Automakers Seek to Enhance Supply Chains to Aid in the Transition to Electric Vehicles

Inventory and sales numbers remained relatively stable over the past month as it appears supply is leveling off at approximately 1.0 million units. Automakers are expecting positive developments in the coming months relating to semiconductor chip supply as they continue to navigate the current volatile environment.

In this issue, A&M identifies steps organizations can take to prepare for and manage through the current crises that many suppliers are facing with supply chain disruptions and significant increases in input costs.

In the transaction market, automakers are bolstering their electric vehicle supply chains through partnerships and joint ventures while others are raising additional funds through initial public offerings.

In regulatory news, the United States is facing pushback from Canada and other countries for proposing tax incentives for the purchase of electric vehicles made by unionized American workers.

Additional December insights are included below.

Financial Performance

The latest Auto Forecast Solutions’ (AFS) numbers show that shutdowns and delays have already resulted in 10.2 million lost vehicles globally, and AFS estimates approximately 11.3 million total cars and trucks will be affected by chip-related supply disruptions. The latest AFS forecasts have been positive for domestic automakers as the forecast for total losses of North American vehicles was slightly reduced to 3.4 million units, while loss projections for international automakers have remained relatively steady from last month.

While the microchip shortage drags on, automakers continue to identify opportunities to work through the supply issues and maintain optimal performance. BMW and Stellantis both recently agreed to deals directly with semiconductor manufacturers to secure chip supplies, which signals that automakers are willing to sidestep traditional suppliers to fortify their supply chains. Volvo believes chip supply will continue to improve each month, but despite losing production, the automaker actually improved overall financial performance last quarter through better pricing on sold models. According to J.D. Power, 87 percent of all new vehicles purchased in November by individual customers sold at or above the sticker price; this figure is up from 75 percent at the midpoint of 2021 and far above the pre-pandemic average of 36 percent. Toyota’s announcement that in January 2022 it expects to produce a record number of vehicles for the month, despite cutting production in December, mirrors the sentiment that the industry will see incremental supply improvements each month.

Industry Update

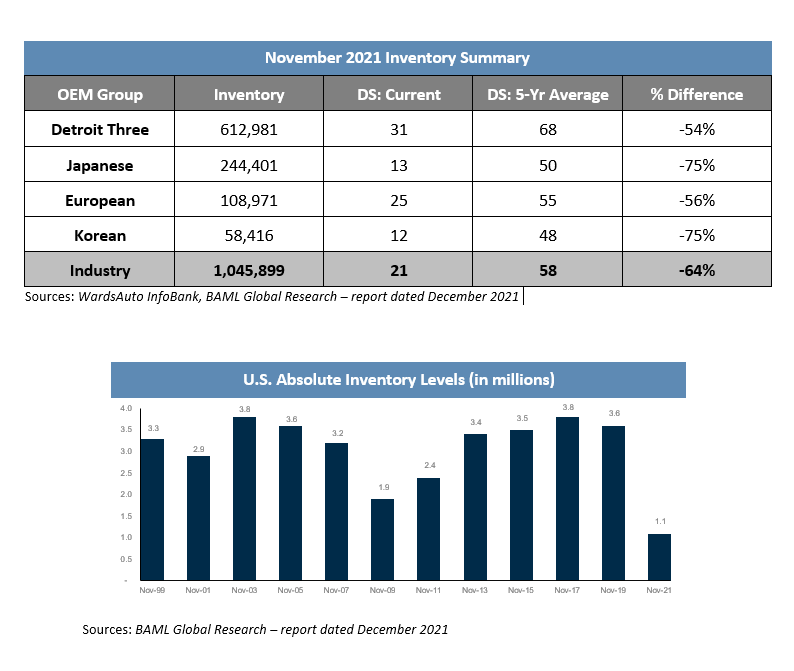

Automotive inventory increased by 29,000 units in November, resulting in approximately 1.0 million total units. This translates to a days’ supply (DS) that is 64 percent below the five-year average at 21 DS. November is the second consecutive month of an absolute increase in inventory, but it appears that the inventory levels are leveling off at a trough of approximately 1.0 million units rather than materially improving. Additionally, new light vehicle sales remained low as the 12.9 million seasonally adjusted annualized rate (SAAR) of sales in November was a slight deterioration from October. With SAAR levels not showing a consistent trend during the past few months, it is unclear when sales will sustainably begin to improve.

