Production cuts increase as chip shortage and supply chain issues persist

Automotive suppliers face down another difficult year as industry macro conditions remain volatile and growing electric vehicle (EV) volumes add significant operational complexity. U.S. tax incentives and state grants continue to drive manufacturing investment domestically. Inventory continues to mix toward large vehicles as automakers take action to manage truck inventory.

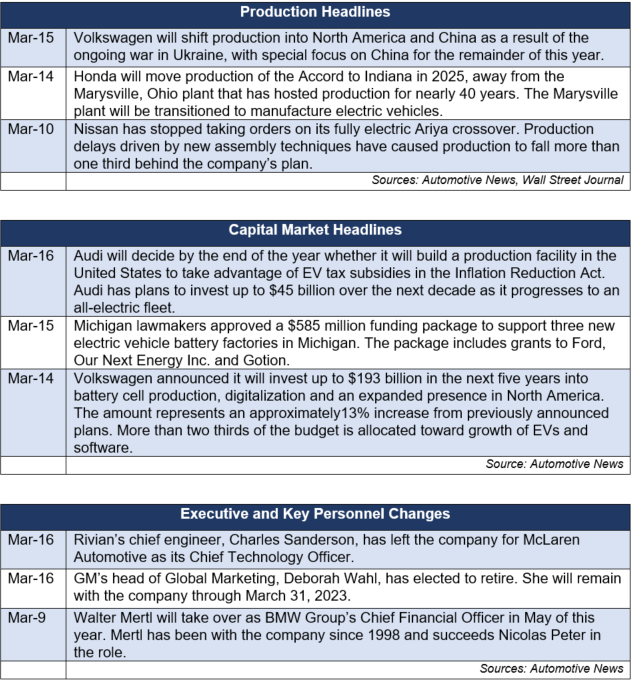

In transaction news, Lithia has acquired Jardine Motors Group to officially expand into the U.K. PDF Solutions and Voltaiq are partnering to lead electric battery improvements through analytics and machine learning. Cox Automotive has acquired FleetNet America to expand its service network and mobile app offering.

In regulatory news, Ford and Honda have announced significant safety recalls totaling approximately 1.7 million vehicles. The Department of Transportation is applying further scrutiny to Tesla’s Autopilot system as the Department of Justice investigation continues.

Additional March insights are included below.

Financial Performance

North American automakers eliminated approximately 344,000 vehicles from their 2023 worldwide production plans in March because of further escalation in the ongoing global microchip shortage, according to AutoForecast Solutions (AFS). The updated estimate more than triples the previous year-to-date total losses to approximately 478,000 vehicles for the region, causing manufacturers to frontload production cuts for the year. AFS still expects approximately 2.8 million vehicles will be cut from production plans for lack of chips in 2023, down from 4.38 million in 2022 and 10.56 million in 2021.

Automotive suppliers largely underperformed consensus profitability targets in Q4 and FY 2022 after a difficult operating year, marred by supply volatility and record low inventory levels for automakers. Outperformers, such as Michigan-based BorgWarner, have focused primarily on efficiency and growth in the electrification of their business and cite 2023 as an inflection point for the automotive supply industry.

Industry Update

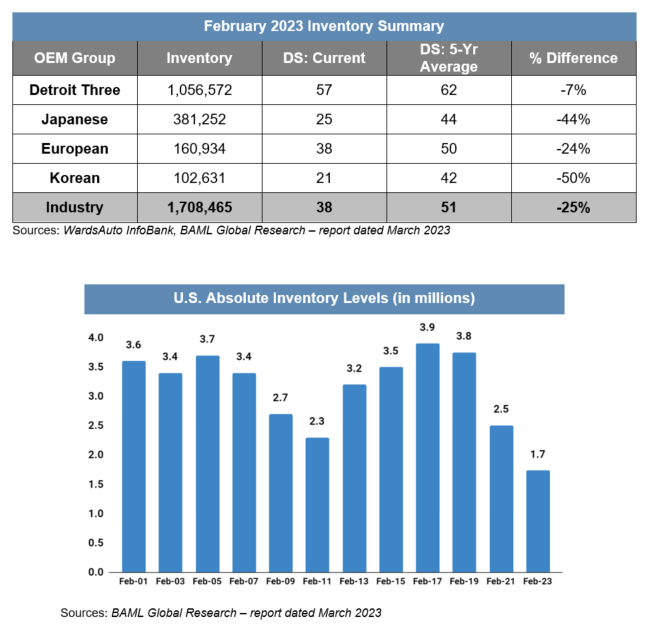

February inventory levels ended at 1.74 million units, their highest level since April 2021. Days’ supply (DS) closed at 38, approximately 25 percent below the five-year average, consistent with the last several months of results. Inventory mix continues to shift toward trucks and large vehicles as OEMs prioritize higher margin segments, with inventories in these categories approaching pre-COVID levels. Furthermore, GM has taken steps to manage truck inventory as it announced production cuts to its Fort Wayne plant that manufactures the Sierra and Silverado.

February U.S. light vehicle sales increased 8.5 percent year over year, beating consensus estimates from Bloomberg. Vehicle mix continues to improve to record levels of large vehicles as average transaction prices remain steady but are elevated compared to this time last year. Expectations for full year 2023 remain moderate based on continuously growing production cuts, but signs continue to point toward a steeper recovery in 2024.

