suppliers, buyers, and ASPs:

Activity | Supplier | Buyer | ASP |

Issuing and exchanging Electronic Invoices | ✔ | ✔ (self-billing only) | X |

Calculating all invoice values | ✔ | ✔ (self-billing only) | X |

Secure transmission using encryption | X | X | ✔ |

Contacting the buyer to obtain their Peppol Participant Identifier | ✔ | X | X |

Looking up the Peppol Participant Identifier once provided by the supplier | X | X | ✔ |

Generating a UUID for each invoice (prevents duplication) | X | X | ✔ |

Agreeing data security requirements | ✔ | ✔ | X |

Note- Even where an ASP carries out activities on behalf of a supplier, the compliance obligation remains with the supplier — or the buyer in the case of self-billed invoices.

3.2 PINT-AE System Rules — No Custom Fields Permitted

- Custom fields are not allowed: Businesses and Government Entities cannot add additional optional fields of their own into PINT-AE. Any industry-specific requirements must be discussed with the appointed ASP to find accommodation within the existing specification.

- HSN codes: Currently optional. The Ministry will announce the timeline for making HSN codes mandatory in due course. Businesses should not assume they will remain optional indefinitely.

3.3 Insurance and Reinsurance

- Any invoice or statement in the insurance sector that carries VAT implications must be issued as an Electronic Invoice — this includes reinsurance treaty portfolio statements that consolidate premiums, claims, and commissions.

- The guidelines do not prescribe who must issue the Electronic Invoice between the insurer and the broker. It is for the insurance company and broker to agree this between themselves, provided the invoice is ultimately issued through the e-Invoicing system in compliance with VAT legislation.

4. Key Implications for businesses- A Refresher

The following covers the most material compliance implications drawn from both versions of guidelines- V1.0 and V1.1, focused on points that require action or a change in existing practice.

Business type | What you need to know and do |

Large businesses ≥ AED 50M revenue | ASP appointment deadline is fast approaching. Mandatory go-live is 1 January 2027. Appoint your ASP immediately, begin ERP integration, and plan parallel testing. Penalties are active from 1 January 2027. |

VAT groups | Intra-group transactions are legally in-scope but a 24-month grace period defers mandatory compliance to 1st January 2029. Third-party invoices must comply on standard timelines. Each group entity must have its own TIN and Peppol Participant ID — the group representative's TIN cannot be used. Each member may appoint a different ASP. |

Holding companies & family offices | Pure passive income (dividends, interest) is out of scope. Any management fee, shared services charge, or cost recharge to a related party constitutes a Business Transaction and brings the entity into scope for e-invoicing/e-reporting. Review all intercompany arrangements — even those without formal contracts. |

Construction & contracting | Retention deductions and milestone calculations must not appear on the Electronic Invoice. A separate commercial document is required to show the retention working. The e-Invoice reflects only the net payable amount. A further Electronic Tax Invoice must be issued when the retention amount is released. Standard ERP invoice templates will need restructuring — this is an immediate action item. |

Financial services | Two categories of financial service are excluded from e-Invoicing: (1) Services that are VAT-exempt under Article 42 of the VAT Executive Regulation; and (2) Zero-rated exports of those same exempt services under Article 31 of the VAT Executive Regulation. Services that are standard-rated when supplied domestically are NOT excluded — even if they happen to qualify as zero-rated exports under Article 31. The starting point is always whether the service is exempt under Article 42. If it is not, e-Invoicing applies regardless of how it is rated on export. Financial services firms must map each product line individually — a blanket assumption that exported financial services are out of scope is incorrect. |

Insurance & reinsurance | Any invoice or statement with VAT implications — including reinsurance treaty portfolio statements covering premiums, claims, and commissions — must be issued as an Electronic Invoice. Insurers and brokers must agree which party will issue it. This is an internal governance question but must be resolved before go-live. |

