The Industry Continues to Battle Disrupted Supply Chains and Lower Production, While Sales and Inventories Remain Consistently Low

Through the second quarter financial results of 2022, several original equipment manufacturers (OEMs) and suppliers saw decreased profits year-over-year. Additionally, chip shortages, COVID-19, and supply chain issues continue to affect production. Auto inventories and sales both decreased in July, as unfavorable global conditions and declining vehicle demand continue.

In this issue, A&M analyzes a potential new market for OEMs, new technologies, and autonomous vehicle (AV) driving capabilities as the selected topic for the August Industry Focus.

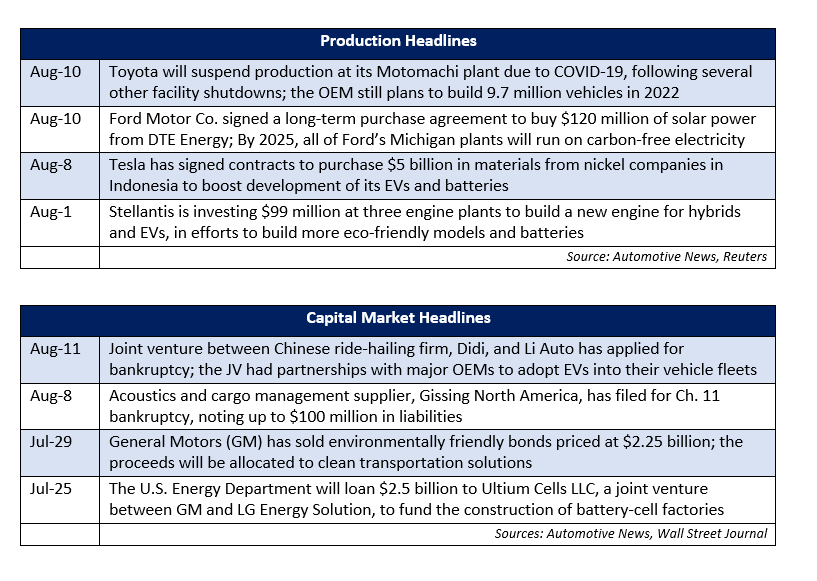

In transaction news, auto makers and suppliers continue to expand their capabilities to focus on electric technologies and batteries, along with establishing strategic partnerships.

In regulatory news, the CHIPS and Science Act was signed by the Biden Administration. The Inflation Reduction Act has also been signed by President Biden, creating several opportunities and challenges for electric vehicle (EV) manufacturers.

Additional August insights are included below.

Financial Performance

Auto Forecast Solutions’ (AFS) latest numbers show that shutdowns and delays have resulted in approximately 2.9 million lost vehicles globally during calendar year 2022. In August, approximately 185,000 vehicles have been cut from production schedules, significantly driven by losses in North America. North America is now the region most impacted by the chip crisis this year, with 1.06 million vehicles cut from production. Although supply chain issues are expected to continue into 2023, slowing vehicle demand and the passage of the CHIPS Act may provide relief to auto makers. The latest AFS estimates suggest approximately 3.8 million total cars and trucks will be affected by chip-related disruptions in 2022.

Over the past few years, several EV startups such as Rivian, Arrival, Canoo, Lordstown Motors, and others entered the market to compete directly with well-established OEMs. The EV startups raised hundreds of millions of dollars or more through both traditional IPOs and reverse mergers with special-purpose acquisition companies (SPACs). In recent months, some EV startups have noted struggles, as Electric Last Mile Solutions filed for bankruptcy liquidation and Lordstown Motors sold assets to Taiwanese contract manufacturer, Foxconn. Additionally, Rivian and Arrival have announced plans to cut costs, while both companies have common stock trading at prices considerably lower than recent highs. Rivian reported revenue of $364 million in the second quarter, while noting a net loss of $1.71 billion and expecting further increases in adjusted losses to $5.45 billion annually in 2022. EV startups are burning through cash in a market that may become more difficult to raise additional capital and are therefore racing to achieve profitable operations as soon as possible. Despite cash burn and production issues, Xos and BrightDrop have delivered 200 and 150 EVs to Amazon delivery contractors and FedEx, respectively. Rivian has also supplied Amazon with delivery vehicles, as well as Arrival starting phased trials with United Parcel Service and targeting to produce 10,000 vehicles at a later date.

