Is Healthcare Spending Really Dropping?

A recent New York Times article entitled “Health Spending Rises Only Modestly” highlighted 2013 as the year with the lowest rate of increase in healthcare spending since recording began in 1960.1 One day earlier, the White House published the following statement on its blog: “Today’s data make it increasingly clear that the recent slow growth in the cost of health care reflects more than just the 2007–2009 recession and its aftermath, but also structural changes in our health care system, including reforms made in the Affordable Care Act.”2

Healthcare is a $3 trillion industry with significant variation in local market demographics and socio-economics, care-delivery fragmentation, efficiency and effectiveness, as well as competitive intensity. Alvarez & Marsal (A&M)’s analysis suggests that the growing local market power of hospital-led health systems and insurance companies is “squeezing” downstream costs without necessarily enhancing clinical outcomes or operational efficiencies on a commensurate level. The messaging of reform far exceeds the reality of change. This article seeks to provide supporting evidence to our hypothesis.

Lower growth rates reflect embedded inefficiencies

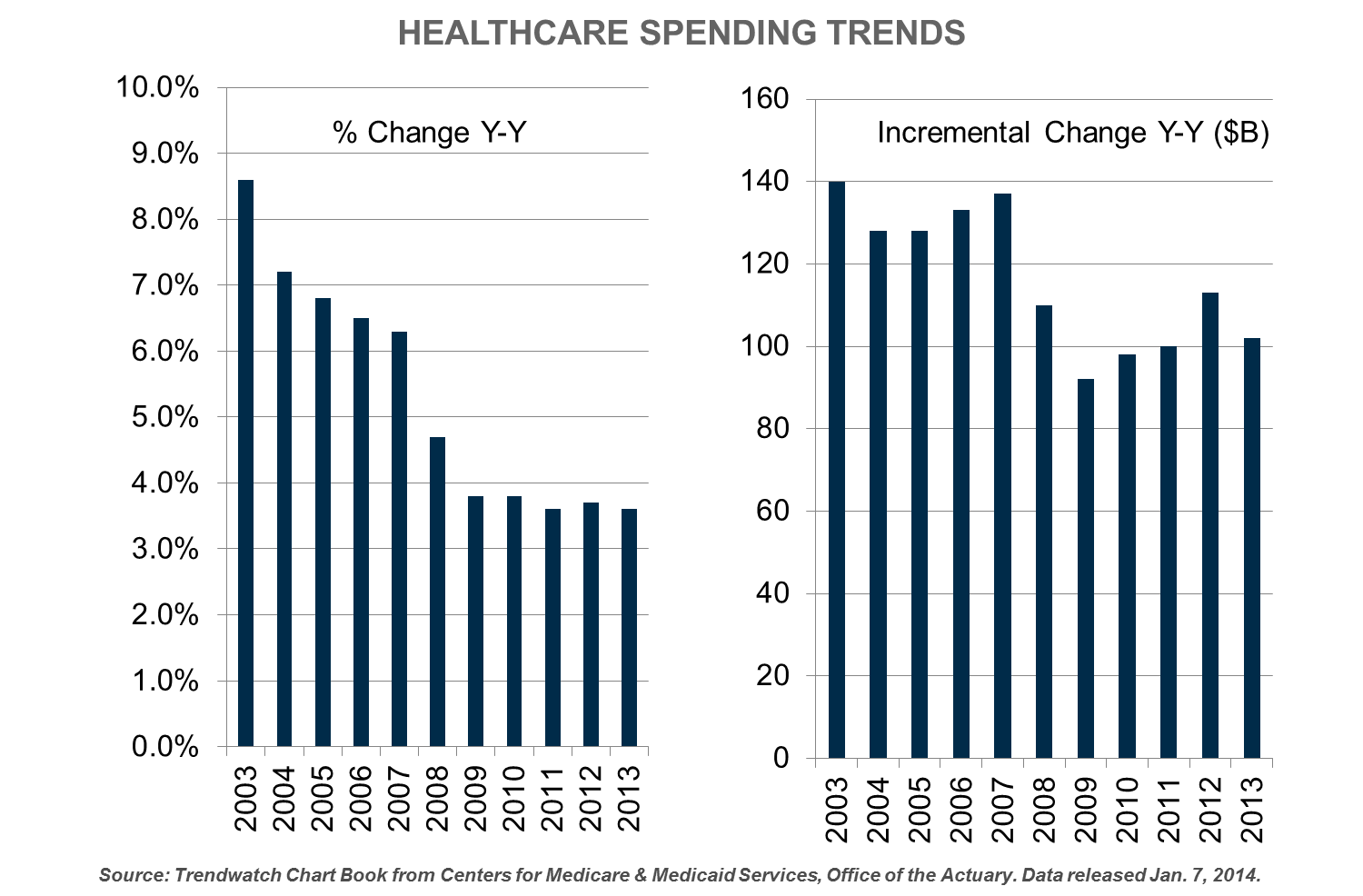

National health spending in 2013 increased 3.6 percent, consistent with growth rates seen since the onset of the “Great Recession” in 2008.3 Expenditures of $2.9 trillion represent 17.4 percent of the national GDP. A&M believes the high rate of baseline spending, combined with annual incremental outlays of $102 billion, is a better indicator of embedded care delivery inefficiency and ineffectiveness than the less imposing annual percent change.