Industry Focus – Supply Chain Challenges Linger for the Year Ahead

The automotive supply chain faces a difficult near-term future as OEMs look to ramp up production of EVs. Continued pressure from an inflationary macroeconomic environment has caused historic financial strain for automotive suppliers, in addition to one of the most complicated operating environments in a century.

As federal legislation places increasingly difficult requirements on tax credits tied to EVs, sourcing of raw materials and components for EVs presents a significant challenge. Complexity of running dual-track programs for both internal combustion engines (ICEs) and EVs has spread human capital thin, stretched delivery timeliness and quality and driven profitability down despite many suppliers returning to pre-pandemic revenue by the end of 2022.

Component and Mineral Sourcing

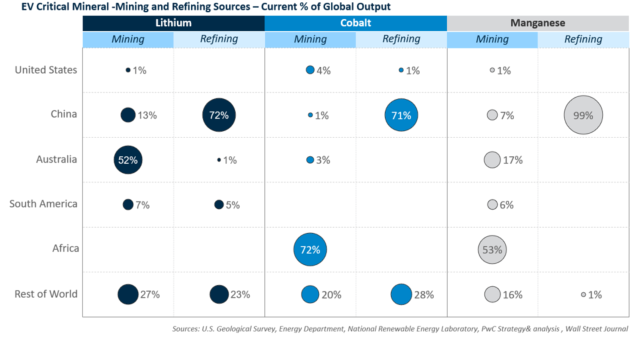

Recently introduced legislation that would shake up battery and mineral sourcing requirements for electric vehicles may have meaningful implications for EV suppliers. One of the biggest issues the automotive industry faces in a transition to EVs is reliable and cost-efficient sourcing of key raw materials like lithium, nickel, manganese and cobalt.

The vast majority of current mining for these metals falls outside the U.S. and is heavily concentrated in specific countries or regions, depending on the metal. Refinement processes for the metals once they are mined are even more geographically limited, with China processing approximately 70 percent of the world’s lithium and cobalt and 99 percent of the world’s manganese. Furthermore, prices for these minerals are reaching record highs. Geopolitical shifts may further complicate the quality and quantity of future supply available to U.S. suppliers.

Program complexity and OEM uncertainty

While the rapid growth of EV programs has helped suppliers return to pre-pandemic revenue levels, the complexity of dual-track programs for EVs and ICEs has placed significant strain on suppliers and their profitability. Wage inflation, chip shortages and production volatility have been significant contributors to the difficult operating environment suppliers face, on top of difficulties attracting and retaining top talent.

The component profile of EVs versus traditional ICE vehicles adds another significant challenge for suppliers: traditional ICE vehicles require approximately 600 semiconductor chips where EVs typically require more than 1,300. Given chips in EVs control a significantly higher number of major functions compared to ICE vehicles, the need for a robust supply chain is essential for suppliers. Relief is expected for the domestic supply of chips with last year’s passing of the $280 billion federal CHIPS and Science Act.

Suppliers that operate on a just-in-time basis have had a notably tougher time adapting to operating conditions based on manufacturer production volatility. While a majority of suppliers have struggled with the volatility, recent earnings reports suggest that suppliers that have had success in passing on price increases to OEMs are sitting in better positions.

Transaction Activity

A significant geographic expansion for Lithia, one of the largest dealership groups in the U.S., leads the way in transaction news this month. Focusing on improving the future of EV battery production through analytics and machine learning, PDF Solutions and Voltaiq have announced a new partnership. In the dealership technology space, Cox Automotive has acquired FleetNetAmerica to expand its service network and mobile app offering.

See below for additional detail on recently announced transactions.

- (3/16) Lithia Motors has acquired Jardine Motors Group, marking the dealership group’s entrance into the U.K. The deal adds approximately $2 billion in revenue to Lithia’s existing $28 billion revenue base (2022 FY result) across more than 40 luxury dealerships in the U.K.

- (3/9) PDF Solutions and Voltaiq announced a partnership designed to improve data collection, analytics and production speeds for EV batteries. PDF Solutions is a Santa Clara, California-based company that provides analytics and machine-learning for semiconductor manufacturers, while Voltaiq creates software to analyze EV battery function. The partnership hopes to drive improvements for domestic battery manufacturers to keep pace with global competitive standards.

- (3/3) Dealership technology provider and wholesale auction company Cox Automotive has acquired fleet maintenance and repair service provider FleetNet America for $100 million. The acquisition will add more than 60,000 independent service providers and includes FleetNet’s mobile app.

Regulatory Landscape

Ford Recall: Ford will recall nearly 1.3 million Ford Fusion and Lincoln MKZ vehicles globally for a braking defect. The defect affects vehicles made from 2013 through 2018 and can cause front brake hoses to rupture and leak brake fluid, leading to reduced rates of deceleration. There is one known reported accident related to the defect with no mention of injury.

Honda Recall: Honda will recall nearly 450,000 CRV, Accord and Odyssey models built between 2017 and 2020. A manufacturing issue with the front seat belts is preventing proper latching. As of March 2, the company had received more than 300 warranty claims related to the defect and will send recall notices on April 17.

Tesla Autopilot: U.S. Transportation Secretary Pete Buttigieg said this week that Tesla’s name for its trademark driver-assistance system is misleading and lacks “common sense.” While the Department of Transportation does not have any authority over the system’s naming convention, the U.S. Justice Department’s investigation into whether Tesla has made misleading statements about the system’s capabilities remains open.

Stay connected to industry financial indicators and check back in April for the latest Auto Industry Spotlight.

Automotive Industry Spotlight Archive