Industry Supply Chain Issues Further Exacerbated by Russia-Ukraine Conflict

Production shutdowns and delays are accelerating as issues with sourcing and supply continue. Industry performance remained depressed as automotive inventory decreased slightly in February, a month which historically is for inventory build.

In this issue, A&M analyzes how the Russian invasion of Ukraine is affecting the automotive industry as the selected topic for the March Industry Focus.

The transaction market remains busy as automakers partner with startups and technology companies to gain exposure to innovative technologies.

In regulatory news, the United States government is implementing rules and standards to accelerate and support the transition to electric vehicles.

Additional March insights are included below.

Financial Performance

Auto Forecast Solutions’ (AFS) latest numbers show that shutdowns and delays have resulted in 930,000 lost vehicles globally during calendar year 2022, a significant increase from the prior week estimate of 656,000. European automakers axed approximately 110,000 additional units in the past week, while plants in Asia (not including China) added 106,200 cuts in the same period. The latest AFS estimates suggest approximately 1.66 million total cars and trucks will be affected by chip-related disruptions in 2022.

While the semiconductor shortage remains a major issue, the recent Russian invasion of Ukraine has added another large variable for future industry performance. The CEO of Volkswagen warned that the conflict could be much worse than the pandemic and the interruption “could lead to huge price increases, scarcity of energy, and inflation.” The March Industry Focus section expands further on how the Russia-Ukraine conflict will affect the automotive industry.

Industry Update

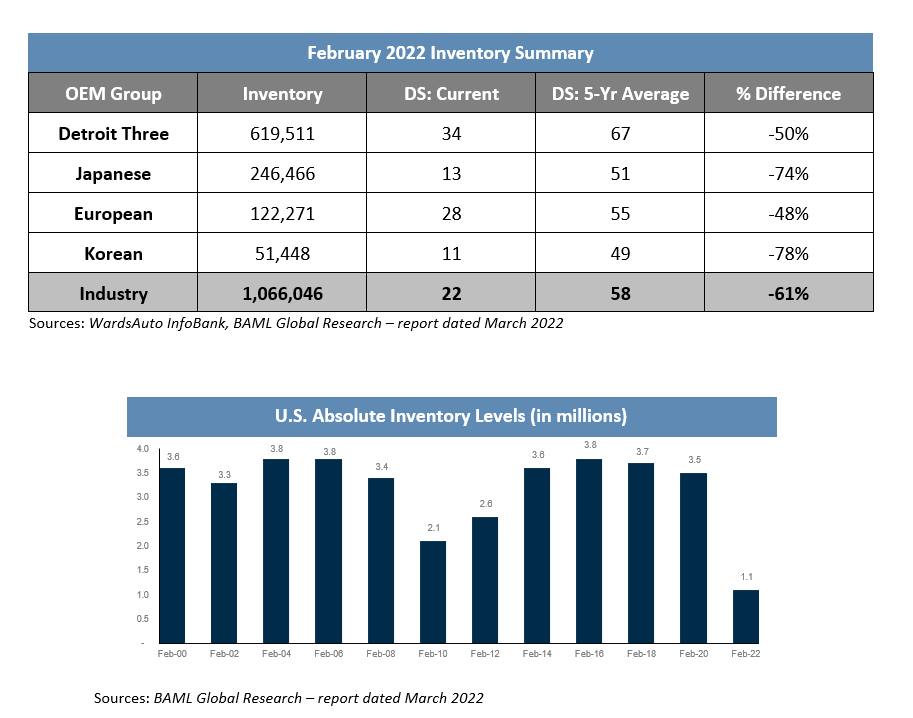

Automotive inventory decreased by 3,000 units in February, remaining at approximately 1.1 million total units. This translates to a days’ supply (DS) that is 61 percent below the five-year average at 22 DS. February is historically a month of inventory build prior to the spring and summer selling seasons, so this figure does not bode well for a robust sales recovery in the near-term. The industry likely will not face further significant deterioration with inventory stabilizing around 1 million units on-hand, but production continues to constrain the industry.

New light vehicle sales in the U.S. declined 12 percent year-over-year in February with a 14.1 million seasonally adjusted annualized rate (SAAR) of sales. While this is a decline from the January SAAR, the result is not surprising given the seasonal trend of February being a low sales month. However, there are a variety of warning signs from broader economic environment, such as falling consumer confidence, COVID resurgences, the Russia-Ukraine conflict and other economic indicators, that makes year-over-year sales growth in 2022 highly unlikely. Despite the turmoil caused by the current inventory and sales performances, it will likely lead to a more robust recovery in future years.