Touted Pioneer ACO cost savings may stem from market attributes

The CMS Pioneer Accountable Care Organizations (ACO) Model, launched in January 2012 with 32 participants, was designed for providers experienced with care coordination across multiple settings. Year 1 results highlighted improved quality scores for ACO participants relative to their Fee-for-Service (FFS) peers (risk-adjusted re-admissions, patient / caregiver satisfaction, preventive health, at-risk population management). Eighteen of 32 Pioneer ACOs (56 percent) also had lower costs, but only 13 of 32 (38 percent) had sufficiently lowered costs to generate shared savings. Nine ACOs dropped out after Year 1 indicating the challenge of reducing costs to target levels within 12 months, especially among already relatively efficient providers. 4

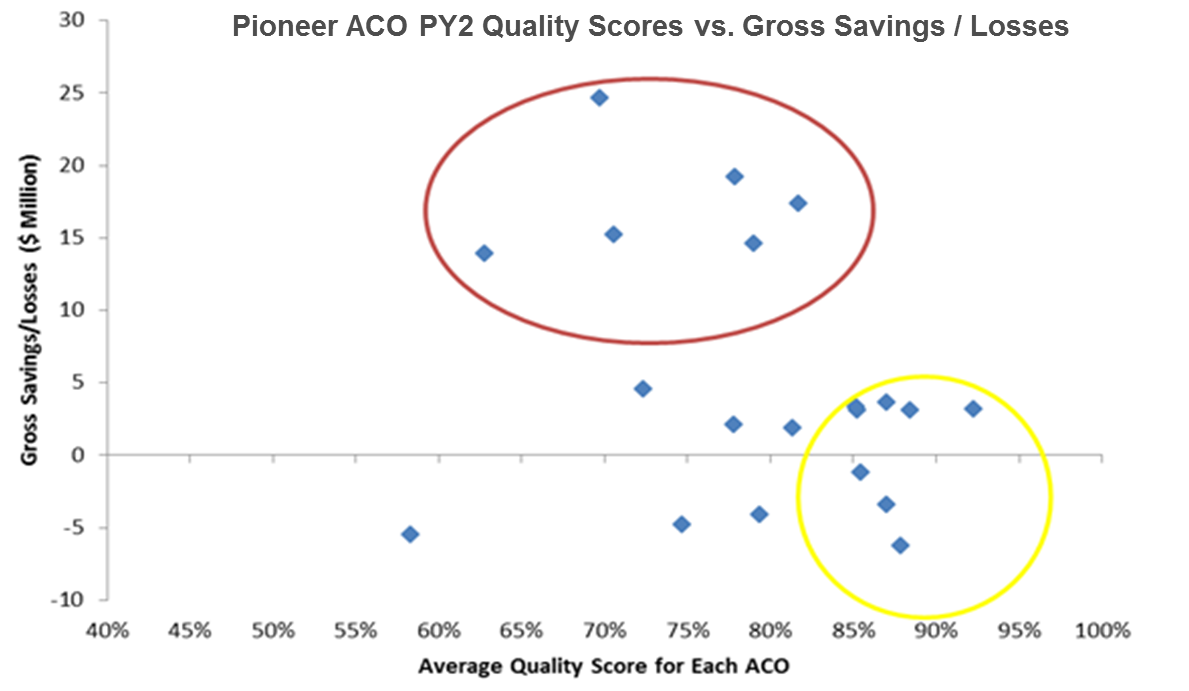

Year 2 results also highlighted improved quality scores for ACO participants relative to their FFS peers; 14 of 23 (61 percent) had lower costs, but only 11 of 23 (48 percent) had sufficiently lowered costs to generate shared savings. Four ACOs dropped out after or during Year 2. According to a Brooking Institute analysis, the average per capita Medicare spending in the metropolitan area of those ACOs in the red circle (higher savings, average quality scores) was $11,544 — significantly above the average Pioneer ACO county of $10,384.5 The data suggest that higher levels of baseline spending (reflective of local market provider inefficiency or ineffectiveness) may be more important than actual performance to generate shared savings.

