The Automotive Industry Continues to Look Towards an Electric Future While Supply Issues Hinder Current Performance

Production shutdowns due to semiconductor shortages are slowing, but chip issues are expected to affect the industry throughout 2022. Automotive inventory increased slightly to 1.1 million units in December, but supply continues to weigh on sales performance.

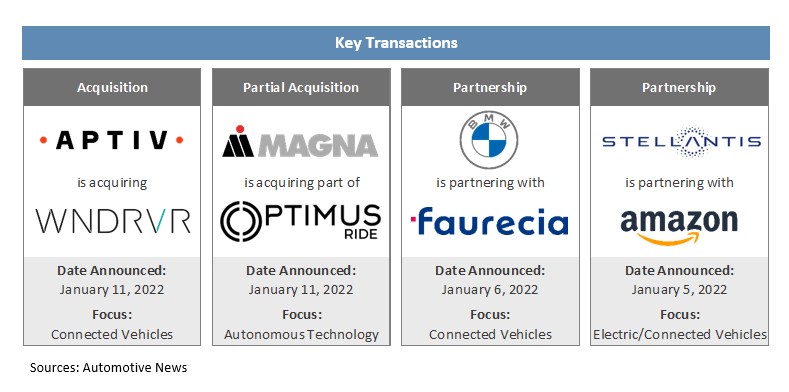

Automakers are using the M&A and transaction market to enhance connected capabilities and the in-vehicle experience. Meanwhile, fortifying chip supply and autonomous technology remain a focus in partnership agreements.

In regulatory news, Tesla is facing a recall for safety issues, and the Biden administration reversed a Trump-era rule that restricted California from setting additional emission regulations.

Additional January insights are included below.

Financial Performance

Auto Forecast Solutions’ (AFS) numbers show that shutdowns and delays resulted in 10.2 million lost vehicles globally during calendar year 2021 with China taking the biggest hit of any region at 3.6 million units. However, North America and Europe both took significant hits with 3.1 million and 3.0 million units axed from factory schedules, respectively. The latest AFS estimates suggest an additional approximately 833,000 total cars and trucks will be affected by chip-related supply disruptions in 2022 as factories in China and North America have already begun to encounter problems.

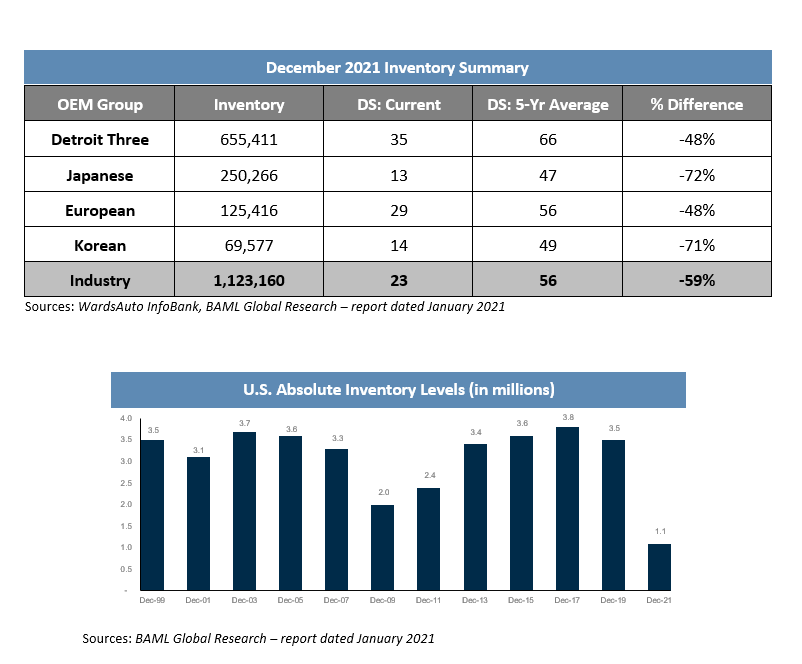

Automakers have adapted to account for the limited supply of chips, which has helped global production begin to steady with less unplanned downtime in recent months. Despite potentially improved production during the upcoming year, dealerships do not expect pre-crisis levels of inventory to return, as a new normal may be emerging with lower in-stock inventory. It is anticipated most vehicles will be sold as soon as they arrive at dealerships and go directly to customers through at least the first three quarters of 2022.