Industry Update

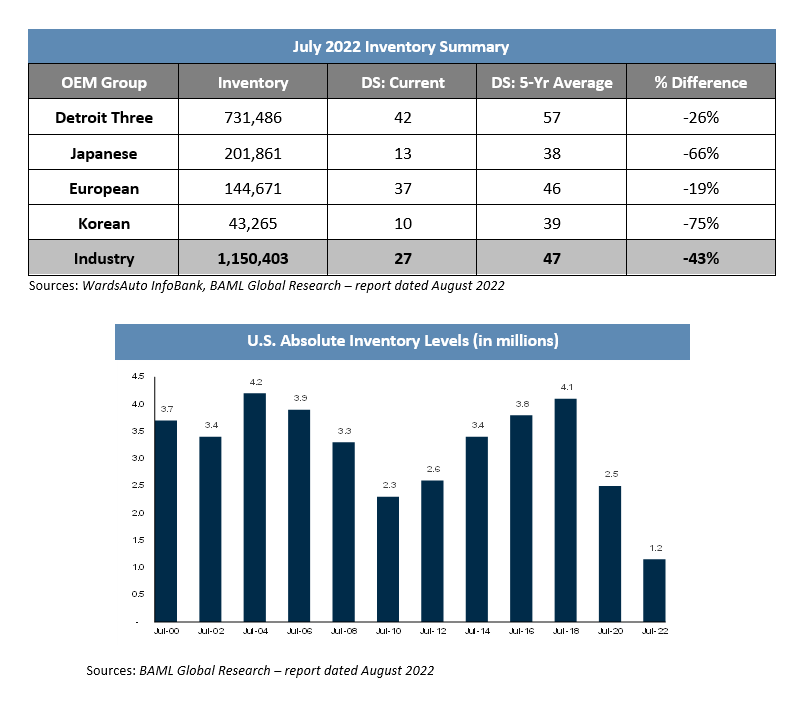

Automotive inventory decreased by 72,000 units in July, resulting in approximately 1.15 million total units. This translates to a days’ supply (DS) that is 43 percent below the five-year average at 28 DS. Inventories continue to hover around the 1-million-unit mark, as global macroeconomic conditions are impacting OEM production. Automotive inventory remains restricted, with the industry operating at recessionary production levels for approximately two years. Current inventory figures are approximately 45 percent below the five-year average, with estimates of a recovery in the mid-2020s.

New light vehicle sales in the U.S. declined 9 percent year-over-year in July with a 13.4 million seasonally adjusted annualized rate (SAAR), marking another month at SAAR levels significantly below pre-COVID comparables. July sales represent an increase from the June SAAR, but the lasting effects of a limited inventory environment and recessionary fears are resulting in constricted sales and weakened consumer vehicle demand. Inflation of 8.5 percent in July, supply chain disruptions, and material shortages continue to pressure the industry, as the current sales rate is tracking at 13.7 million units for the full year.

Industry Focus – Expanded Markets for OEMs

As OEMs and suppliers continue to invest and move into the EV era, they are simultaneously modifying their future business plans to adapt to new markets, software developments and autonomous vehicle capabilities.

In this month’s industry focus section, A&M analyzes a new vehicle market that presents unique opportunities for auto makers, as well as several different autonomous technologies and driving capabilities that will require other strategic transitions.

Mobility in Space

Since the National Aeronautics and Space Administration (NASA) announced plans to return to space, several OEMs have identified and stated intentions to develop mobility solutions for the moon. NASA’s missions, known as Artemis I, II, and III, will involve collaboration with automotive, commercial, and international partners in order to drive scientific discovery and establish a long-term presence on the moon. Due to the complexities of space, these plans come with one-of-a-kind challenges that will require various changes to OEMs’ and suppliers’ current business plans, in addition to further investments and advancements in software, EVs, and AVs.