Brookings: A More Complete Picture of Pioneer ACO Results;

SL Kocot, R White, P Katikaneni, M. McClellan; 10/13/14.

Increasing health system consolidation raising commercial prices

Healthcare consolidation is increasing across all sectors, thereby highlighting the potential for oligopolistic pricing. For example, in 2011–2013, there were 285 announced merger and acquisition deals involving 683 hospitals, an increase of 55 percent of deals as compared to 2008-2010 when there were 184 deals involving 283 hospitals. 6 The HMA - Community Health Systems (CYH) announcement alone involved 206 hospitals. However, unlike the HMA-CYH, not all announced deals actually close.

Consolidation during this period contributed to a rise in the aggregate hospital payment-to-cost ratio for private payers from approximately 133 percent to 148 percent.7 According to the Healthcare Cost Institute, for commercial payers:8

- Inpatient services: Acute inpatient hospital admissions fell 2.3 percent, while prices rose 6.7 percent, causing overall inpatient spending to rise by 3.8 percent. The average price per-admission grew by $1,067, in 2013 to $18,030.

- Outpatient services: Outpatient visits declined by 0.8 percent, while prices rose 6.4 percent. Total outpatient visit spending grew 5.5 percent.

The commercial payer price increases are being masked by media focus on overall growth rates subject to changes in payer mix, limited Medicare and Medicaid reimbursement growth and declining to flat utilization.

Physicians getting squeezed by insurers

Spending growth in physician and clinical services declined from 4.3 percent (price: 1.0 percent, volume: 3.3 percent) in September 2011 through September 2012 to 4.0 percent (price: -0.2 percent, volume: 4.2 percent) in 2012-13 and 2.1 percent (price: 0.8 percent, volume: 1.3 percent) in 2013-2014.9 Physicians, especially those in primary care and related specialties, remain critical to enhanced management of chronic conditions and diseases, as well as to the influx of newly covered Medicaid patients.

More than one-third of active physicians are over 55 years old, and another 25 percent are between the ages of 45 and 54.10 Twenty-six percent of physicians are now employed by hospitals; the percentage for primary care physicians and cardiologists is higher.11 A majority of physicians are malcontents; 59 percent would not recommend a medical career as a profession.12 Thirty-six percent of physicians plan to retire or leave medicine within 10 years due to “burn out”, a desire not to practice in an era of healthcare reform or economic factors.12

Declining morale, combined with accelerated retirements, will exacerbate the already forecasted shortages of primary care physicians.

Lowering government costs without necessarily creating value

Three-quarters of Medicaid and 28 percent of Medicare beneficiaries are enrolled in Managed Care.13 Plan participation allows government agencies to transfer risk and better estimate annual costs. However, managing financial risk does not imply care delivery efficiency and effectiveness. A recent investigation by the Health and Human Services Inspector General discovered that 48 percent of providers listed as serving Medicaid patients were either inaccurately listed, or did not accept Medicaid or new Medicaid patients. Appointment wait times were also excessive.14 Selection bias, contract exclusions, restricted access and utilization constraints are often used to maximize plan profitability.

Wellpoint’s acquisition of AmeriGroup in July 2012 signaled the financial benefits to be accrued from Medicaid expansion.15 The number of Medicare Advantage plans has declined from 2,830 in 2009 to 2,014 in 2014.16 Dual-eligible interest among insurers is rising due to the high level of spending associated with the lack of care coordination and co-morbidity management, and an excess of institutionalization.

Shifting healthcare costs to employees reduces utilization

Since 2008, the average worker contribution to employee premiums increased at a 6.3 percent compound annual growth rate (2014: $4,823), as compared to employer contributions at 4.3 percent (2014: $12,011).17 Rising deductibles, co-insurance and co-payments represent additional out-of-pocket expenses. High-deductible health plans (HDHPs), those with a minimum deductible of $1,250 for self-only coverage and $2,500 for family coverage, have also grown rapidly during this period with 17.4 million enrollees as of January 2014.18

Higher out-of-pocket costs are affecting the overall utilization of health services. Approximately 30 percent of consumers have deferred visiting a physician, undergoing a test, filling a prescription or complying with treatment due to economic reasons.19 In one-third of cases, the consumer believes treatment was delayed for a serious condition.19 Worse outcomes and higher costs in these patients are likely to ensue as preventable or reversible conditions progress to more severe forms. The net cost impact due to deferral is likely higher due to the concentration of costs among those that are most ill.