Industry Focus – Russia-Ukraine Conflict: Impacts on the Auto Industry

With the ongoing conflict in Eastern Europe, A&M’s March industry focus section analyzes the effects of Russia’s invasion of Ukraine on the automotive industry.

After weeks of tension, Russia officially invaded Ukraine on February 24. The invasion in this region took little time to start wreaking havoc on the automotive industry. NATO affiliated countries, which house most of the major OEMS, placed sanctions against Russia, which ultimately led to the suspension of foreign operations and stoppages of incoming shipments to Russia. There is significant uncertainty surrounding when or if OEMs will return to Russian operations and how each organization will adjust to the disruptions.

The Russian automobile industry has sold between 1.6 million and 1.75 million units in each of the three previous years, resulting in approximately 2 percent of global vehicle sales in 2021. AFS estimates currently expect Russian automobile output to be cut roughly in half in 2022, but a few notable OEMs comprise most of the Russian automotive market and will be the most heavily affected. Renault accounts for 39.5percent of Russian vehicle production, followed by Hyundai at 27.2percent, Volkswagen at 12.2 percent, and Toyota at 5.5 percent, while other automakers have low percentages of the market. Given the relatively small size of the Russian automotive market, experts do not believe that automakers will prioritize reinvesting in Russia anytime soon.

Raw Material, Auto Parts and Supply Chain Shortages

Both Russia and Ukraine are a main access point for key gases, metals, and raw materials used in the production of automobiles and semiconductors. Many of these components are experiencing shortages and are irreplaceable when it comes to manufacturing.

Major automakers, such as VW, BMW, and Mercedes Benz have cut back production and adjusted shifts at assembly plants in Western Europe during March because of the material shortages. These auto manufacturers typically have access to Western Ukraine, which carries a highly skilled, low-cost workforce with close proximity to Europe’s car factories. Furthermore, Ukraine’s wealth of raw materials has allowed this area to grow into a major production hub, particularly for wire harnesses. Wire harnesses are an essential but niche vehicle input which makes sourcing extremely difficult. Without this access, the wire harness supply chain has shattered, and the industry may have to invest in new equipment and production facilities. Automotive News Europe has stated that the parts shortages due to wire harnesses could affect roughly 15 percent of European auto output, which translates to ~700,000 vehicles.

On top of automotive component parts, there are several metals that are seeing price increases and reduced output due to the Russian invasion of Ukraine. These metals include aluminum, high-grade nickel, palladium, and more. Despite metals not being the target of Russian sanctions, price increases are a significant side effect for withdrawing ties from Russia. Palladium and nickel are especially important, as they are crucial parts of catalytic converters and EV batteries, respectively. This is ultimately putting more pressure on OEMs, who are still working through the semiconductor crisis and high energy and metal prices experienced before the conflict in Ukraine.

Given the ongoing semiconductor shortage, automotive supply chains are also vulnerable to shortages in neon and palladium, both of which are critical to chip production. Ukraine and Russia both play a role in the creation of neon gas, as it is a byproduct of Russian steel manufacturing that is later purified in Ukraine. Ukraine is the primary source for neon, providing approximately 70 percent of the global output. Historically, a conflict between the two nations in 2014 yielded a 600 percent price increase when Russia annexed the Crimean Peninsula from Ukraine. Additionally, Russia supplies approximately one-third of the world’s palladium used in semiconductors.

Automakers are being forced to find alternative sourcing and reconfigure supply chains to account for the Russia-Ukraine conflict. While the war is affecting the entire industry, see below for a graphic of automotive companies which have suspended production or halted exports in Russia and Ukraine.

Oil and Gas Prices

Russia’s economy is largely based on energy, and several countries are dependent on Russian energy sources. According to the EIA, in 2021, Russia was the largest natural gas exporting country in the world, the second-largest crude oil and condensates exporter, and third largest coal exporter.

Prior to the current conflict in Eastern Europe, the price of gasoline was already on the rise, but has since been exacerbated with a 23 percent price increase when compared to the start of the year, according to the New York Times. Gas prices are known to fluctuate in tandem with the cost of crude oil, which are both likely to continue increasing, as the U.S. and Britain have announced a ban on the import of Russian oil. Chief Economist of Moody’s analytics, Mark Zandi, expects the world oil price to reach $150 per barrel, representing a gasoline price of $5 per gallon or more in most parts of the country.