Total new light vehicle sales in the U.S. for 2021 is pacing towards approximately 15.0 million units, which is only a slight improvement from the 2020 Covid-induced trough of 14.5 million units. 2021 sales have been heavily affected by the ongoing supply issues, which remain volatile with low visibility. IHS Markit continues to expect stabilization of the supply environment to occur in the second half of 2022 with inventory recovery and restocking not occurring until 2023.

Industry Focus – Crisis Management

The automotive industry is experiencing unparalleled global operational issues, essential material shortages, significant inflation in all input costs and a disruptive transformation to electrification. Although demand for light vehicles remains strong, many automotive suppliers are finding themselves dealing with crises approaching levels of the Great Recession. The most successful suppliers are the ones who prepare and actively manage through crises and transition by understanding the necessary financial and operational levers to pull to fortify the company before and through a crisis. A&M has identified two main goals for executives to ensure organizations are well equipped for the current crises: (1) preserving or improving liquidity, (2) and developing realistic scenarios for the range of potential outcomes and identifying actions to take based on changing circumstances.

Preserving/Improving Liquidity

From a financial standpoint, cash is the top priority in a crisis. Liquidity measures should be understood and prioritized, replacing historical focuses on growth, margins, and cost efficiency. Crisis demands bold and decisive action, with an unrelenting focus on pivoting to cash.

It is crucial to understand the difference between cash reflected in the financial statements and available liquidity. Cash shown in the financial statements may be outdated, distributed throughout the world, or restricted for required debt-related covenants. Therefore, it is imperative for automotive suppliers to understand how much cash is truly available, the restrictions to freeing up cash and levers to boost liquidity in the short and medium term.

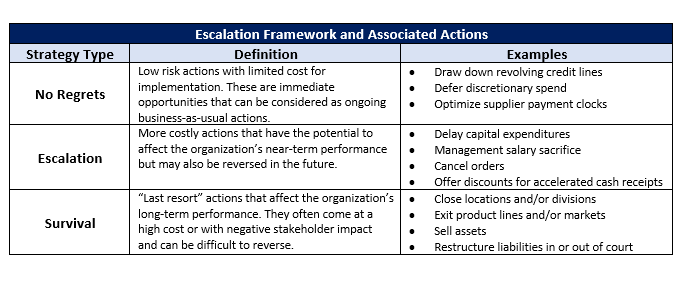

A critical tool for liquidity management is the 13-week cash forecast. This cash forecast helps form a baseline understanding of liquidity, and organizations that do not utilize a weekly cash forecast should develop one immediately. To extend the “runway” of liquidity and maximize flexibility, organizations should develop a series of escalation strategies; an escalation framework and associated actions are described further in the below table.

Introduce Scenario Planning

The weekly cash forecast is complemented by the development of business plan scenarios that contemplate the path out of the crisis. It is critical that scenarios incorporate assumptions that are based in reality, along with sensitivities for downside and upside cases. Too often, organizations view the future with rose-colored glasses and business plans contain assumptions they would like to see happen rather than what could happen. Ignoring the potential range of outcomes limits an organization’s ability to plan for these outcomes and begin taking action early. Examples of situations that are often ignored until too late are potential covenant violations in credit agreements and accepting losses from operations based on an expectation that conditions will improve in the near term.

Business plan scenarios should cover a long-term period of approximately three to five years, while having special focus on the immediate four-to-six-month period with defined initiatives, milestones, and resource allocations. Organizations should also stress test each scenario against their cash forecast and liquidity metrics to analyze any further potential business changes. Organizations should ensure they have the right leadership to execute on the plan, sufficient capital for implementation and a definitive process to monitor performance in real time.

Executives and management often have difficulty accepting how bad a situation truly is or can become. It is crucial that organizations are realists as it is necessary to be proactive rather than reactive when it comes to crisis decision making. Throughout this process, it can be extremely helpful to hear from peer companies and outside advisors on important business and legal items to confirm all considerations have been taken into account.

Transaction Activity

In recent transaction news, Volkswagen is rumored to be contemplating an IPO for its luxury brand, Porsche, to fund its shift towards software and electric vehicles. While no official decision has been made, a Porsche listing is expected to bring a valuation of approximately $50-100 billion. GM battery supplier LG Energy is aiming to raise as much as $10.8 billion through an IPO. The offering could give LG Energy a valuation of approximately $59 billion despite recent concerns over fires involving its batteries that resulted in a recall of Chevy Bolts. Additionally, Daimler and Stellantis both plan to invest in solid-state battery maker Factorial Energy. Solid-state batteries are a potential next generation of battery technology that includes faster charging, better energy storage, and improved safety.