Furthermore, anecdotal evidence suggests higher out-of-pocket expenditures among employees with commercial plans are leading to an increase in unpaid bills among middle-class workers. Health-related bankruptcies affected 1.7 million Americans in 2013.20

Conclusion

Short-term stabilization of national health expenditures does not signify transformational change in care delivery. Nor does it imply a sustainable moderation in costs.

Insurance companies have emerged as the primary beneficiaries of the PPACA. Higher enrollment rates, combined with rising commercial premiums (e.g., 9.5 percent in 2011, the highest rate in five years), changes in benefit design and more restrictive networks have led to Aetna, Cigna and Wellpoint outperforming the S&P500 by 50 to 100 percent.21, 22

Pharmaceutical companies have also emerged as winners, though the full impact of the change in their business model has yet to be felt. Specialty drugs represent 1 percent of prescriptions and 25 percent of pharmaceutical expenditures and near-monopolistic pricing is evident.21 Annual specialty drug spending increases of 18 to 20 percent have become the norm.23

The Medicare ACO data appears paradoxical. Less efficient and effective providers generate greater savings in high-cost markets — as compared to more efficient and effective providers with many years of experience focused on the care continuum and reducing costs. Opportunities may exist for a number of the Pioneer ACOs (and others) to extend their geographic reach into contiguous areas of relative inefficiency.

Accelerated spending is inevitable. The growth rate in health spending through nine months (Sept.) 2014 was 4.7 percent, somewhat higher than the 3.6 percent reported in 2013.24

-------------------------------------------------------------------------------------------------------------

1 New York Times. Health Spending Rises Only Modestly; Dec. 4, 2014

2 White House Blog; Council of Economic Advisers; Dec. 3, 2014.

3 CMS. Table 1 National Health Expenditures; Aggregate and Per Capita Amounts, Annual Percent Change and Percent Distribution, Selected Calendar Years 1980-2013

4 The Advisory Board Company Daily Briefing. Nine ACOs Are Leaving the Pioneer ACO Program; July 16, 2013.

5 Brookings Up Front. A More Complete Picture of Pioneer ACO Results; Oct. 13, 2014.

6 Irving Levin Associates, Inc. The Healthcare Acquisition Report, 20th Edition, 2014.

7 AHA Trendwatch Chart Book, 2014. Chart 4.6.

8 Healthcare Cost Institute. Spending Per Privately Insured Grew 3.9% in 2013, as Falling Utilization Offset Rising Prices; Oct. 28, 2014.

9 Center for Sustainable Health Spending, Altarum Institute. Health Care Price Growth Settles Into Narrow Range at Low Rate. Price Brief #14-11; Nov. 12, 2014.

10 AMA. Physician Characteristics and Distribution in the U.S. 2015 Edition.

11 Beckers Hospital Review. Survey: Number of Employed Physicians Up 6%; June 18, 2013.

12 Filling the Void: 2013 Physician Outlook and Practice Trends. Jackson Healthcare.

13 AHA Trendwatch Chart Book, 2014. Charts 1.23 and 1.25.

14 New York Times. Half of Doctors Listed as Serving Medicaid Patients Are Unavailable, Investigation Finds; December 8, 2014.

15 AMED News. Acquisition may be first wave of Medicaid managed care consolidations; July 30, 2012.

16 Kaiser Family Foundation; Medicare Advantage 2014 Spotlight.

17 Kaiser Family Foundation; 2014 Employer Health Benefits Survey.

18 AHIP Center for Policy & Research. Jan. 2014 Census Shows 17.4 Million Enrollees in Health Savings Account— Eligible High Deductible Health Plans (HSA/HDHPs).

19 Costs Still Keep 30% of Americans From Getting Treatment: Lower Income and Younger Adults Most Likely to Have Delayed Treatment.

20 Christina LaMontagne. NerdWallet Health finds Medical Bankruptcy accounts for majority of personal bankruptcies; Mar. 26, 2014.

21 AHA Trendwatch Chart Book, 2014. Chart 1.27 Annual Change in Health Insurance Premiums, 2000-2013.

22 Yahoo Finance information.

23 AHIP Center for Policy and Research. Issue Brief: Specialy Drugs – Issues and Challenges; Feb. 2014 23 Express Scripts Insights. Specialty Drug prices to Increase 67% by 2015; May 22, 2013.

24 Center for Sustainable Health Spending, Altarum Institute. Health Spending Continues Moderate Growth Through Third Quarter. Spending Brief #14-11; Nov. 12, 2014.