IRS Extends Research Credit Claim Transition Period Through January 2026

On November 25, 2024, the IRS announced an extension to the research credit claim transition period, providing taxpayers with an additional timeframe to perfect their research credit claims for refunds.[1] This extension allows taxpayers 45 days to refine their claims before the IRS makes a final determination. The new deadline for this transition period is now set for January 10, 2026.

Background on Research Credit Claim Requirements

In October 2021, the IRS outlined specific information that taxpayers must include when filing a research credit claim. These requirements were designed to ensure that claims were substantiated with adequate documentation. However, recognizing the complexities involved, the IRS made modifications in June 2024 to ease some of these requirements.

Key Modifications Effective June 18, 2024

For claims postmarked after June 18, 2024, the IRS has waived the requirement for taxpayers to provide the names of individuals who performed each research activity and the information each individual sought to discover. This change was implemented after the IRS gained significant experience with the research credit refund claims process. While these two pieces of information are no longer required at the time of filing, they may still be requested if the claim is selected for examination.

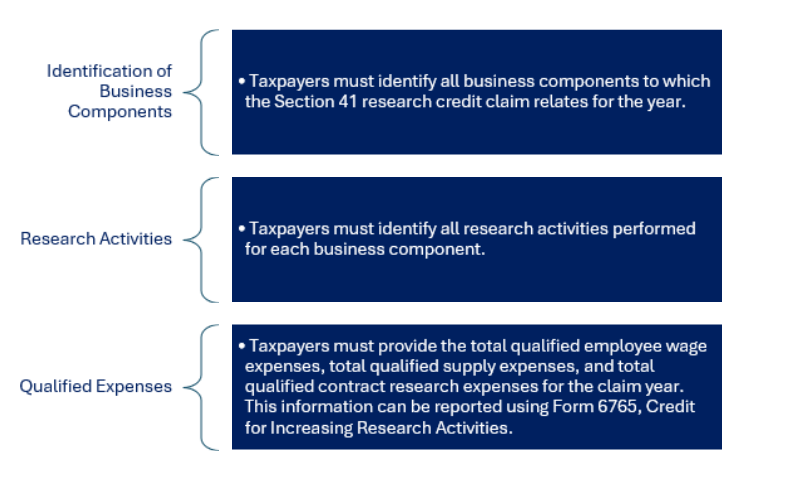

Current Requirements for Research Credit Claims

Despite the waiver of certain requirements, taxpayers must still provide comprehensive details to support their research credit claims. The following information is mandatory for claims postmarked after June 18, 2024:

Implications for Taxpayers

The extension of the transition period through January 10, 2026, offers taxpayers additional time to ensure their research credit claims are accurate and complete. By adhering to the updated requirements and utilizing the extended timeframe, taxpayers can better position themselves for successful claims and avoid potential delays or rejections.

This extension and the modifications to the research credit claim requirements reflect the IRS's ongoing efforts to streamline the process and reduce the burden on taxpayers. By staying informed and compliant with these changes, taxpayers can effectively navigate the research credit claim process and maximize their potential refunds.

Contact Stephanie Doughty to learn more.

[1] Internal Revenue Service, “IRS sets forth required information for a valid research credit claim for refund,” News release, November 25, 2024, https://www.irs.gov/newsroom/irs-sets-forth-required-information-for-a-valid-research-credit-claim-for-refund.