Businesses on global cloud ERP | V1.1 expressly confirms that overseas server hosting is compliant — no UAE data centre is required. However, the business remains legally responsible for retention compliance even if storage is delegated to the ASP. Ensure your ASP or cloud vendor contract includes an obligation to make records available to the FTA on demand, and review your retrieval SLA against the standard retention periods (5 or 7 years as applicable). |

Non-UAE established businesses | Businesses without a UAE establishment but with a UAE VAT Tax Invoice obligation must issue Electronic Invoices. Register with the FTA via EmaraTax for a TIN and appoint a UAE-accredited ASP. |

5. Immediate Next Steps

Action | Who | By when |

Confirm scope — which entities and transactions are subject to e-Invoicing | Tax / Finance | Now |

Register with FTA for TIN if not already registered for any UAE tax | Tax / Finance | Before ASP onboarding |

Appoint an Accredited Service Provider (ASP) — urgent for businesses ≥ AED 50M | Finance / IT | 30 Oct 2026 |

Onboard to ASP via EmaraTax | Finance / IT | Post-ASP appointment |

Assess ERP: 8 transaction flags, line-level AED VAT amounts, XML output, no custom PINT-AE fields | IT / Systems | Now |

* NEW- Review advance payment and retention billing workflows against V1.1 Appendix 5 | Finance / Tax | Now |

* NEW- Confirm ASP or cloud storage meets three FTA retrievability conditions; review delegation terms in ASP contract (V1.1 Appendix 4) | IT / Compliance | Now |

Map intra-VAT-group transactions; note grace period expiry on 1 January 2029 | Tax / Group Finance | Recommendation to be included in initial impact assessment. Need to be before 2029 and grace period expiration |

Review financial services product catalogue — confirm which lines are exempt under Art. 42 and which are standard-rated | Tax / Finance | Pre go-live |

Align insurer/broker agreement on who will issue Electronic Invoices for reinsurance and premium statements | Finance / Legal | Pre go-live |

Add Beneficiary Name and Beneficiary ID fields to invoice templates for Free Zone transactions | Finance / IT | Pre go-live |

Build Peppol Participant Identifiers into vendor and customer master data | Finance / Procurement | Ongoing |

Test end-to-end invoice exchange and reporting with ASP | Finance / IT | Pre go-live |

6. Our Final Thoughts

The June 2026 update to the UAE e-Invoicing Guidelines is a clarification document, not a policy shift, but that should not diminish the urgency of preparation. The core deadlines remain firm.

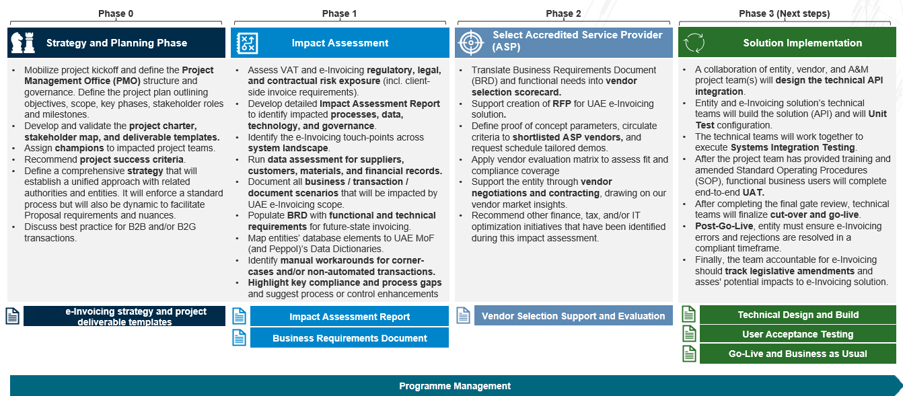

Businesses that treat e-Invoicing as an IT project rather than a cross-functional compliance programme (spanning tax, finance, legal, and technology), risk being underprepared when mandatory go-live dates arrive. The time to act is now, and we are available to assist with scope assessments, ASP selection, ERP readiness reviews, and ongoing implementation support.

At A&M, we have developed a standard comprehensive approach for e-Invoicing readiness in the UAE:

Get in touch today with one of our experts.