GM, Nissan North America, Hyundai, Kia, and Toyota are among the first OEMs to establish key partnerships and create plans for the development of lunar vehicles. The group of automakers and their respective collaborators will aim to pioneer the movement for a new generation of transformative vehicles to conquer the moon’s surface.

GM, in partnership with Lockheed Martin, is designing autonomous vehicles and platforms that are multifaceted in use and able to transport astronauts and their respective gear around the lunar surface, prepare for humans landing and provide commercial payload services among other services. Furthermore, GM and Lockheed Martin have envisioned a car rental service on the moon, which will leave vehicles in space that are available for any international government-led expedition to use. GM has a history of success with vehicles in space, which include the electric Lunar Roving Vehicle (LRV) for several of NASA’s historic Apollo missions.

Nissan has designed, built, and delivered the first of three Launch Vehicle Stage Adapters of NASA’s Artemis Vehicle earlier this year, after teaming up with Teledyne Brown Engineering and Sierra Space. Hyundai and Kia have landed partnerships with six Korean organizations and Toyota has joined forces with the Japan Aerospace Exploration Agency.

The vehicles developed for space must have extreme durability and the ability to last a minimum of 10 years, while spanning multiple expeditions and withstanding intense environmental conditions. While OEMs and suppliers work through this set of rigorous challenges, the vehicular developments have the potential to accelerate advancements in autonomous driving and its respective technologies on Earth.

Autonomous Technologies and Driving Capabilities

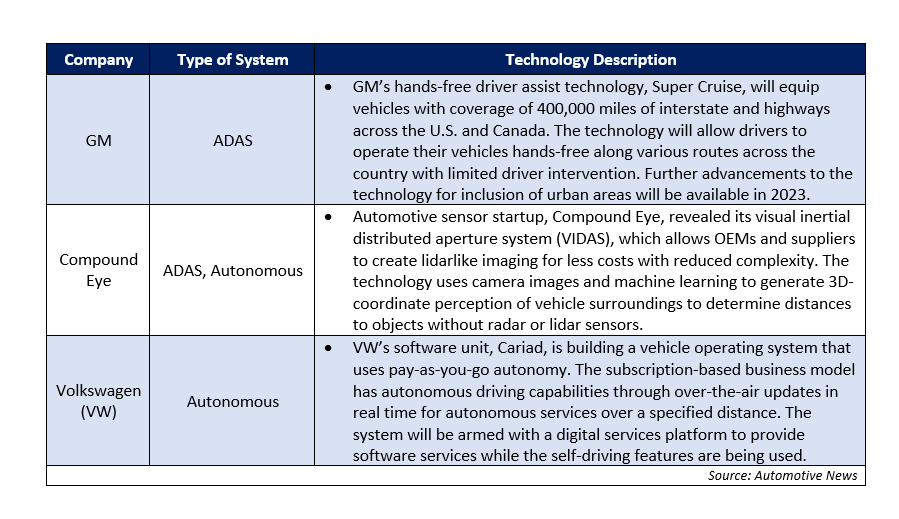

Autonomous technology is still in the developmental stage but is continuing to see significant investments from auto makers, parts suppliers, and technology companies. These technology systems can be broken down into two components: advanced driver-assist systems (ADAS) and autonomous systems. Additionally, there are various levels of autonomy when referencing vehicles, which range from no autonomy at Level 0 to full autonomy at Level 5. As the level of autonomy increases, the reliance upon human intervention diminishes, while the complexity of the underlying technology expands due to the necessity for vehicles to re-create human action. Thus, ADAS set the foundation for autonomous driving systems and provide supporting actions to drivers rather than piloting the vehicles on their own. Although ADAS do not fully automate vehicles, they are showcasing the progress and growth of the automotive industry and setting the ultimate stage for vehicle autonomy. Please see below for a chart of some of the latest releases and enhancements to ADAS and autonomous technologies.