Automotive inventory increased by 77,000 units in November, resulting in approximately 1.1 million total units. This translates to a days’ supply (DS) that is 59 percent below the five-year average at 23 DS. With December marking the third consecutive month of an absolute increase in inventory, it appears that inventory levels are improving from the 1 million-unit trough. However, new light vehicle sales remained low as the 12.4 million seasonally adjusted annualized rate (SAAR) of sales in December continued the pattern of sales deterioration. The December figures resulted in a 2021 full-year sales performance of 14.9 million units, a 3 percent increase from 2020 sales. North American production in 2021 also decreased by nearly 70,000 units from 2020, which was already down 20 percent from 2019 production, and production is expected to stay at depressed levels at least through the first half of 2022.

The disappointing level of sales improvement in 2021 from 2020 was due to a drop-off in the SAAR from 16.8 million units in the first half of 2021 to 13.0 million units in the second half of the year. Looking forward, January through March are typically inventory build months prior to the spring and summer selling season, and continued improvement in production during this period will be critical to avoid constraining sales moving forward. IHS Markit forecasts U.S. sales volumes to reach nearly 15.5 million units in 2022 and continues to expect stabilization of the supply environment to occur in the second half of the year.

Click here for a report prepared by A&M and Jones Day detailing several long-term automotive supply chain challenges expected to affect the industry

Transaction Activity

In recent transaction news, semiconductor company Qualcomm announced deals to supply chips to Volvo, Honda, and Renault, signaling an accelerated effort for Qualcomm to expand into the automotive sector. Additionally, Intel’s autonomous driving unit, Mobileye, announced it is partnering with Volkswagen, Ford, and Geely to collaborate on driver assistance and autonomous vehicle technology. Eaton Corporation, a power management company, announced the purchase of Royal Power Solutions, an electric connectivity components company, in an effort to expand into the electric vehicle supply chain business. Lastly, Honda and battery maker LG Energy Solution are rumored to be planning a U.S. battery joint venture which could cost $3.4 billion.

See below for additional detail on recently announced transactions.

- Aptiv, an automotive technology supplier, announced it has agreed to purchase software firm Wind River from private equity group TPG Capital for $4.3 billion. The acquisition further enables Aptiv to capitalize on the digitalization of vehicles with features such as over-the-air updates and other connected technologies.

- Magna agreed to a deal with Optimus Ride, a self-driving shuttle company, to hire more than 120 of Optimus Ride’s engineers and acquire its autonomous driving technology. While Magna is not acquiring the company outright, Optimus Ride has no go-forward plans to continue operations.

- BMW announced a partnership with Faurecia to use the Aptoide Automotive App Store in future BMW vehicles. Aptoide is a scalable platform that offers over-the-air updates, in-vehicle purchases and more than one million apps. Faurecia and Aptoide created a joint venture in 2019 and the platform is in talks with additional automakers for integration.

- Stellantis is partnering with Amazon in a series of software and electric vehicle pursuits. The partnership will aim to get the electric Ram ProMaster van on the road next year and Amazon will be the first commercial customer of the vehicle. The companies will also collaborate to offer artificial intelligence-based applications as part of the STLA SmartCockpit platform.

Regulatory Landscape

USMCA Fight Resolution: Canada recently joined Mexico in its request to form a dispute settlement panel regarding the United States’ interpretation of the United States-Mexico-Canada Agreement (USMCA). The key issue is the United States’ strict rules interpretation for calculating regional value content for core auto parts. The USMCA replaced the North American Free Trade Agreement in 2020.

Tesla Recall: The National Highway Traffic Safety Administration (NHTSA) announced that Tesla will recall more than 475,000 vehicles to address rearview camera and trunk issues that increase the risk of crashing. This is latest of a variety of issues that the NHTSA has had with Tesla; the automaker recently agreed to stop allowing video games to be played on vehicle screens while in motion after the NHTSA opened a probe.

California Emissions Regulations: President Biden finalized a reversal of former-President Trump’s rule which barred California from implementing vehicle regulations that conflicted with the federal government’s authority to set Corporate Average Fuel Economy requirements. The reversal allows for states to actively set more stringent vehicle emission regulations.

Halted Vaccine Mandates: The U.S. Supreme Court blocked the Occupational Safety and Health Administration from implementing a rule that would have required 80 million workers to get vaccinated or periodic tests. The rule was part of President Biden’s push to get more U.S. workers vaccinated. Certain automakers have implemented mandatory vaccine mandates, but others in the industry have not set as strict of standards.

Stay connected to industry financial indicators and check back in February for the latest Auto Industry Spotlight.