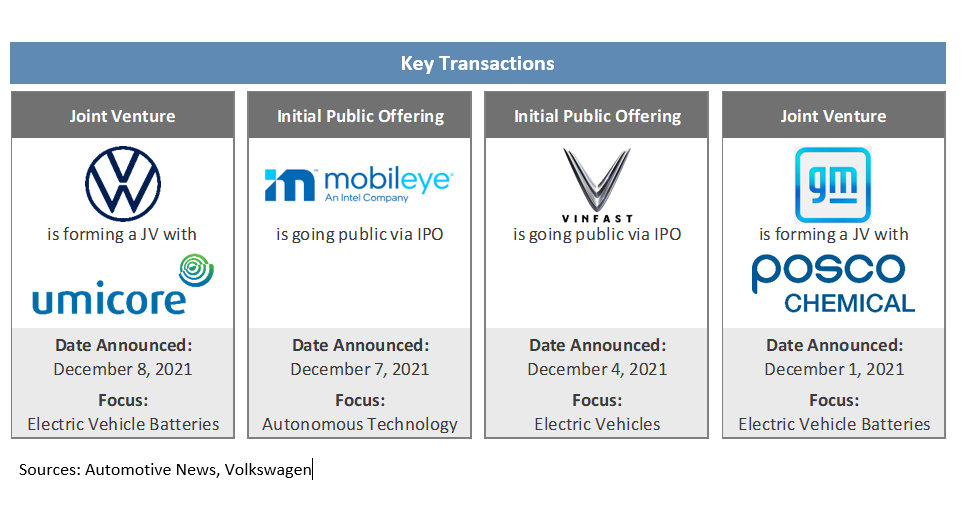

See below for additional detail on recently announced transactions.

- Volkswagen is forming a joint venture with the chemical and recycling company Umicore to produce key materials for battery cells. The venture aims to supply cathode materials, which greatly affect battery performance, safety and cost, to Volkswagen’s European battery cell factories. In addition, Volkswagen also recently announced an agreement with Vulcan Energy Resources for lithium as well as an investment in battery startup 24M.

- Semiconductor company Intel plans to take its self-driving car business, Mobileye, public in 2022. Intel will remain the majority owner in the transaction as the chipmaker looks to capitalize on the growing autonomous vehicle industry by listing shares of the business unit.

- Electric vehicle company VinFast is planning an initial public offering in the United States during the second half of 2022. VinFast could raise up to $3 billion from the transaction at a valuation up to $60 billion, but the Vietnamese company is unsure at this time if it will pursue a traditional IPO or a SPAC merger.

- GM is forming a joint venture with Posco Chemical, a Korean advanced materials company. The aim of the venture is to process cathode active material for use in GM’s Ultium batteries in North America by 2024.

Regulatory Landscape

EV Charging Network: President Biden and his administration released a strategy for building a nationwide network of electric vehicle charging stations. Last month, President Biden signed an infrastructure package into law that includes support for electric vehicle charging, and this proposed strategy will “establish a more uniform approach, provide greater convenience for customers, and offer increased confidence in the industry”.

Federal Fleet Going Electric: President Biden signed an executive order which includes the federal vehicle fleet only acquiring zero-emission vehicles by 2035. The U.S. government owns more than 600,000 vehicles and the executive order also pledges for 100 percent zero-emission light duty vehicle acquisitions by 2027.

EV Tax Credits: After the U.S. proposed a tax incentive for electric vehicles made by unionized American workers, Canada has proposed a deal to align electric vehicle tax credits with the U.S. The Canadian government has stated it may impose tariffs in response to the tax credit and Mexico and the European Union have also expressed concerns.

U.S. Vehicle Fuel Economy: The U.S. Environmental Protection Agency (EPA) said the fuel economy for new vehicles hit a new high in 2020 at 25.4 miles per gallon. However, most automakers relied on credits to meet federal emissions requirements and the expectation is that the industry’s fuel economy for 2021 will decline. The EPA report also cited the Detroit 3 automakers of GM, Ford, and Stellantis as lagging behind other automakers in fuel economy performance.

Stay connected to industry financial indicators and check back in January for the latest Auto Industry Spotlight.