Transaction Activity

In recent transaction news, Intel’s autonomous vehicle unit Mobileye has confidentially filed for a U.S. IPO as Intel looks to take advantage of consumer demand for developing technologies. Motional, an Aptiv and Hyundai joint venture, announced it will be launching a free robotaxi service in downtown Las Vegas with ride services company Via. In addition, Swedish automaker Polestar announced it is collaborating with a variety of suppliers to accelerate its development of a climate neutral vehicle by 2030. These are just a few of the latest examples of the automotive industry leveraging partnerships both inside and outside of the industry to enhance innovation and accelerate the implementation of next-generation technologies.

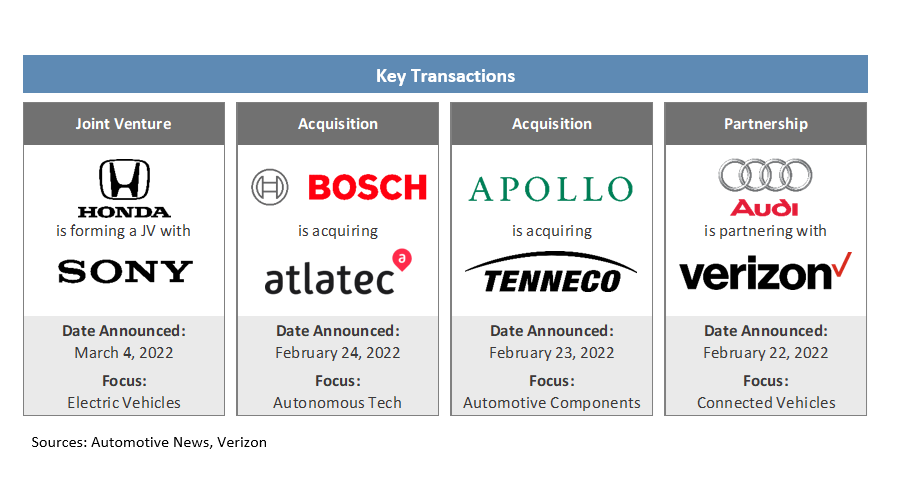

See below for additional detail on recently announced transactions.

- Honda is forming a joint venture with technology giant Sony to develop and sell electric vehicles by 2025. Honda will manufacture the vehicle and believes that partnering with a technology company is crucial for innovation.

- Supplier Robert Bosch is acquiring German 3D-mapping company Atlatec to boost the development of automated driving systems. Bosch believes digital maps will play a crucial role in the development of automated vehicles and this acquisition further expands their autonomous expertise.

- Diversified automotive supplier Tenneco will be acquired by private equity group Apollo Global Management in a deal valuing the company at $7.1 billion. Apollo will pay $20 per share, approximately double the current trading price, in a deal that will remove Tenneco from the New York Stock Exchange as the supplier goes private.

- Audi is partnering with Verizon to add 5G connectivity to the automaker’s U.S. vehicle lineup. This is Verizon’s first agreement with an automotive company, and the 5G capabilities are estimated to be included with select Audi models in 2024.

Regulatory Landscape

Autonomous Vehicle Standards: The National Highway Traffic Safety Administration (NHTSA) has eliminated the need for automated vehicle manufacturers to equip fully autonomous vehicles with manual driving controls to meet crash standards. Previously, automakers have faced significant hurdles to deploy autonomous vehicles without human controls due to outdated standards, but the new focus will be on providing the same safety standards as human-driven vehicles.

Tesla Autopilot and Automated Features: Tesla defended the safety benefits of their advanced driver assistance system Autopilot and other autonomous capabilities but acknowledged that constant monitoring and attention of the driver is required. The letter came as a response to a letter penned by Democratic senators raising safety concerns over Tesla’s automated technology, and the senators claim the Tesla response is “just more evasion and deflection”.

California Emissions Standards: The Environmental Protection Agency (EPA) has reinstated a waiver under the Clean Air Act, which allows California to pursue its own tailpipe greenhouse gas emission standards and zero-emission vehicle (ZEV) mandates. The EPA’s decision comes as the California Air Resources Board is developing regulations that would accelerate the transition to ZEVs and strengthen emission standards for new light-duty and trucks sold in the state.

States Challenge New EPA Standards: A group of oil refiners, ethanol producers, and 16 states have challenged the EPA’s tougher vehicle emission requirements that reverse a rollback issued by former President Trump. The new rules aim to speed the U.S. shift to electric vehicles and will take effect in 2023.