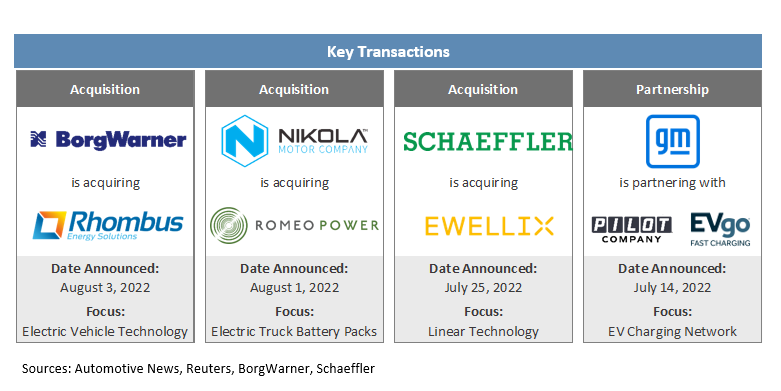

Transaction Activity

In recent transaction news, OEMs and suppliers continue to evaluate strategic opportunities to partner and create synergies for the development of EV technologies and vehicle charging initiatives. Additionally, Guangzhou Automobile Group and Stellantis have terminated their joint venture in China, resulting in a new approach for the U.S.-based OEM, as Stellantis shuts down its local factory in China and looks to import vehicles to satisfy domestic demand in China.

See below for additional detail on recently announced transactions.

- BorgWarner has acquired Rhombus Energy Solutions in a transaction valued at $185 million. The acquisition adds a North American presence to BorgWarner’s European charging business, strengthens its EV positioning and enhances the supplier’s existing capabilities in quality, engineering, supply chain, and manufacturing.

- Nikola Corporation has entered into an agreement to buy Romeo Power, an energy technology leader of advanced battery electric products, in an all-stock transaction. The acquisition will bring all battery pack engineering and production in-house, in addition to significant cost reduction and operational improvement. Nikola will use approximately $144 million in stock, valuing Romeo Power at $0.74 per share.

- German supplier, Schaeffler, will buy Sweden’s Ewellix, a global manufacturer and supplier of linear actuators, for $594 million. Schaeffler has diversified and strengthened its industrial business, ultimately preparing the supplier for future investments in attractive growth markets.

- GM, Pilot Travel Centers, and EVgo have partnered to add 2,000 electric vehicle charging stalls at approximately 500 different stations along U.S. highways. The partnership will increase overall access to charging for all EV brands and is part of GM’s $750 million investment in EV charging infrastructure through 2025. EVgo will install, operate, and maintain the nationwide DC fast charging network.

Regulatory Landscape

U.S. Court of Appeals: The U.S. appeals court recently rejected the Federal Communications Commission’s 2020 decision for a reallocation of the auto safety spectrum, which aimed to develop technology to allow vehicles to communicate with each other to avoid crashes. Despite differing views on the regulatory approach, government studies showed preventions of 600,000 crashes annually if the technology was widely adopted in the U.S.

CHIPS and Science Act: President Biden has signed the CHIPS and Science Act, which provides more than $52 billion in government subsidies for U.S. semiconductor research, design, and production. The funding also includes $2 billion to support legacy chip production and a 25 percent tax incentive for investments in chip production. The legislation aims to strengthen domestic economic growth, job creation and national security.

Inflation Reduction Act: The Inflation Reduction Act was recently approved by the Senate, House of Representatives and President Biden. The bill allows for roughly $374 billion in climate and energy spending, while limiting the $7,500 tax credit for EV purchases and requiring vehicles to be built in North America.

Vehicle Safety Tests: The National Highway Traffic Safety Administration (NHTSA) has launched five separate safety probes into approximately 1.9 million vehicles manufactured by Ford, GM, and Stellantis. The NHTSA will evaluate the safety-related issues and assess next steps in the investigation. Additionally, the NHTSA opened a probe into 1.7 million Ford and Lincoln vehicles for alleged front brake defects.

Stay connected to industry financial indicators and check back in September for the latest Auto Industry Spotlight.